Learn a two-step process to identify every recurring transaction in your checking account — so your cash flow forecast starts with complete, accurate inputs.

March 15, 2026

Identifying your recurring transactions is one of the most important steps in creating a checking account cash flow forecast — and it's the step most people rush through. A forecast is only as accurate as the cash flow events it contains. Miss one recurring expense, and your projected Account Low — the lowest point your balance is expected to reach over the next 60 days — could be off by hundreds of dollars. That means your Available Cash figure overstates what's truly safe to move, or a warning about an upcoming overdraft never fires when it should.

Understanding how the forecast works mechanically makes this point concrete: your cash flow schedule is one of only a few inputs the algorithm uses. Everything the forecast produces — every projected balance, every warning, every Available Cash figure — is derived from those inputs. If the inputs are incomplete, the outputs are misleading.

The most reliable way to build a complete list is a two-step process: first, write down every recurring transaction you can think of from memory, then verify that list against your actual bank statement history to catch what you missed. The rest of this article walks through both steps in detail.

Before you start listing transactions, it helps to clarify what you're actually looking for. A checking account forecast needs every predictable inflow and outflow that debits or credits your checking account. That's a narrower universe than "all my recurring expenses."

The distinction matters most if you use credit cards. If you pay for Netflix, Spotify, your gym membership, and your weekly groceries with a credit card, none of those individual charges touch your checking account. What does touch your checking account is your credit card payment — one transaction, once a month, for the combined total. For purposes of your forecast, the credit card payment is the recurring event that matters, not the individual charges behind it.

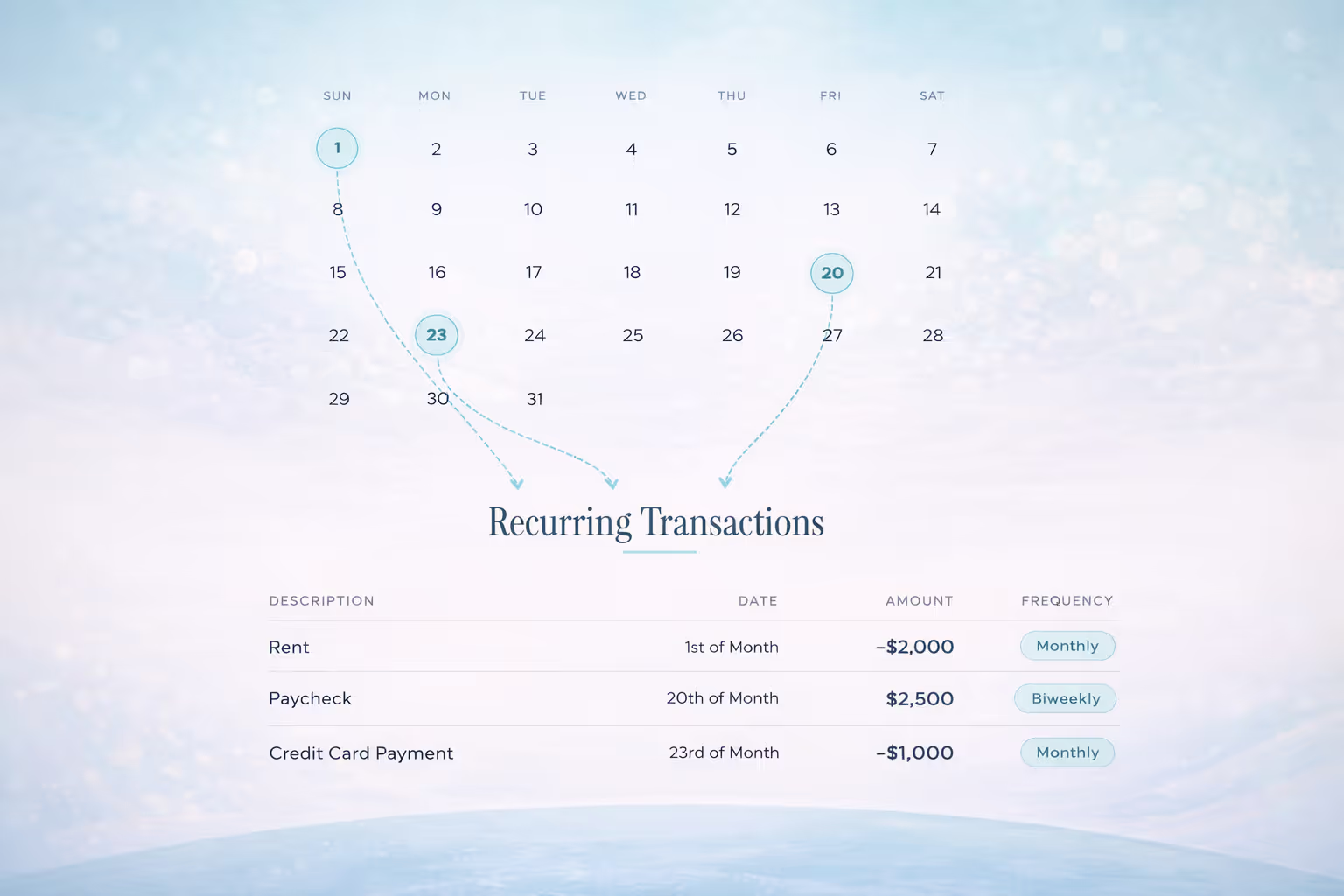

If you pay for subscriptions or memberships with a debit card, those charges do hit your checking account directly and belong in your forecast. But for most people, the transactions that flow through checking are a relatively manageable set: your paychecks, your rent or mortgage, loan payments, utility bills, insurance premiums, credit card payments, and any automatic transfers you've set up to savings or investment accounts. That's the universe you're trying to map.

The first step is pure recall. Sit down and list every recurring transaction you can think of that flows through your checking account. Don't look anything up yet — just write down what you already know. For each item, note three things: the approximate amount, the date it typically hits, and how often it recurs (every month, every two weeks, twice a month, quarterly, etc.).

Most people can get through this step fairly quickly and capture the large, obvious items: rent, car payment, paychecks, utility bills, credit card payments. These high-dollar, high-frequency items will likely account for 70-80% of the total dollar volume flowing through your account. That's a strong foundation.

Start with money coming in. Your primary paycheck is the most important cash flow event in your forecast, and you almost certainly know the amount, frequency, and typical deposit date. If you have a secondary income source — a side gig, a regular reimbursement, a recurring transfer from a partner — capture that too.

These are the outflows where you know the exact amount and the exact date every time: rent or mortgage, car payment, student loan payment, a fixed-rate insurance premium. These are the easiest to capture because they never change, and you probably know most of them from memory.

Some transactions hit on a predictable schedule but the amount changes: electric and gas bills, water, phone bills, credit card payments. You know they're coming; you just don't know the exact amount until the bill arrives. For now, write down your best estimate — you'll refine these in the next step.

If you've set up automatic transfers from your checking account to a savings account, investment account, or anyone else (like a recurring Venmo or Zelle payment to split rent with a roommate), those are outflows that belong in your forecast. People often forget about these because they set them up once and then stopped thinking about them — but they're still debiting your checking account on schedule.

Now that you have a list based on what you know, it's time to catch what you missed. Pull up your checking account transaction history — at least the last 60 — and work through it.

You're looking for any recurring transaction that didn't make your initial list. Scroll through the transactions and flag anything that appears more than once on a regular interval. Pay particular attention to smaller amounts that are easy to overlook: a $12 subscription you forgot about, an $8 monthly service fee from your bank, a $15 app subscription charged to your debit card.

As you review, this is also a good time to refine the variable-amount items from your brainstorm. Check the last two or three instances of each one — your electric bill, your credit card payments — and use a recent average or a slightly conservative (higher) estimate for your forecast. You don't need to be exact. Slightly overestimating your outflows means your forecast projects a lower balance than you'll actually have, which is a safer place to be than the reverse.

A 60-day bank statement review will capture monthly and biweekly transactions reliably, but it will miss anything that occurs less frequently. Annual and semi-annual payments — property taxes, vehicle registration, an annual insurance premium, a yearly software renewal, professional membership dues — are the items most likely to blindside your forecast, and they tend to be large amounts.

An effective way to catch these is to mentally walk through the calendar year month by month and ask yourself what financial obligations fall in each period. January might bring an annual subscription renewal. April has tax payments. Your vehicle registration might fall in September. The holiday season brings its own spending patterns. This exercise doesn't need to be exhaustive — even identifying two or three annual payments you would have otherwise missed can materially improve your forecast's accuracy.

This manual audit works well, but it does take time. Centinel's Premium tier automates much of this process by analyzing your bank transaction history and surfacing recurring patterns for you to confirm — turning what might be an hour of line-by-line review into a few minutes of verifying suggestions and filling in gaps.

Every recurring transaction you miss creates a gap between what your forecast projects and what will actually happen in your checking account. If you miss a $200 quarterly insurance premium, your forecast will show a balance $200 higher than reality on the day that payment hits.

That gap flows downstream into every decision you make based on the forecast. If you're using your Account Low to figure out how much is safe to spend or to optimize your checking account balance by moving surplus to savings or investments, an inflated number could lead you to move money you actually need. And if your balance is tighter than you realize, a missed transaction can push you below zero without warning — the kind of overdraft that a forecast is specifically designed to help you prevent.

The good news is that you don't need to be perfect on day one. The initial two-step process described here — brainstorm, then audit — will typically capture 90% or more of your recurring cash flow by dollar volume. From there, ongoing reconciliation closes the remaining gap. As you compare your forecast to what actually happens in your bank account over the following weeks, you'll naturally discover transactions you missed and patterns you didn't initially recognize. Each correction makes the forecast more accurate.

Whether you build your forecast in a spreadsheet or use a dedicated tool like Centinel, the completeness of your recurring transaction list determines the reliability of everything the forecast tells you. A forecast built on complete inputs gives you a number you can trust. One built on incomplete inputs gives you a number that feels useful but quietly misleads you — and that's worse than having no forecast at all.

STAY A STEP AHEAD