Most people keep more in checking than they need—but don't know what's safe to move. Learn how to calculate your Available Cash with confidence.

January 25, 2026

Most people don't think of their checking account as a place where money goes to waste. But in many cases, that's exactly what's happening.

American households collectively hold approximately $4.5 trillion in checking accounts—and most of that money earns almost nothing. The result, according to our analysis, is an aggregate opportunity cost of $50 to $90 billion per year: money that could be earning 4% or more in a high-yield savings account, but instead sits idle at 0.07%.

The difference matters. If you're keeping $5,000 more in your checking account than you actually need, that's roughly $200 per year in lost interest—money that could be compounding in a savings account, paying down high-interest debt, or growing in an investment portfolio. Scale that across years, and the opportunity cost becomes substantial.

The challenge isn't awareness. Most people know, at least vaguely, that they probably have more in their checking account than they need. The challenge is confidence: how do you know what's actually safe to move?

Here's why most people never optimize their checking account: they're afraid.

Not irrationally afraid—reasonably afraid. If you move too much money out and then overdraft, you face fees, declined payments, and the stress of scrambling to cover the gap. The consequences of being wrong feel immediate and painful. The consequences of being too conservative—leaving money idle—are invisible and abstract. So people default to keeping more than they need, just to be safe.

The result is a kind of paralysis. You suspect you could move some money to a higher-yield account, but you don't know exactly how much is safe to move. So you move nothing. Or you move a small amount that feels "safe" but leaves most of your surplus untouched.

The traditional advice doesn't help much here. "Keep 1-2 months of expenses plus a 30% buffer" gives you a static number, but it doesn't account for the actual timing of your cash flows. You might have $8,000 in your account today, but if rent hits tomorrow and your paycheck doesn't arrive until Friday, that $8,000 isn't as "available" as it looks.

What you need isn't a rule of thumb. What you need is visibility into where your balance is actually headed.

The way to know what's "too much" is to stop looking at your current balance and start looking at your projected lowest balance over the coming weeks.

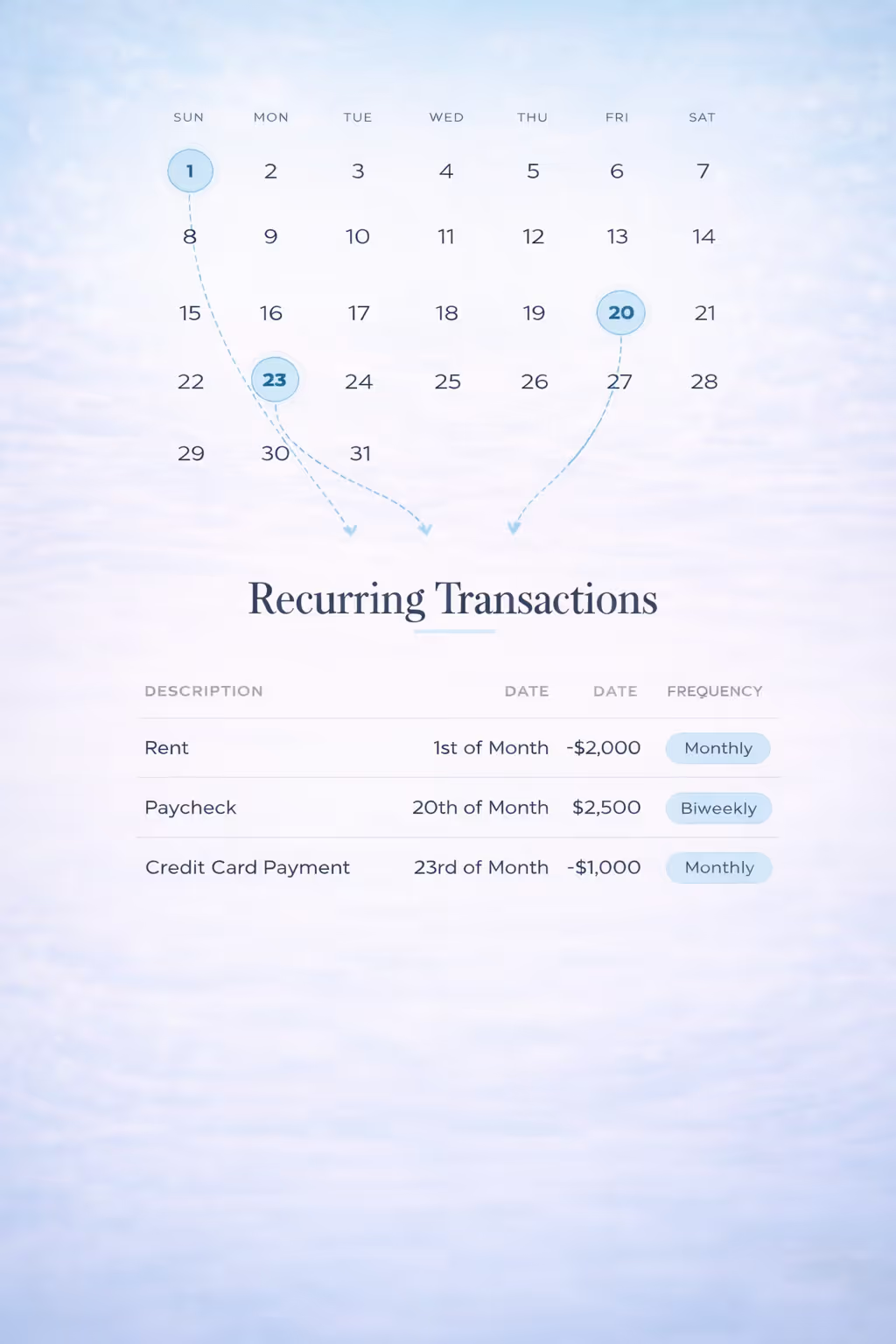

This is where checking account cash flow forecasting comes in. By mapping out your upcoming income and expenses day by day over a forward-looking window—such as 60 days—you can simulate how your balance will rise and fall. The result is a projected trajectory that shows you exactly where your checking account is headed.

The most important number this forecast produces is your Account Low—your projected lowest balance over the forecast window. This is the point where your balance dips to its minimum before the next inflow brings it back up.

Once you know your Account Low, you can compare it to your Floor—the minimum balance you're personally comfortable with. It's the lowest point you want your checking account to reach before you'd start feeling uncomfortable. Setting your Floor is a critical component of deciding how much to keep in your checking account.

The formula for what you can confidently move is simple:

Available Cash = Account Low − Floor

If your Account Low over the next 60 days is $2,500 and your Floor is $1,000, you have approximately $1,500 of Available Cash. That's money you could move to a high-yield savings account, use to pay down debt, or invest—because even at your lowest projected point, you'll still be above your personal minimum.

You're not guessing. You're not relying on a generic rule. You're calculating what's safe to spend or move based on your actual cash flow.

Once you've identified that you have Available Cash, the question becomes: where should it go?

There's no single right answer—it depends on your financial situation, goals, and risk tolerance. But here are the common options to consider.

High-yield savings is the most conservative choice. Your money stays liquid and accessible, typically within a few business days, while earning meaningful interest. As of this writing, many online banks offer ~4% APY on high-yield savings accounts, compared to the near-zero rates at most traditional checking accounts. This is a sensible default for money you might need in the medium term—it's working harder for you without taking on risk.

Paying down high-interest debt can offer a guaranteed "return" equal to your interest rate. If you're carrying credit card debt at 20% or more APR, directing surplus cash toward that balance is often the highest-impact financial move you can make. Every dollar you pay down saves you that interest rate in future charges.

Investing offers the potential for higher long-term returns but comes with risk and reduced liquidity. This is generally appropriate for money you're confident you won't need for years—not for short-term surplus you might need to access.

The right choice depends on your circumstances: your interest rates, your debt levels, your financial goals, and your time horizon. The point of this article isn't to tell you what to do with your surplus—it's to help you confidently identify that you have one. Once you know the number, you can make an informed decision about where to direct it.

This article is for informational purposes and reflects general principles of cash flow management. It's not financial advice, and your situation may require different considerations. When in doubt, consult a financial professional.

Optimizing your checking account balance isn't without risks. Here's what can go wrong—and how to avoid it.

If your Floor doesn't leave enough cushion for variability or unexpected expenses, you might find yourself dipping below it more often than you'd like—or worse, actually overdrafting. The solution is to be honest with yourself about your risk tolerance. Start conservative. You can always lower your Floor later once you've observed how your forecast behaves over a few months.

Just because you have Available Cash doesn't mean you need to move all of it immediately. Your forecast is based on what you know today, and life is unpredictable. A recurring transaction you didn't capture when building your forecast, an automatic payment that changed, or an unexpected expense can all shift your Account Low. Leaving some margin above your Floor—rather than optimizing down to the exact dollar—gives you room for the unexpected.

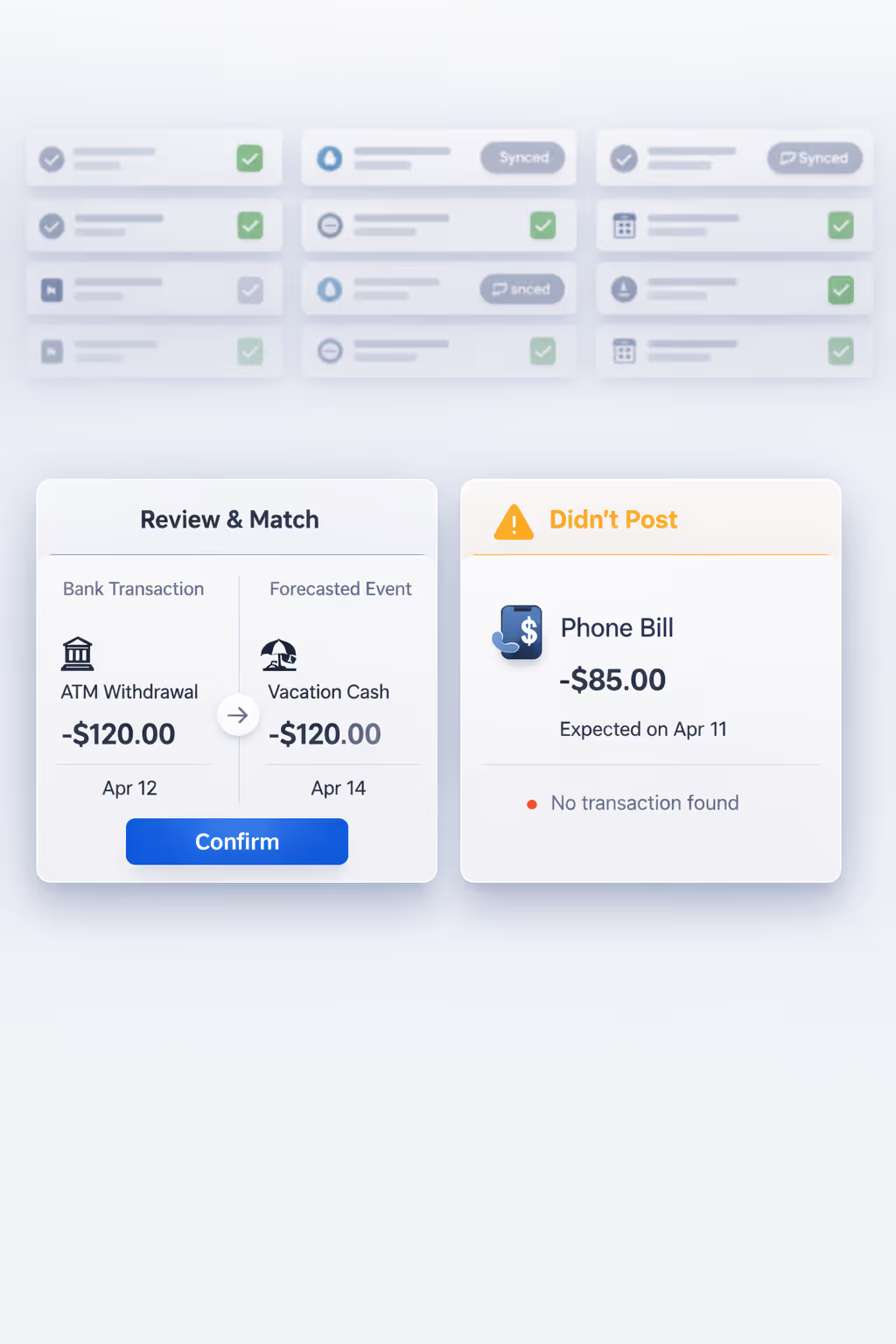

A forecast is only as good as the information it's based on. If you change jobs, adjust your rent, or have a one-time expense coming up, your forecast needs to reflect that. Stale inputs produce stale outputs, which can lead to unpleasant surprises. Treat your forecast as a living document that requires periodic updates — from keeping your starting balance current to catching the variance between what you estimated and what actually posted, maintaining an accurate forecast is what keeps the Available Cash number you're acting on trustworthy. Credit card payments are the clearest example of this — the amount is a projection until the statement closes, which means your forecast is carrying an estimate for what's often one of your largest line items.

A forecast is an estimate, not a guarantee. Transactions can post in unexpected order, automated payments can change without notice, and life doesn't always follow the schedule. Treat your Available Cash figure as directional guidance—a reasonable approximation of what you can move—not a precise number to optimize against to the penny.

The common thread across all these pitfalls is this: stay engaged. The forecast is a tool that requires attention, not a set-it-and-forget-it solution. The more you maintain it, the more reliable it becomes—and the more confidently you can act on what it tells you.

The real value of this approach isn't a single optimization—it's the ongoing practice. When you regularly know where you stand, you can make incremental improvements over time: moving a bit more to savings when you have room, pulling back when things get tight, and always staying ahead of potential problems rather than reacting to them.

For some people, a periodic manual review works well. You might check your forecast weekly or biweekly, update it with any changes to your income or expenses, and decide whether to move surplus cash. This approach requires discipline, but it gives you full control.

Centinel's free tier supports this manual approach. You can build and maintain your forecast yourself, set your Floor, and see your projected Available Cash. The tradeoff is that keeping the forecast accurate requires regular attention—you're the one updating balances and adjusting for changes.

For others, automation makes the difference between doing this consistently and not doing it at all. Centinel's Premium tier automatically pulls your checking balance daily, updates your forecast as transactions post, and incorporates your credit card statement data to keep payment projections accurate. This means your Available Cash figure stays current with less manual effort. It also means you're more likely to catch potential issues—like a projected dip below your Floor—before they become problems, because the system is recalculating daily based on fresh information.

Either approach can work. A manual forecast you actually maintain is better than an automated one you ignore. And an automated forecast that stays accurate is better than a manual one that goes stale. The key is choosing the approach you'll actually stick with—and then making it part of your routine.

Most people keep more in their checking account than they need. Not because they've carefully calculated that they need it, but because they don't have a reliable way to know what's safe to move. The cost of this uncertainty is invisible but real: idle cash that could be earning interest, paying down debt, or building long-term wealth.

The solution isn't to guess, and it isn't to follow a generic rule that doesn't account for your actual cash flow. It's to forecast your balance forward, set a Floor you're comfortable with, and let the math show you what's available. Then make a habit of checking in, keeping your forecast current, and putting your surplus to work.

This is the same basic approach that powers corporate cash management — and it works for your checking account too. They don't leave money sitting idle because they're not sure if they need it. They forecast, they set thresholds, and they optimize. There's no reason you can't do the same.

The first step is knowing your number. Once you do, the rest is just execution. Ready to take the next step? Here's a simple, practical way to create a checking account cash flow forecast.

STAY A STEP AHEAD