Account Low is your projected minimum checking account balance over the next 2 months. Here's how Centinel calculates it — and what it tells you about your cash flow.

January 2, 2026

Your checking account balance tells you what's there today. It says nothing about whether next week's bills will clear, whether you're heading toward an overdraft, or how much of what you're looking at is genuinely yours to deploy.

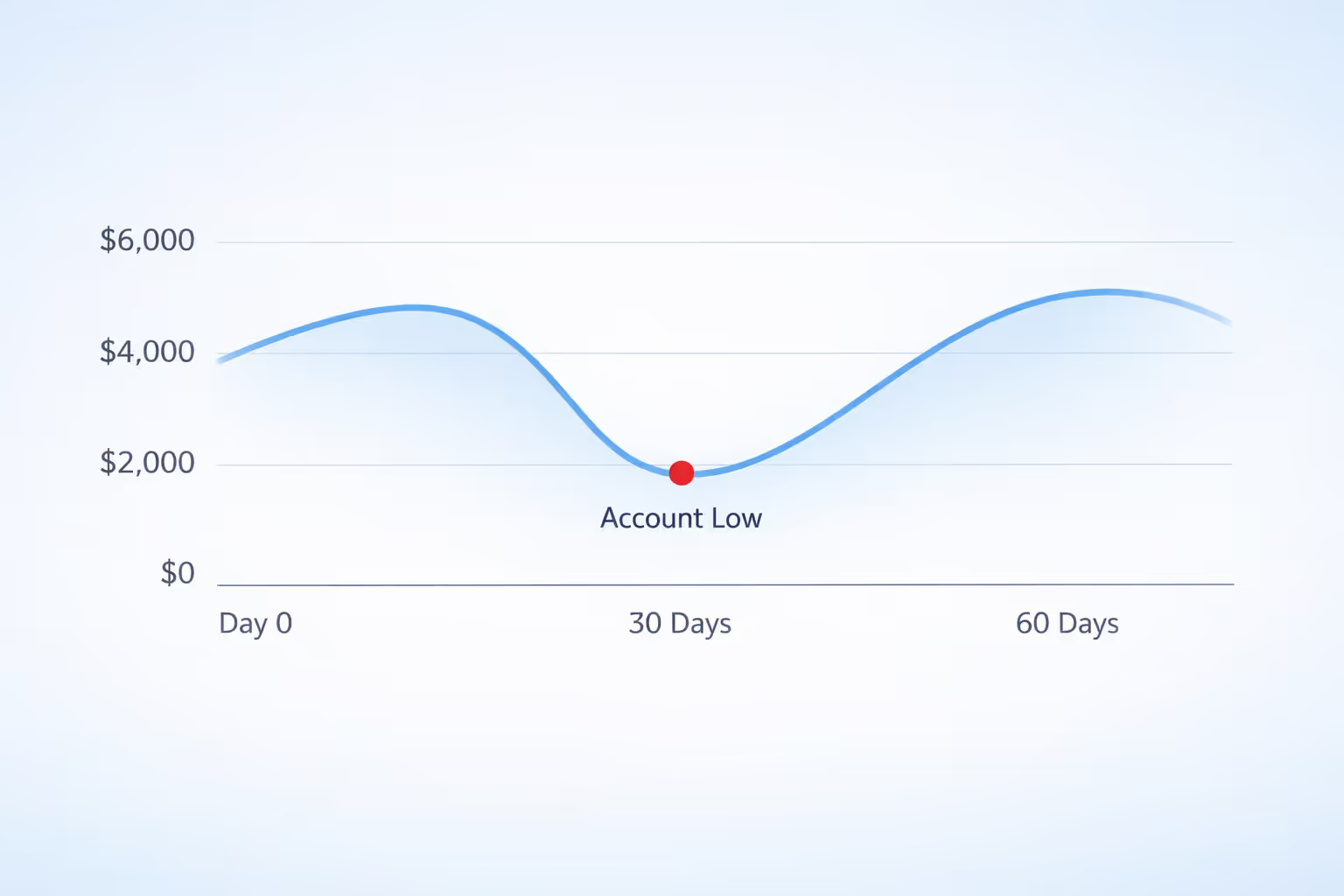

Account Low answers all three questions in one number. It's your projected minimum checking account balance over the next 2 months — the lowest point your balance will reach based on your scheduled income and expenses. It is the main output of Centinel’s checking account forecast: Centinel starts with today’s balance, walks the calendar forward through each known paycheck, bill, transfer, and credit card payment, and identifies the lowest projected balance along the way. This article focuses on Account Low itself — what the number means, why it matters, and why it is deliberately conservative.

Account Low is the projected minimum checking account balance you'll reach within the next w months. More precisely: it's the lowest point your balance hits when Centinel simulates forward through every scheduled income and expense event.

That makes it a worst-case figure for your forecast period — the tightest day. It answers one specific question: is your current balance, plus your scheduled income, enough to cover your upcoming expenses? If Account Low is positive, the answer is yes — you'll stay above $0 through every day of the next 2 months. If it's negative, the answer is no, and the number tells you exactly how short you'll be at your worst point.

[Keep Table].

Centinel calculates Account Low by walking through your account day by day across the 2-month forecast horizon, applying each scheduled event on its expected date and tracking the lowest balance reached along the way. But there's one specific design choice inside the simulation that shapes what the resulting number actually means: when an income event and an expense event both fall on the same day, Centinel applies the expense first.

That's the conservative same-day timing assumption, and it's the reason Account Low is a worst-case figure rather than a best-guess. The reason has to do with how banks actually process transactions.

Suppose you start a day with $1,000 in your account. During that day, your $2,000 paycheck is deposited and your $1,500 rent payment posts. By the end of the day, your balance should logically be $1,500 — and you should never go negative, because the paycheck more than covers the rent.

But banks don't process transactions in real time. They process them in batches, and they have discretion over the order within each batch. If your bank applies the $1,500 debit before the $2,000 credit, your balance temporarily drops below $0 before recovering:

That momentary dip is enough to trigger a $35 overdraft fee. You ended the day with plenty of money. You technically had the funds to cover the rent. But you wake up the next morning to a balance of $465 instead of $500, because your bank charged you for a transaction order you had no control over.

This is the scenario the conservative assumption protects against. By assuming debits always post before credits on any given day, Account Low reflects the lowest balance your account would reach under the worst possible posting order — not the best, not the average. If Account Low shows a positive number, you can be confident the account stays positive regardless of how your bank chooses to sequence transactions on the constrained day. If it shows a negative number, you're being warned about a shortfall that's certain rather than one that depends on lucky timing.

The alternative — assuming credits post first — would produce a more optimistic Account Low that sometimes turns out to be wrong in the user's favor and sometimes wrong against them. A forecast that's occasionally too pessimistic is far more useful than one that's occasionally too optimistic, because the consequences of being wrong in the costly direction (overdraft fees, declined transactions) are much worse than the consequences of being wrong in the safe direction (slightly more cash on hand than expected). Conservative-by-design means Account Low is a number you can act on, not a number you have to hedge against.

Whether Account Low is positive or negative changes what the number is telling you.

A positive Account Low is an opportunity signal. It represents money that isn't needed to cover your scheduled obligations over the forecast period — cash that's genuinely available rather than already committed. But Account Low is not the final spendable amount by itself. It is the starting point for figuring out how much of your checking balance is actually safe to spend.

A negative Account Low is a risk signal. It's telling you that at some point in the next 2 months, given your current trajectory, the account will overdraft or breach the minimum you want to keep in your checking account. The magnitude tells you how short you'll be at the worst point — which is also the amount that, if deposited now, would clear the shortfall everywhere in the window.

Account Low compresses the next 2 months of your account into a single worst-case number. The conservative same-day assumption is what makes it a number to act on rather than one to hedge against. If Account Low says you're safe, you're safe even on the worst posting day. If it says you’re not, the issue is visible in your scheduled cash flow — and you have time to act before the low point arrives.

STAY A STEP AHEAD