Overdraft protection catches you after your balance goes negative. Overdraft prevention helps you see it coming and avoid it. Here's why the distinction matters.

March 6, 2026

Banks talk a lot about overdraft protection. Regulators talk about it. Personal finance sites review it, compare it, and rank it. What almost nobody talks about is the difference between overdraft protection and overdraft prevention—because the industry treats them as the same thing. They're not.

Protection is a seatbelt. It reduces the damage after the collision has already happened. Prevention is seeing the hazard ahead and steering around it—so the collision never occurs.

Most consumers have encountered some form of overdraft protection: a linked savings account, a line of credit, a grace period. These are real tools that serve a real purpose. But they all share a common trait that's easy to overlook—they activate after your balance has already gone negative. They manage the consequences of an overdraft. They don't stop it from happening.

Overdraft prevention is a different category entirely. It means seeing the overdraft coming—days or weeks in advance—and taking action while you still have time. No fee, no transfer, no safety net needed.

Overdraft protection transfers funds from a linked account after your balance goes negative, reducing the fee but not preventing the overdraft. Overdraft prevention identifies a potential shortfall days or weeks before it happens, giving you time to avoid it entirely.

This article draws the line between the two, explains why it matters, and makes the case that the most effective approach uses both—with prevention as your primary strategy and protection as your backup.

Overdraft protection comes in several forms, but they all work on the same basic principle: when your checking account balance drops below zero (or is about to), the bank intervenes to cover the shortfall. The intervention varies in cost and mechanism, but the timing is the same—it happens at the moment of overdraft, not before.

The most common form of overdraft protection. You connect a savings account, money market account, or secondary checking account to your primary checking account. When a transaction would push your balance negative, the bank automatically pulls funds from the linked account to cover it. Some banks charge $10–$12.50 per transfer, though many have eliminated this fee in recent years. The catch: you need money in the linked account for this to work, and each transfer quietly drains your savings.

These function like a small loan earmarked for overdrafts. When your balance goes negative, the bank advances funds from the credit line. You pay interest on whatever amount is advanced until you repay it. This avoids the flat overdraft fee, but introduces a different cost—one that's easy to ignore because it accrues gradually rather than showing up as a single charge on your statement.

This is what most people picture when they hear "overdraft fee." The bank pays the transaction on your behalf, your account goes negative, and you're charged a flat fee—currently averaging $26.77 per occurrence. You can opt in or out of this coverage for debit card and ATM transactions (under federal rules that took effect in 2010), but for checks and ACH payments—rent, utilities, car payments, insurance—the bank decides whether to pay or return them regardless of your opt-in status.

The newest category. Some banks now give you until the end of the next business day to bring your balance positive before charging a fee, or waive fees entirely on overdrafts below a small threshold (often $5 or $50). These are genuinely consumer-friendly improvements, but they're still reactive by design—they give you a few extra hours to respond to a problem that's already arrived.

What all four of these have in common is worth stating clearly: every form of overdraft protection responds to an overdraft that has already occurred or is in the process of occurring. They vary in cost, convenience, and how forgiving they are. But none of them give you advance warning. None of them help you see next Tuesday's problem on the previous Thursday. They're all seatbelts—good to have, but they only help after impact.

Americans pay over $12 billion a year in overdraft and NSF fees, and the burden falls disproportionately on households with tight cash flow and low balances. Overdraft protection solves the fee problem for individual transactions. You pay less—or nothing—when an overdraft happens. That's genuinely valuable. But it doesn't solve the visibility problem, which is the one that actually matters.

When you rely on protection, you don't know the overdraft is coming until it arrives. Your balance goes negative, the linked transfer fires, and you find out after the fact. The immediate crisis is handled, but nothing has changed about the underlying pattern. You still don't know what your balance will look like next week, or whether the same collision of income and expenses is going to repeat itself on the 15th, or the 1st, or the next time your pay cycle falls out of sync with your bills.

This is how overdraft protection can quietly become a crutch. If your linked savings account bails out your checking account every month, the protection is working as designed, but you're not preventing anything. You're automating the cleanup. Your savings erode by $50 or $100 each cycle, you never address the cash flow timing that keeps causing the problem, and the "protection" becomes a recurring cost you've simply stopped noticing.

The question isn't whether overdraft protection is useful. It is—genuinely. The question is whether it's sufficient on its own. For most people, it isn't, because it can't answer the one question that would prevent the overdraft from happening: what does my balance look like nine days from now?

Prevention means seeing the overdraft before it happens—far enough in advance that you can stop it rather than manage it.

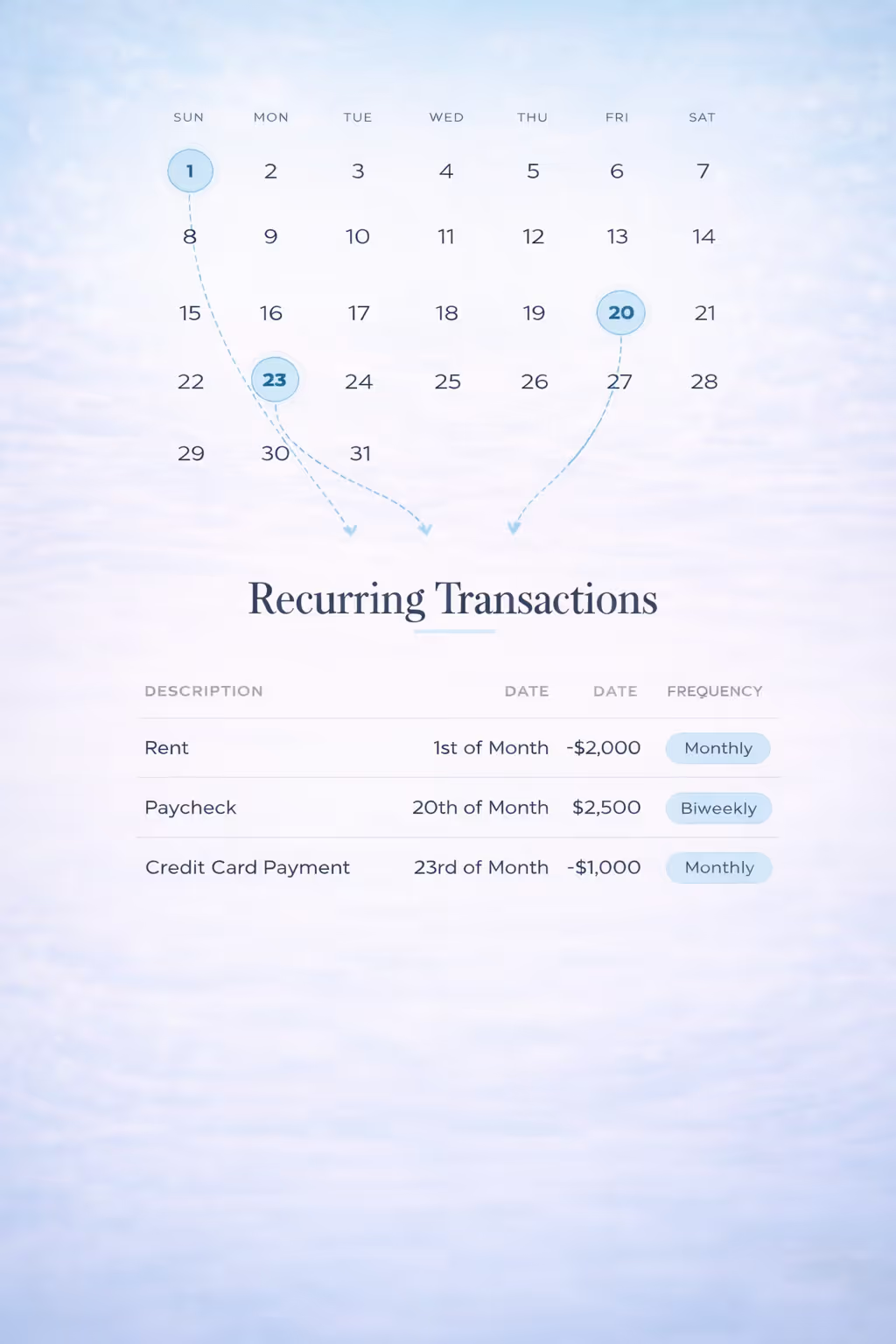

The mechanism is straightforward: instead of checking your balance today and hoping it's enough for the week ahead, you project your balance forward day by day. Start with today's balance, add every expected deposit on the date it's scheduled to arrive, subtract every expected expense on the date it's due to hit, and extend the timeline out 30 to 60 days. The result is a forward-looking view of your checking account—a trajectory that shows exactly where your balance rises, where it dips, and whether it's projected to cross zero at any point.

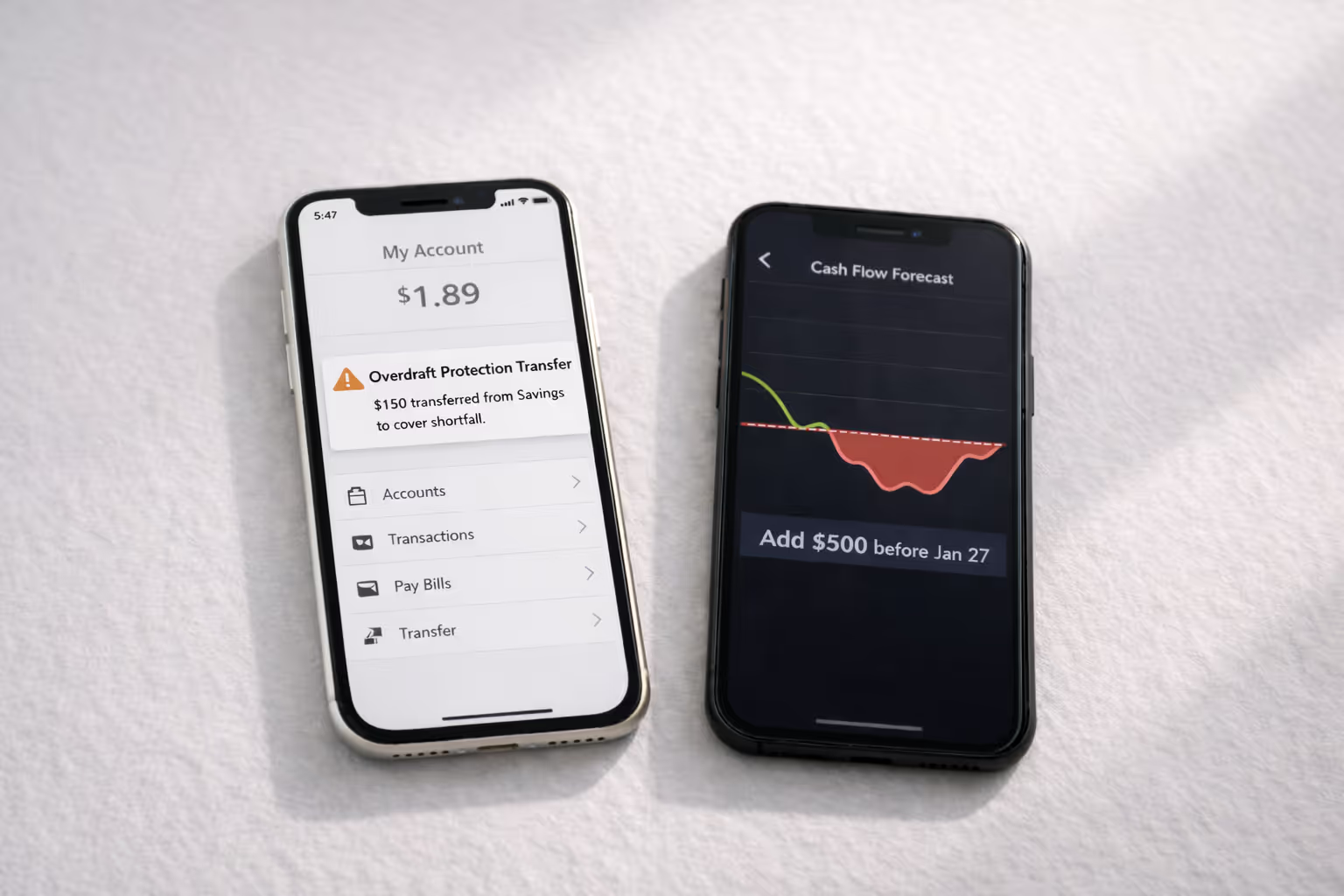

This is the core concept behind checking account cash flow forecasting. When you can see your balance trajectory over the next month or two, a potential overdraft shows up as a visible dip on the timeline—not as a surprise on your bank statement. And with that visibility comes something protection can never provide: lead time.

Lead time is what makes prevention fundamentally different from protection. When you can see that your balance is projected to go negative in two weeks—because rent and your credit card payment land on the same day, two days before your paycheck arrives—you have a range of options that simply don't exist in the moment of overdraft. You can move a bill payment date. Transfer funds from savings proactively rather than having the bank do it reactively. Adjust a discretionary purchase. Contact a biller about shifting your due date. You're making a calm, informed decision with days of runway, instead of discovering the problem after the fact.

The core insight is one that most overdraft advice misses entirely: the majority of overdrafts aren't caused by spending too much money. They're caused by timing collisions—income and expenses that don't land on cooperative days. Your paycheck covers your bills over the course of the month, but it doesn't always cover them on the exact days they're due. Forecasting makes those collisions visible before they cost you anything.

There are several ways to put this into practice. You can build a forecast manually in a spreadsheet—our step-by-step guide walks you through the process. If you want a purpose-built tool, Centinel's free Starter plan works like a smarter spreadsheet designed specifically for checking account forecasting: enter your income and expenses, set your Floor (your minimum comfortable balance), and get a 60-day forward view with clear indicators of surplus or risk. And if you'd rather not maintain it manually, Centinel's Premium plan connects to your bank via Plaid, detects your recurring transactions, and updates your forecast automatically each day—flagging projected shortfalls before they arrive.

The point of drawing this distinction isn't to argue that overdraft protection is bad. It's to argue that it's incomplete—and that most people are relying on it as their entire strategy when it was designed to be a backup.

Think of it as defensive driving. Nobody says "you don't need a seatbelt if you drive carefully." Everyone understands that you should do both. But everyone also understands that careful driving is the more important of the two—the seatbelt is there for the cases that careful driving couldn't prevent.

The same logic applies here. Prevention—seeing your cash flow forward and acting on what you see—is your primary strategy. It's what you rely on daily. Overdraft protection is your backup: the safety net that's there for the genuinely unexpected charge, the deposit that didn't clear when you expected, the edge case your forecast didn't anticipate. When prevention is working, your overdraft protection almost never activates. It becomes what it was always supposed to be—a safety net you rarely need, not a system you depend on every month.

If you're currently relying on protection alone, the shift to this layered approach starts with one thing: visibility into what's ahead—moving beyond reactive strategies like balance alerts toward predicting and preventing overdrafts before they reach your account.

Centinel was built around this distinction—a daily 60-day forecast that turns prevention from a concept into a daily practice. Keep your seatbelt on. But turn the headlights on too.

STAY A STEP AHEAD