The same framework Fortune 500 teams use to manage cash — forecast, find the low point, deploy the surplus — works for your checking account.

March 10, 2026

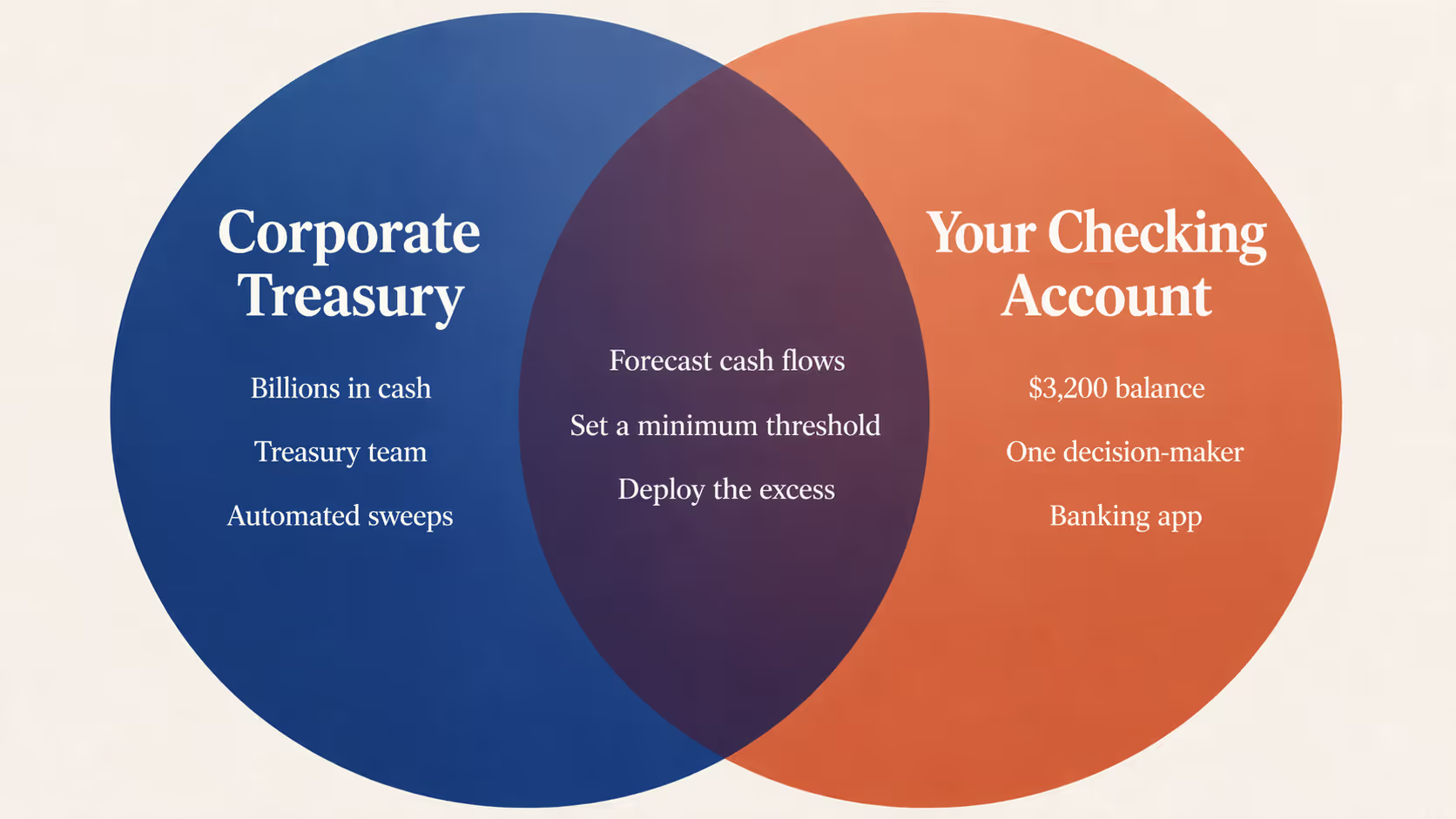

Corporate treasurers and you have the same problem. Theirs is measured in billions; yours, in the $3,200 sitting in your checking account. Some of that money is committed — to rent, car payments, credit card bills due next week — and some of it is surplus that could be working harder somewhere else. The job, in both cases, is knowing which dollars are which.

Corporate finance teams solved this with a three-move framework: forecast your cash flows, set the minimum balance you need on hand, and put everything above it to work. The framework exists because guessing is expensive. Hold too much cash and you're letting money sit that could be growing. Hold too little and you can't cover what you owe. The same two failure modes apply to a checking account, and most people default to the first — leaving money idle — because the second failure (an overdraft, a bounced payment) is visible and embarrassing. Idle cash is just invisible. But it still costs you.

The rest of this article walks through how corporate treasurers apply this framework, why it translates cleanly to a $3,200 balance, and what has to change when you move from a finance team with modeling software to a consumer trying to make sense of their financial life.

A corporate treasurer navigates between two failure modes. Running short means missing payroll, defaulting on a vendor payment, or violating a debt covenant. Holding too much means leaving cash idle in an operating account when it could be earning returns elsewhere. A treasurer who runs short is in crisis. A treasurer who routinely leaves millions earning zero overnight is considered incompetent. Both sides cost the company money.

Treasurers address both with the same three-part framework. First, they forecast cash flows — projecting known inflows and outflows day by day to turn the coming weeks into a visible balance trajectory rather than a guess. Second, they set a target balance — the minimum the operating account should carry to absorb variability and meet obligations without incident. This is a deliberate policy decision informed by cash flow volatility, risk tolerance, and the cost of a mistake. Third, they deploy the excess. Anything sitting above the target gets moved automatically into higher-yield vehicles — money market funds, short-term investments, or applied against a line of credit — typically through a daily sweep that runs at the close of each business day. Forecast, threshold, deploy.

The three moves serve one governing principle: idle cash is a cost, and surprise shortfalls are a crisis. A treasurer who protects against one while ignoring the other isn't doing the job.

The framework translates directly. Forecast your checking balance forward. Set a minimum you want to maintain. Deploy whatever sits above that minimum. The scale is different and the mechanism is different, but the underlying logic is identical.

Here's how each element maps:

Two of these deserve unpacking because they're where the framework actually becomes useful. Account Low is the lowest your checking balance is projected to reach over the next 2 months, and it's doing double duty as both a protection signal and an optimization signal. If it's negative, you're heading for an overdraft — and because the forecast runs 2 months out, you see it coming with enough time to fix it. If it's positive, it tells you exactly how much buffer you have at your most vulnerable point, which is far more useful than your current balance, because your current balance still includes money that's already committed. Available Cash is Account Low minus your Floor. It's the amount you can move to a high-yield savings account, pay down a credit card, or invest, knowing that even at your worst projected moment, you'll remain above your personal minimum. Acting on that number is the core of checking account optimization and knowing how much is safe to spend — and until you have it, every "should I move money?" decision is a guess.

The gap between corporate and consumer behavior isn't sophistication. It's information. A corporate treasurer has three things a consumer doesn't: a forecast showing what's coming, a defined minimum balance, and a mechanism to act on the difference. With those inputs, the decision is mechanical on both sides — avoid shortfalls, deploy the excess. Without them, both sides become a guess, and the rational response to uncertainty is to keep more than you probably need. The conservatism isn't irrational. It's the only sensible response to an information vacuum.

The problem is that the conservatism doesn't actually solve either side. It costs money on the low end and on the high end simultaneously. On the low end: overdraft fees that average north of $30 per incident, late payment fees on credit cards, and the compounding damage of a missed payment hitting your credit report — all of which happen because you couldn't see the shortfall coming, not because you didn't have the cash. On the high end: the average American household keeps thousands more in checking than their cash flow requires, earning around 0.07% APY when high-yield savings pay 4% or more. On a $5,000 idle balance, that's roughly $200 a year in foregone interest — a hidden cost that compounds quietly because no one experiences it as a loss. You never see the interest you didn't earn.

Both costs come from the same vacuum. You can't optimize what you can't see, and you can't protect yourself from a shortfall you didn't know was coming.

Centinel operationalizes this framework for consumers. It forecasts your balance forward through every upcoming paycheck, bill, and recurring charge. It identifies your Account Low and compares that to your Floor, the personal minimum you choose to maintain. And the difference becomes your Available Cash: the exact amount you can deploy without risking a shortfall at your most vulnerable moment in the forecast, and the earliest warning you'll get if a shortfall is coming. One integrated output replaces the treasurer's forecast-plus-sweep workflow — and does it in a way that keeps you in control of your money.

The principles are inherited from decades of corporate practice. The mechanism is built for consumer scale. And the reason it hasn't existed before comes down to three specific gaps. First, consumer finance tools evolved from the budgeting tradition — Mint, Monarch, and their descendants asked "where did my money go?" rather than "where is my money going, and when?" Those are different questions that require different data models. Second, the infrastructure consumers need — programmatic, near-real-time access to their own transaction data — only became reliable with the maturation of open banking APIs in the last several years. Third, the framing itself is new: the personal finance conversation has been organized around budgeting, saving rates, and investing strategy, not around the treasury question of how much cash to hold and where the rest should go.

The framework works regardless of the tool. Forecasting your balance forward, setting a deliberate minimum, and deploying the surplus above it isn't a corporate luxury. It's the same logic Fortune 500 treasurers have used for decades to prevent shortfalls and put cash to work — and the only reason it hasn't been available to you is that nobody had built the tool. Now it exists.

STAY A STEP AHEAD