Learn how to prevent overdrafts with a hierarchy of strategies—from balance alerts to cash flow forecasting.

March 6, 2026

Most overdraft prevention advice boils down to the same handful of tips: check your balance, set up alerts, keep a cushion in your account. That advice isn't wrong — it's just incomplete. It treats overdrafts as a behavior problem, as if the solution is simply paying closer attention. But for the millions of Americans who overdraft each year—paying an average of $26.77 per occurrence and collectively losing billions annually—the issue usually isn't carelessness. It's visibility.

You didn't overspend. You couldn't see what was coming.

The mechanics behind overdraft fees are more complex than most people realize — cascading charges, posting order effects, and a system that can turn one missed timing into three or four separate fees. But the trigger is usually simpler than the mechanics. An overdraft happens when your checking account balance drops below zero, typically because income and expenses landed on the wrong days relative to each other. Your paycheck arrives on Friday but rent clears on Wednesday. Three automatic payments stack up on the same day your account was already running thin. The problem isn't how much you earn or spend. It's that you couldn't see the collision in advance.

The most effective way to prevent an overdraft is to forecast your checking account balance forward, day by day, so you can see a potential shortfall days or weeks before it happens — and take action while you still have time.

This article presents overdraft prevention as a hierarchy — five levels, from the most reactive to the most proactive. Each level adds lead time: the amount of warning you get before an overdraft hits. The higher you go, the more time you have to respond — and the less likely you are to need a safety net at all.

If you've ever searched for advice on avoiding overdraft fees, you've probably encountered some version of this list: check your balance regularly, keep a buffer in your account, sign up for balance alerts, link a savings account for overdraft protection. These are the standard recommendations from banks, regulators, and personal finance sites—and every one of them has a meaningful limitation.

Checking your balance is a snapshot. It tells you where you are right now, not where you'll be on Thursday when rent, your car insurance, and a credit card payment all hit within hours of each other. It's a rear-view mirror in a situation that requires a windshield.

Keeping a buffer assumes you have surplus cash available to set aside. For many households—particularly those on biweekly or irregular pay cycles—there isn't a reliable surplus to buffer with. The money is there; it just doesn't always arrive before it's needed.

Low-balance alerts are better, but they fire when your balance is already low. By the time you get the notification, the overdraft may be hours away rather than days. And the alert tells you the number is low without explaining why—you still have to piece together which upcoming transactions are about to make things worse.

Overdraft protection (linking a savings account or credit line) is a safety net, not a solution. The overdraft still effectively happens—your checking account goes negative—and a transfer covers it. You avoid the full fee, but you haven't addressed the underlying timing problem.

None of these methods are bad. But they all share the same fundamental limitation: they're reactive. They respond to a problem that's already arrived or is about to. What they can't do is show you today that a week from now there’s going to be a problem, which is while you still have time to do something about it.

That's the gap the hierarchy below is designed to address.

Each level below adds more lead time between you and a potential overdraft. Level 1 gives you a real-time view of today. Level 5 gives you a 30-60 day forward look. Where you choose to operate on this spectrum depends on how much visibility you want—and how actively you want to manage your money.

This is the most basic prevention step, and it's one that most people either skip or do incorrectly.

The key distinction here is between your account balance (also called your ledger balance) and your available balance. Your account balance shows transactions that have officially posted. Your available balance subtracts pending transactions—charges your bank has authorized but hasn't fully processed yet—and accounts for any holds on recent deposits. Your bank evaluates overdrafts against your available balance, which means you can see a positive number in your app and still overdraft if pending transactions haven't been reflected in the figure you're looking at.

Getting in the habit of checking your available balance—not just glancing at the number on your home screen—is a genuine improvement over not checking at all. But it's still a snapshot. It tells you where you stand right now, not what's coming. If you have $300 available today and a $400 car insurance payment is scheduled to hit in two days, today's balance won't warn you. You need to carry that information in your head, which is exactly the kind of thing that's easy to forget when life gets busy.

Lead time: Zero. You see where you are, not where you're going.

Most banks and credit unions let you configure alerts—via text, email, or push notification—that fire when your available balance drops below a threshold you set. This is a meaningful step up from manual checking because it comes to you rather than requiring you to remember to look.

Set your alert threshold high enough to give yourself a useful warning. If your largest single expense is a $1,200 rent payment, an alert at $100 isn't helpful—by then, the damage is already done or imminent. A threshold closer to $1,500 or $2,000 gives you more room to react.

The limitation is that alerts are backward-looking by nature. The alert fires because your balance has already dropped, not because it's about to drop. And the alert doesn't tell you what's coming next. You might get a notification that you're at $500, which feels manageable—until you remember that three automatic payments totaling $450 are scheduled for tomorrow. The alert gave you a data point, but not the context around it.

Lead time: Hours, maybe a day. Better than nothing, but often not enough to rearrange your cash flow.

This is where most banks steer the conversation: link a savings account, money market account, or line of credit to your checking account so that if a transaction would take your balance below zero, the bank automatically pulls from the linked account to cover it.

It works. If you have money elsewhere, the transfer happens seamlessly, and you avoid the full overdraft fee. But it's worth understanding what this approach actually is and isn't.

Overdraft protection is protection, not prevention. The overdraft still happens in the mechanical sense—your checking balance goes negative—and the linked account bails you out. Some banks charge a transfer fee (typically $10–$12.50 per transfer, though many have eliminated this fee in recent years). If the linked account is a line of credit, you'll pay interest on the amount advanced. And if the linked account doesn't have enough to cover the shortfall, you're back to a standard overdraft with its standard fee.

This approach also assumes you have funds available in another account. If your savings account is thin—or if you don't have a savings account at all—overdraft protection isn't an option. It's a safety net designed for people who have money elsewhere but occasionally mistime their checking account. That's a real scenario, but it's not the only one.

This approach is a safety net, not a solution—a form of overdraft protection, not overdraft prevention—covering the immediate shortfall without addressing the underlying timing problem.

Lead time: None. It's a safety net, not an early warning system. The overdraft happens; you just don't pay the full fee.

This is a different kind of prevention—it eliminates one entire category of overdraft risk by telling your bank to decline debit card and ATM transactions that would take your balance below zero. No transaction, no fee.

Under federal Regulation E rules that took effect in 2010, your bank can't charge you an overdraft fee on debit card purchases or ATM withdrawals unless you've opted in to their overdraft coverage program. If you haven't opted in (or if you opt out), those transactions get declined instead of covered. It's less convenient—your card gets declined at the register—but it's free.

The critical limitation: opting out only covers debit card and ATM transactions. It does not apply to checks or ACH payments—which include rent, mortgage, car payments, insurance, utilities, and most other recurring bills. These are typically the largest transactions hitting your checking account, and they're exactly the ones where opting out provides no protection. Your bank can still pay or return them at its discretion and charge you accordingly.

Opting out is a worthwhile step for removing unnecessary fee exposure on discretionary spending, but it doesn't address the transactions that most commonly cause serious overdraft problems.

Lead time: Instantaneous for debit transactions, but irrelevant for the biggest risks. It's a partial shield, not a complete solution.

This is the most proactive approach to overdraft prevention—and the one that none of the standard advice covers.

Instead of looking at your balance today and trying to remember what's coming, you project your balance forward day by day: start with today's balance, then add every expected deposit and subtract every expected expense on the date each is scheduled to occur, for the next 30-60 days. The result is a timeline of your future checking account balance—a curve that shows exactly when your account will rise, when it will dip, and whether it's projected to cross zero at any point. The effectiveness of that projection depends entirely on the completeness of its inputs — every recurring transaction you miss is a withdrawal or deposit your forecast doesn't know about, which means a potential shortfall it can't warn you about.

This is the concept behind checking account cash flow forecasting. It turns a potential overdraft from an invisible surprise into a visible event on your timeline—something you can see and respond to with days or even weeks of lead time.

That lead time changes everything. When you can see that your balance is projected to dip below zero next Tuesday, you have options that simply don't exist when you find out the day it happens: move a bill payment date, transfer funds from savings before you need them (proactively, rather than reactively through overdraft protection), adjust a discretionary purchase, pick up extra hours, or contact a biller to request a different due date. The point is that you're making a decision with time and information, not scrambling after the fact.

The core insight is that most overdrafts aren't caused by insufficient income—they're caused by timing collisions between income and expenses. Your paycheck covers your bills over the course of a month, but it doesn't always cover them on the exact days they're due. Forecasting makes those collisions visible before they cost you money.

That visibility is only as reliable as the forecast producing it — a stale starting balance or a missed expense means the shortfall may not appear on your timeline, and you're back to being surprised by an overdraft you could have seen coming, which is why maintaining an accurate forecast is essential to making Level 5 actually work.

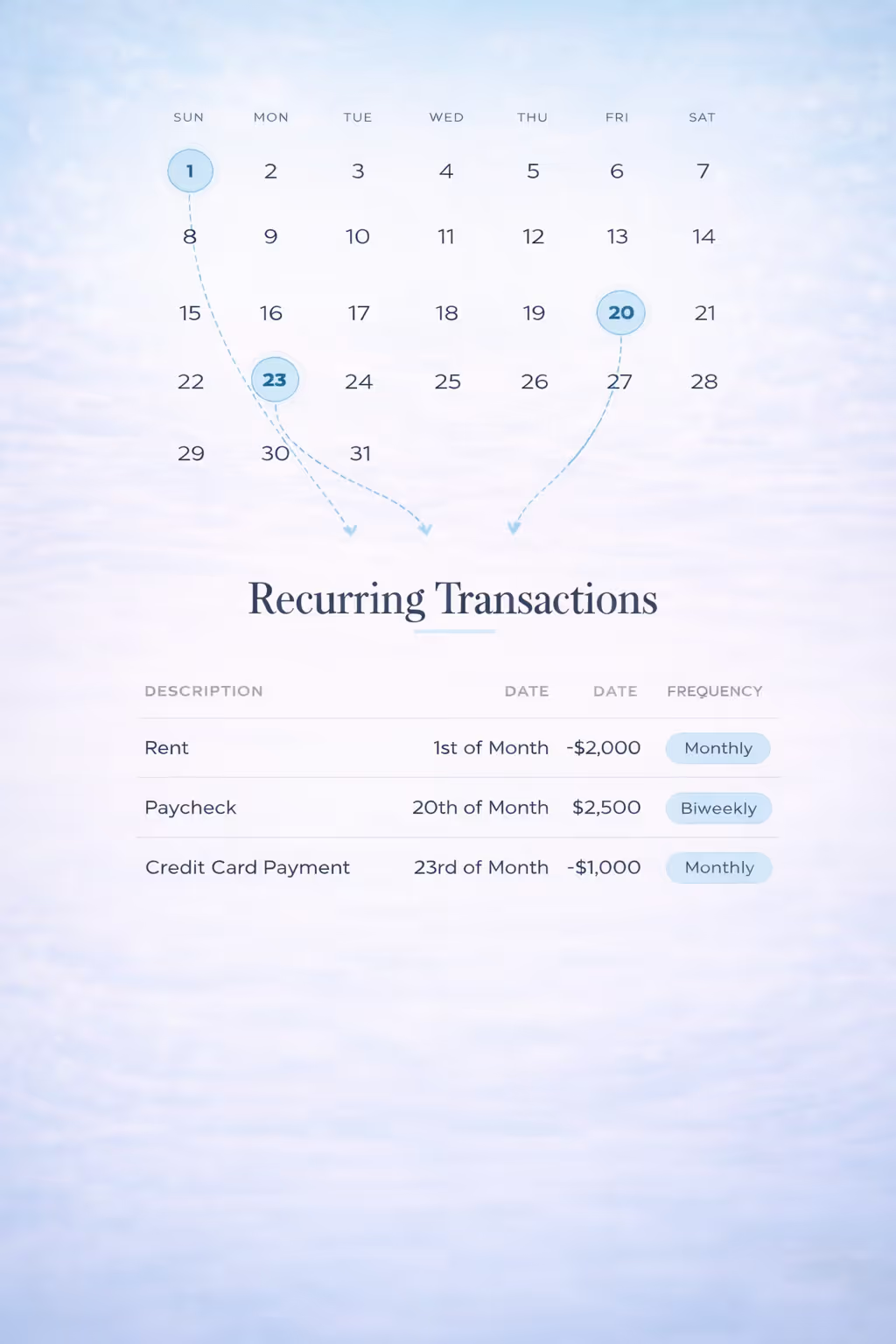

There are several ways to build and maintain a forecast. You can do it entirely on your own with a spreadsheet—our step-by-step guide walks you through the process. If you want a more visual, purpose-built tool, Centinel's free Starter plan works like a smarter spreadsheet designed specifically for checking account forecasting—you enter your income and expenses, set your minimum balance (what Centinel calls your "Floor"), and get a 60-day forward view of your balance with clear indicators of available cash or projected risk. And if you'd rather have more automation, Centinel's Premium plan connects to your bank account via Plaid, detects your recurring transactions, and updates your forecast automatically each day—flagging projected shortfalls before they arrive.

Lead time: Days to weeks to months. You see the problem before it exists, with enough time to prevent it entirely.

The right level for you depends less on how often you overdraft and more on how much visibility you want into your money.

If you prefer a set-it-and-forget-it approach, Levels 2 through 4—alerts, overdraft protection, and opting out—create a reasonable passive safety net. You won't always see what's coming, but you'll have guardrails in place for when things get tight.

If you want active visibility into your checking account—knowing not just your balance today but what it's projected to look like next Tuesday, or the day after rent and your car payment clear on the same morning—Level 5 gives you that window. You're no longer guessing whether you have enough to cover the next few weeks. You can see it.

For people managing biweekly paychecks against monthly bills, or anyone whose income and expenses don't always land on cooperative dates, forecasting addresses the root cause rather than the symptoms. It makes the timing mismatches that create overdraft risk visible and actionable—before they reach your account.

And the visibility that prevents overdrafts also surfaces opportunities. When you can see your projected balance over the next 60 days, you don't just see the dips—you see the peaks. Surplus cash you didn't realize was available. A window to move money into savings or make a purchase you'd been holding off on. Forecasting isn't just about avoiding bad days; it's about knowing what's actually available to you.

The difference between reacting to overdrafts and predicting them is the difference between checking your balance and forecasting it. Most prevention advice lives at Levels 1 through 4—reactive, limited in lead time, and focused on what's already happened or is about to. The opportunity is at Level 5, where you're looking ahead instead of behind and predicting what’s to come.

Centinel was built for prevention: a daily 60-day forecast of your checking account that shows what's available, what's coming, and where the risk is—before it reaches your bank statement.

STAY A STEP AHEAD