Build a checking account cash flow forecast in 5 steps to see whether you’re at risk of overdraft or have cash that’s safe to spend.

January 4, 2026

Most people manage their checking account the same way: glance at the balance, and hope. The balance tells you what's there right now; it says nothing about whether that money survives the rent, the car payment, and the credit card bill still coming before payday. A checking account cash flow forecast answers that question — it projects your balance forward day by day, so you can see whether you’re headed toward an overdraft or have money that is genuinely safe to spend or move.

You can build one two ways: by hand in a spreadsheet, or with an app that runs it for you. This guide covers the manual method — the 5 steps from a current balance to a number you can act on. The arithmetic is simple. The work is in being complete and keeping it current.

Every forecast, manual or automated, runs on the same three things: your current balance, your scheduled cash flow events, and a planning window — how far ahead you look. 2 months is the practical sweet spot, far enough to catch the bills that cause trouble and near enough that the projection stays reliable. The steps below are the work of populating those inputs and letting the arithmetic run.

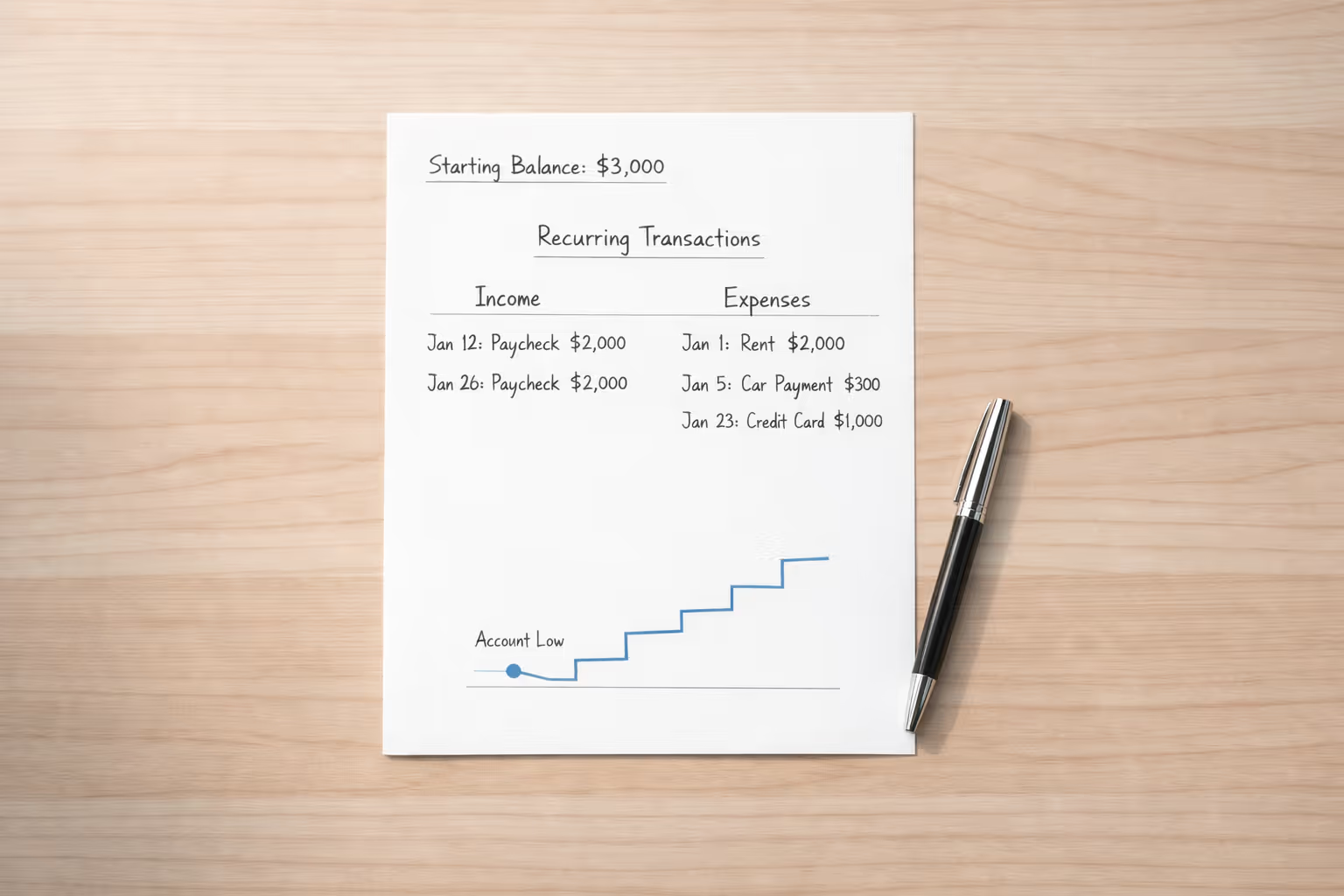

Log into your bank and record your exact balance right now, with the date. Don't round, don't work from memory, and don't reuse a number from a few days ago unless you're certain nothing has posted since. Every projection builds on this figure, which makes a stale starting balance the most common reason a manual forecast drifts from reality — not the math, the anchor.

This is the effortful part, and the part that decides whether the forecast is worth anything. You're capturing every money movement you expect over the next 2 months, of two different kinds. Recurring events are the patterns: a paycheck every other Friday, rent on the 1st, the car payment on the 10th, utilities scattered through the month. One-time events are the known exceptions: a tax refund next month, a bonus, a Venmo to a friend. For each, note what it is, whether it's income or an expense, the date, the frequency, and the amount.

Most people undercount, and the damage comes from the items that don't surface easily — a quarterly premium, an annual renewal — because a forecast missing an expense shows more safety than you actually have. The reliable method is to list everything from memory, then check that list against the last few months of statements to catch what memory left out.

Now run it. Starting from your current balance, move forward one day at a time, adding income and subtracting expenses on the dates they land, and write down the running balance as you go. The lowest point that balance reaches anywhere in the window is your Account Low — the single most useful number the forecast produces, because it marks the moment you're closest to trouble.

Here is a two-week slice of an account that starts at $2,400:

Notice where the tightest point is: March 5th, not the start and not the end. The balance bottoms out at $880 before the paycheck on the 7th lifts it back up. That is the entire value of walking it forward — on March 1st you see $2,400 and feel flush, but the actual lowest point of the period is $880, four days out, and your balance alone never tells you that.

Account Low tells you the low point. Your Floor tells you whether that low point is comfortable. The Floor is the minimum balance you don't want to drop below — $0 if you only care about avoiding an actual overdraft, higher if you want a cushion for the unexpected. It's a personal number: stable income and an accessible emergency fund justify a lower one; variable income justifies a higher one. Setting it deliberately rather than guessing is the whole question of how much to keep in your checking account.

With both numbers, what's safe to move out is straightforward: Available Cash = Account Low − Floor. In the example, an $880 Account Low against a $500 Floor leaves $380 you could move to savings or debt while still clearing every obligation in the window. Moving money out today lowers the entire curve, including the low point — so the deployable figure is anchored to your tightest moment, not your current one.

Once it's built, read it against what you already know. Does the trajectory look right? Do the big events land on the dates you expect? Does the Account Low match where your tight spots actually fall? If it shows more room than feels real, trust the instinct and look for what's missing — a forgotten expense, a wrong amount, a misdated event. A forecast only knows what you tell it.

Building the forecast once is the easy part. Keeping it accurate is the real commitment, and it's where the manual method shows its cost. The balance has to stay current — a forecast built Monday on $3,000 is wrong by Friday if you're actually at $2,000. Amounts change, new expenses get added, a raise shifts the whole structure. None of it is hard. It's just relentless, and the danger isn't the effort but the gap between checks: the longer you go without updating, the longer a discrepancy hides, and the less time you have to react to a shortfall you can no longer see coming.

This is the trade an automated tool makes for you. Centinel refreshes your balance daily through a read-only connection, pulls credit card statements as they close, and surfaces discrepancies within a day instead of weeks — then alerts you when the forecast projects a dip below $0 or your Floor. You still supply what only you can know: one-time events, changes in circumstance. But the mechanical upkeep that quietly corrupts a manual forecast runs on its own.

However you keep it, you now have what managing by balance never gives you — a view forward instead of a snapshot back. When a large expense is coming, you see it first. When you wonder whether you can move money to savings, Account Low minus Floor answers it.

That is the whole point of forecasting your checking account: not predicting the future for its own sake, but acting on the information it gives you. If maintaining it by hand sounds like more than you want to take on, that's what Centinel is built to do for you.

STAY A STEP AHEAD