Most advice focuses on retirement and long-term savings. But the financial stress most people feel happens in the next 30–60 days — and almost no one has a plan for it.

March 3, 2026

Ask someone what "financial planning" means, and you'll get some version of the same answer. Save for retirement. Build an emergency fund. Start investing early so compounding works in your favor. Maybe set aside money for college or a house.

None of that is wrong. But it's incomplete — because it skips the time horizon where most financial stress actually lives.

Not ten years from now. Not even one year from now. The next 30 to 60 days.

Most people don't need more long-term planning advice. They need short-term visibility they've never been told to build. Here's why — and what that visibility actually looks like.

The personal finance industry is overwhelmingly oriented around long time horizons. The most common advice — max out your 401(k), automate your savings, don't try to time the market — is built on a shared assumption: if you get the big picture right, the day-to-day takes care of itself.

For some people, that's true. But for most, it isn't. You can be diligently contributing to a retirement account and still get blindsided by an overdraft next Tuesday. You can have a fully funded emergency fund sitting in a high-yield savings account and still not know whether your checking account can safely cover this week's expenses.

That's because long-term planning and short-term visibility solve fundamentally different problems. Long-term planning answers "Am I on track for the future?" Short-term visibility answers "Am I going to run into trouble this month?" The personal finance world treats the first question as the only one that matters. And that leaves a massive gap in how most people actually manage their money.

Here's what the long-term planning framework misses: most financial stress isn't caused by a failure to save for retirement. It's caused by near-term timing collisions.

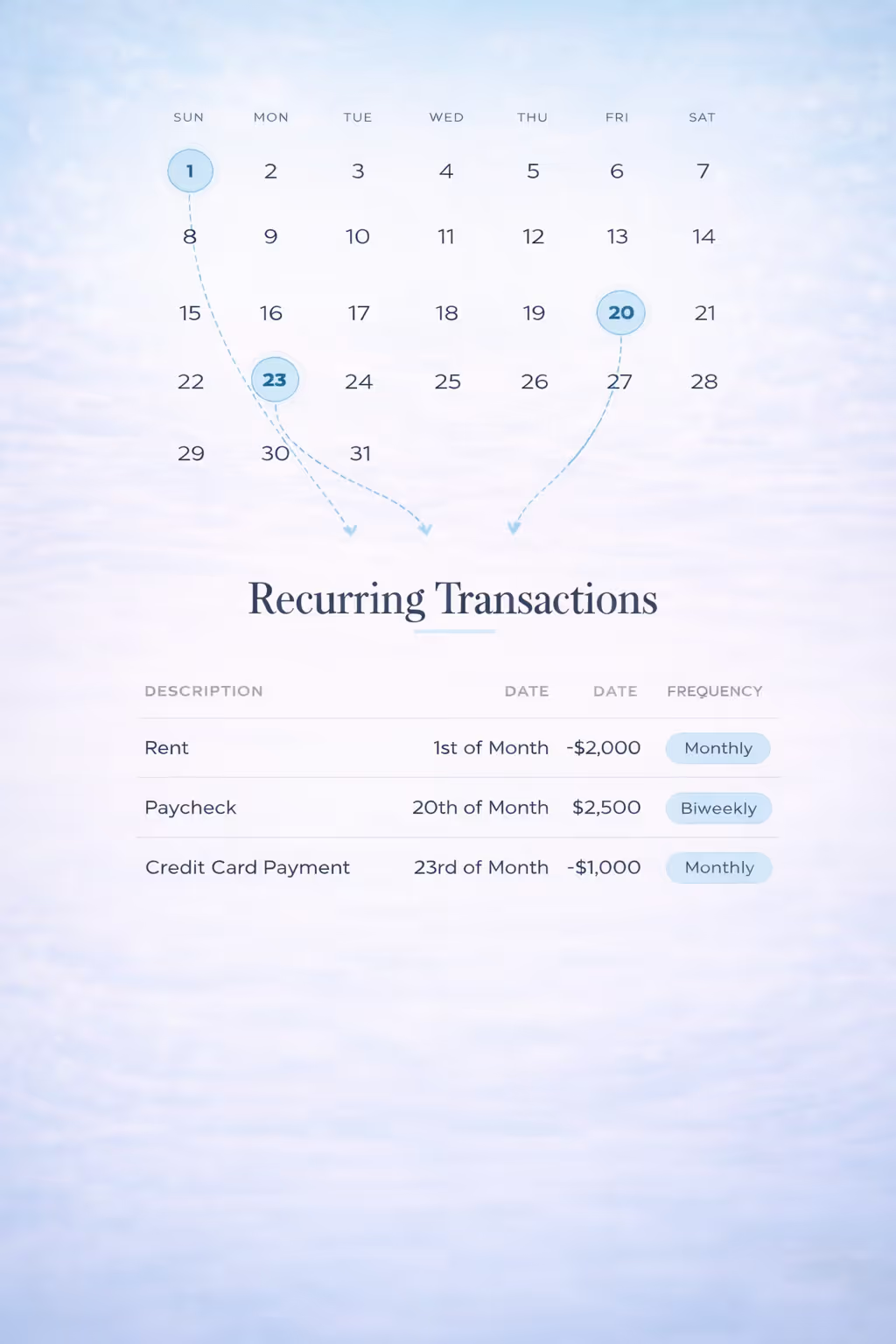

The rent hits two days before the paycheck clears. The credit card payment and the car insurance premium land on the same morning. A forgotten annual subscription tips a healthy-looking balance into the red. These aren't planning failures in any meaningful sense — they're visibility failures. The money exists, or will exist soon. The problem is that it's not in the right place at the right time.

This isn't a hypothetical. Researchers at the Brookings Institution have noted that overdrafting is more about running out of time than running out of money — people are often just hours away from having the funds to cover a shortfall. Data from the Consumer Financial Protection Bureau paints a similar picture: frequent overdrafters typically have no more than a few hundred dollars in their account at the end of any given day. They're not reckless. They're navigating a complex sequence of inflows and outflows with no way to see what's coming — a pattern that plays out across billions of dollars in overdraft fees every year.

A person who overdrafts isn't necessarily bad at financial planning. They just don't have visibility into next week's cash position. And nothing about their current bank balance tells them what they need to know — because a balance is a snapshot of right now, not a projection of what's ahead.

If you're thinking "isn't this what a budget is for?" — you're not alone. But a budget doesn't actually address the timing problem.

A budget categorizes spending. It tells you how much you spent on groceries last month, whether you're over or under on dining out, and how your total spending compares to your income. That's useful. But it operates in monthly totals, which means it flattens the sequence of events within the month into a single number.

A budget can tell you that your fixed expenses add up to $2,000 per month. It can't tell you that on March 14th, three of those expenses land on the same day — and your paycheck doesn't arrive until March 15th. That one-day gap is invisible to a budget. It's also exactly the kind of gap that causes overdrafts, missed payments, and unnecessary stress.

Forecasting and budgeting solve different problems. A budget answers "Where did my money go?" A forecast answers "What's about to happen to my balance?" Most people have some version of the first. Almost nobody has the second.

A short-term cash-flow forecast starts with your current checking account balance. It then lays out every known income and expense — paychecks, rent, subscriptions, insurance premiums, credit card payments — on the specific day each is expected to hit. From there, it walks forward day by day, adding income and subtracting expenses, to simulate how your balance rises and falls over the next 30 to 60 days.

The output isn't a category breakdown or a spending score. It's a projected balance for every day in the forecast window. And it reveals two things no other personal finance tool shows you.

First, whether your account is at risk — and second, how much room you actually have. Your projected lowest balance is the minimum point your checking account is expected to reach over the forecast period. If that number dips below zero, you have a problem. But most people don't just want to stay above zero — they want to stay above a personal comfort threshold: a minimum balance they've deliberately set based on their own circumstances. The distance between your projected low point and that threshold is your true available surplus — the amount you can confidently move to savings, invest, or put toward debt or spend without creating a future shortfall.

This is also the foundation of overdraft prevention. If you can see that your balance is projected to dip dangerously low on a specific date, you can act before it happens — not after the fee has already posted. You can build a forecast step by step on your own, or use a tool that automates the process. Either way, the value is the same: you stop reacting and start anticipating.

Here's the thing: none of this is new. Corporate treasury teams have operated this way for decades.

Every major company runs daily cash-position forecasts. They know exactly how much liquidity they have, when shortfalls are projected, and how much idle cash they can deploy into short-term investments. No CFO would manage a company's cash by glancing at today's bank balance and hoping for the best. The tools and the logic have existed for years — they've just never been translated to the consumer level. But the gap is closing, and the framework translates more directly than you'd expect.

The gap between how corporations manage cash and how individuals manage cash is striking — and increasingly unnecessary. What a corporate treasurer does with enterprise software and a finance team, a consumer can now approach with the right personal tool. The principle is identical: don't just know where you stand today. Know where you're headed.

Long-term planning tells you where you're headed over the years. Budgeting tells you where your money went last month. Short-term forecasting tells you what's about to happen — and that's the layer almost everyone is missing.

If you've ever felt a vague anxiety about your checking account even though you "should" have enough, or if you've ever been surprised by an overdraft you didn't see coming, the issue probably isn't discipline or planning. It's that you're managing your near-term cash flow without any forward visibility.

Centinel is built to fill exactly this gap. It runs a daily 60-day forecast for your checking account, showing you what's projected as available to move or spend and flagging risks before they hit — with the specific date and amount. It's the short-term visibility layer that sits alongside your budget and your long-term plan, not replacing either, but completing the picture.

Because the question most people actually need answered isn't "Am I saving enough for retirement?"

It's "What's going to happen to my checking account this month?"

And until you can answer that, your financial plan has a blind spot.

STAY A STEP AHEAD