Most advice says 1-2 months of expenses. The right number is smaller — and it's a floor you stay above, not a balance you park.

January 25, 2026

Ask how much to keep in your checking account and you'll get a consistent answer: 1-2 months of essential expenses, plus a small cushion. It's the number your bank gives you, the number a quick search returns, the number most advice converges on. For a checking account specifically, it's both more than you need and the wrong kind of answer. The right number is smaller — and more importantly, it isn't a number you park. It's a line you stay above.

That's two claims, and the second one matters more than it sounds. Most advice treats the figure as static: “hold $10,000 and you're done.” But a checking account isn't static. It's an operating account — money lands on certain days, bills leave on others, and the balance rises and falls in between. So the useful question isn't "what number should sit here?" It's "what's the minimum I need to stay above, and am I on track to stay above it?"

The 1-2-months figure isn't wrong so much as it's answering a different question than the one you're asking about checking specifically. The reason it sounds large is because it quietly bundles two jobs your money does into a single number.

The first job is an operating buffer: the cushion that absorbs ordinary timing mismatches between when income arrives and when bills come due. This is genuinely a checking-account function; it's what keeps a Tuesday rent payment from clipping you when payday is Friday.

The second job is an emergency fund: the reserve that absorbs shocks like a job loss, a medical bill, or a major repair. The standard guidance is 3-6 months of expenses. That money needs to be accessible, but it does not need to sit in the account that pays daily bills. In most cases, it can sit in a separate savings account, earn more while it waits, and be transferred back to checking if the need actually arises.

Conventional advice folds the second into the first, which is why "keep 1-2 months of expenses in checking plus a small cushion" comes out so high. Pull them apart, and only the operating buffer actually needs to live in your checking account. The emergency reserve can — and should — sit somewhere where it works harder.

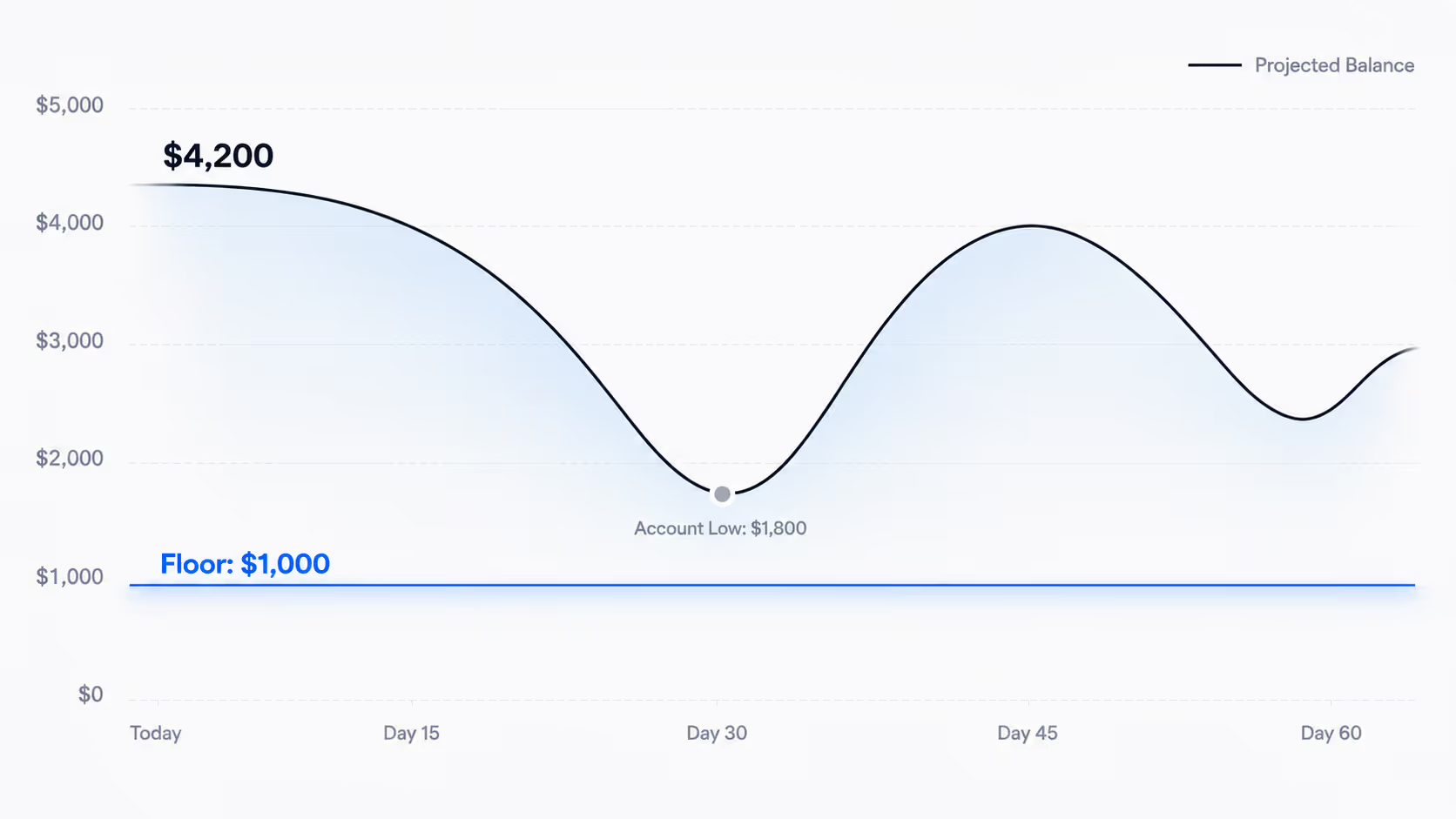

Once you've separated the two jobs, the right question for your checking account comes into focus. It isn't "how much should I park here?" It's "what's the lowest I'm willing to let my account reach — and am I going to stay above it?" That minimum is your Floor: a target minimum balance, the lowest point you'll allow before you'd act.

The difference from parking is the second half of that question. Parking asks whether your balance clears the line today. A Floor asks whether it clears the line through everything coming over the next two months — rent, payday, the credit card bill, all of it. You can sit comfortably above your Floor today and still be projected to breach it next Tuesday, when rent lands before your paycheck does. So a Floor only means something if you can see those movements coming, which means projecting your balance forward through everything you know is arriving and leaving — a checking account cash flow forecast.

With that projection in hand, your Floor works in two directions: it warns you when your balance is projected to dip below it, with enough lead time to move money or delay a discretionary expense — and it shows you what sits above it. Anything consistently above your Floor isn't claimed by your obligations or your buffer, which makes it what's safe to spend or move somewhere it earns more. This is the same logic corporate treasury teams use to run operating cash: don't manage to a static balance, manage to a minimum you stay above. The scale changes; the method doesn't.

A concrete starting point: 1-2 weeks of essential expenses — the obligations that have to be paid no matter what, like rent or mortgage, utilities, minimum debt payments, insurance, and groceries. It's smaller than the conventional figure for one specific reason: the emergency fund that inflates the usual advice is living somewhere else now. From there, adjust along three dimensions.

A steady salary on predictable dates with bills on autopay means predictable cash flow — you can run a lower Floor because you know almost exactly what's coming and when. Variable income (freelance, commission, gig, seasonal) or lumpy expenses mean you need a higher Floor to bridge the gaps you can't time precisely.

If you have a healthy emergency reserve you can reach quickly, your Floor can be lean, because the shocks have their own backstop. If you don't yet, your checking Floor has to do double duty for now — set it higher until that separate reserve exists, then bring it back down.

Some people sleep better with more margin; others are comfortable running lean and putting every spare dollar to work. Neither is wrong. The honest test: at what balance would you start checking the account nervously, and at what balance would you feel fine? Your Floor lives in between.

Begin at 1-2 weeks of essential expenses. Add a week if your income is variable. Add another week or two if you don't yet have a separate emergency fund. Round up if you're risk-averse, down if you have fast access to backup funds. The point isn't precision — it's setting the number deliberately instead of carrying a vague sense of "enough." You can always adjust.

The right amount to keep in your checking account is roughly one to two weeks of essential expenses. But the number is only half of it. Setting it puts you in the right range; holding it as a line you stay above, rather than a balance you park, is what makes the number do any work. It's the difference between watching the road through the windshield and checking it in the rearview mirror — both show you the road, but only one shows you what's ahead.

Most guidance lands on 1-2 months of essential expenses, but that figure is high because it bundles in an emergency fund. The amount that actually needs to sit in checking — your operating buffer — is smaller, closer to 1-2 weeks of essentials, with the emergency reserve held separately.

It's not risky, but it's inefficient. Checking accounts pay little to no interest, so cash sitting well above your Floor is losing ground to inflation and to what it could earn elsewhere. Once you’ve identified a reliable surplus, you can decide what to do with extra money in your checking account instead of letting it sit idle: build emergency savings, pay down high-interest debt, or move it to investments.

No. An emergency fund does a different job than your checking buffer and sits on a different time horizon, so it belongs in a separate account — typically a high-yield savings account — where it stays accessible but earns meaningfully more than it would in checking.

This article is for informational purposes and reflects one approach to managing your checking account. It's not financial advice, and your situation may require different considerations. When in doubt, consult a financial professional.

STAY A STEP AHEAD