Avoid overdraft fees by choosing a bank that doesn't charge them — or, if yours does, by layering two complementary strategies.

May 19, 2026

The most direct way to avoid overdraft fees is to use a bank that doesn't charge them — or, if yours does, by layering two complementary strategies: predictive strategies surface a potential shortfall in advance so you can act before your balance goes negative, and reactive strategies activate at or near the moment of crisis: covering the shortfall, intervening just before it, or declining the transaction so it doesn't occur..

Since 2021, a substantial number of banks and credit unions have eliminated overdraft fees entirely — either declining a transaction that would overdraw your account, or covering small shortfalls at no cost. This removes the fee completely and permanently, with nothing to manage. What it doesn't remove is the shortfall behind it: a declined rent payment, or a covered-but-still-negative balance, is a problem whether or not your bank charges $35 for it.

For everyone whose bank still charges — which includes most large banks — and for addressing the underlying shortfall regardless of where you bank, avoiding overdraft fees comes down to two structural approaches: predictive strategies that surface a potential shortfall in advance so you can act before your balance goes negative, and reactive strategies that activate at or near the moment of crisis: covering the shortfall, intervening just before it, or declining the transaction so it doesn't occur. The predictive category contains one option — forecasting your checking account cash flow forward. The reactive category contains several — bank overdraft protection, opting out of debit card overdraft coverage, and cash advance apps. Annual costs across these strategies range from $0 to over $300. The distinction between predictive and reactive matters because the categories differ not only in what they cost but in how they work — and in whether the underlying overdraft event happens at all.

This guide compares each strategy — beginning with bank choice, then the predictive and reactive approaches — across four elements: what it is, what it costs, what it requires, and what's worth knowing about how it actually performs in practice. Finally, it recommends a layered approach for avoiding overdraft fees entirely.

The strategies below assume a user who would otherwise incur 4 or 10 overdrafts in a year. The 4-overdraft column reflects a typical occasional overdrafter; the 10-overdraft column reflects a more frequent overdrafter. The CFPB has documented that roughly 9% of accounts incur 10 or more overdrafts annually, and that group accounts for nearly 80% of all overdraft fees paid.

Without any strategy in place, the baseline cost is the overdraft fees themselves: at the $35 average per overdraft charged by most large banks, a user who overdrafts 4 times annually pays $140; a user who overdrafts 10 times pays $350. The strategies in the table below should be evaluated against that baseline.

¹ Pricing reflects Centinel's annual plan at $59.99/year ($4.99/month billed annually) or $6.99/month on monthly billing.

² Range reflects variation across major banks. Chase, Wells Fargo, Capital One, and Citibank have eliminated transfer fees entirely; some smaller banks still charge $10-$12 per transfer. Overdraft lines of credit accrue interest at the account's rate (typically 18-21% on standalone overdraft lines, higher for credit-card-linked protection).

³ Range reflects residual overdraft costs from checks and ACH transactions, which the strategy does not cover. The cost is borne in those non-debit overdrafts.

⁴ Range reflects variation across subscription-model apps, per-advance models, and tip-based models at 2026 published pricing.

What it is. The most direct way to eliminate overdraft fees is to bank with an institution that doesn't charge them. A substantial number of banks and credit unions have done away with overdraft fees entirely. These institutions handle a shortfall in one of two ways: they decline the transaction outright, so no negative balance occurs, or they cover small shortfalls at no charge. Several large banks that still charge fees also offer a no-fee checking account within their lineup. Even as institutions eliminate overdraft fees, overdraft fee structures still vary significantly by bank.

What it costs. Nothing in overdraft fees. The cost is the friction of switching: opening a new account, moving your direct deposit, and re-pointing automatic payments and transfers. Some no-fee accounts carry secondary tradeoffs worth weighing, such as a smaller free-ATM network, lower interest, or fewer branches. None of those is an overdraft cost, but they belong in the calculation when overdraft policy is the reason you're considering a switch.

What it requires. Opening or converting to a qualifying account, then migrating the moving parts of your financial life — direct deposit, autopay, linked transfers, and any billers with your card on file. Some no-fee coverage features carry eligibility conditions; the institutions that cover small shortfalls require recurring direct deposits before the coverage limit activates, so the protection isn't available the day you open the account.

What's worth knowing. Choosing a no-fee bank removes the fee, not the shortfall. If your balance goes negative, a no-fee bank simply doesn't charge you the $35; but the underlying event still has consequences. A declined transaction can mean a missed rent payment, a returned-item fee from the biller, or a late fee on the bill that didn't clear. A covered transaction leaves you with a negative balance you still have to bring positive. Eliminating the bank's fee is a real and permanent saving, but it addresses the price of the shortfall, not the shortfall itself — which is why this strategy pairs with the predictive approach below rather than replacing it.

The split between predictive and reactive isn't a marketing distinction or a matter of degree. It's a structural one — the two categories differ in what they actually do at the mechanical level, when they operate, and what they require from you.

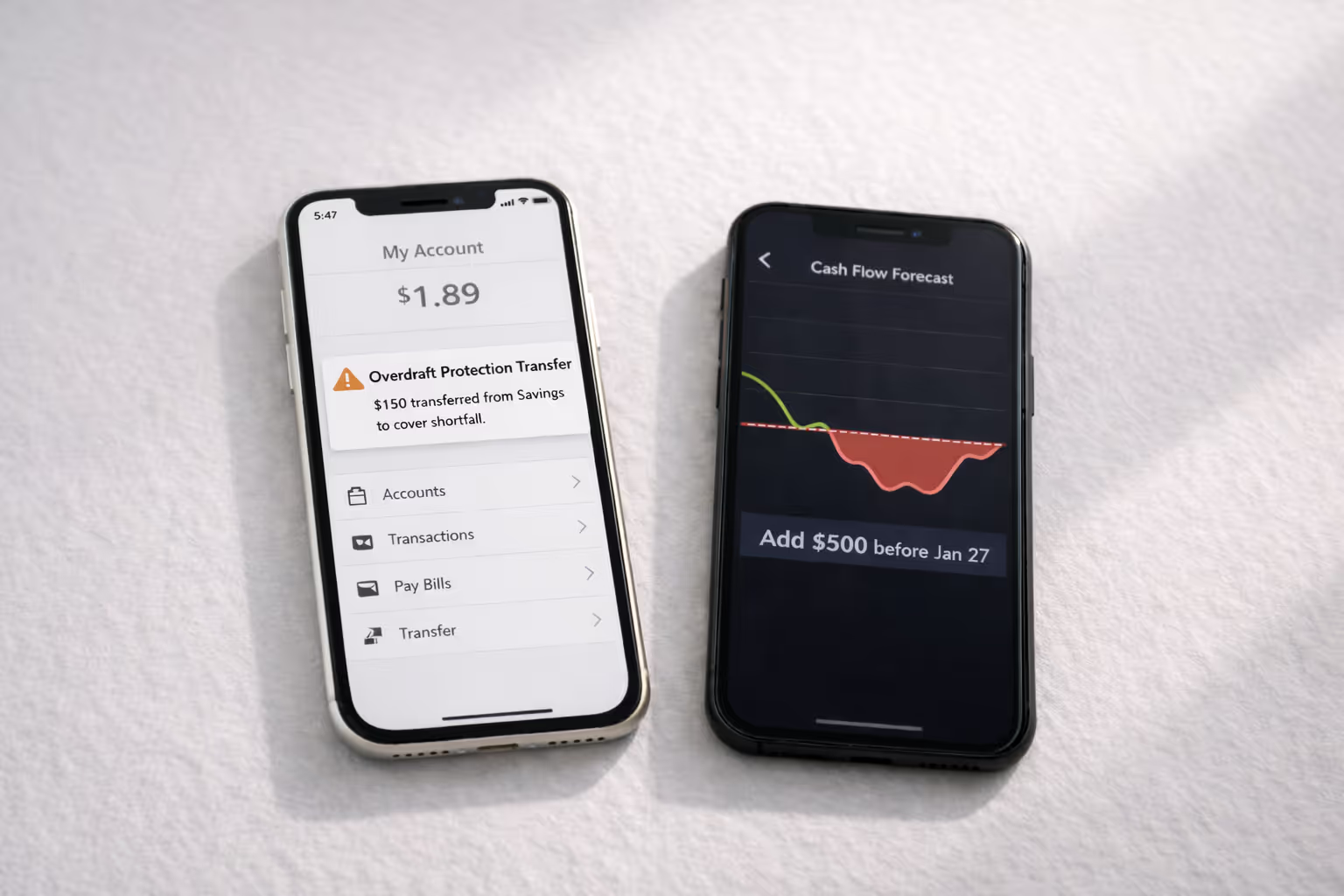

Predictive strategies operate before the shortfall exists. They work by giving you forward visibility into your checking account: projecting your balance day by day over the coming weeks based on expected income and expenses, so you can see a potential overdraft on your timeline before it reaches your bank statement. With that visibility comes lead time — days or weeks during which you can transfer funds from savings proactively, pick up an extra shift, adjust a discretionary purchase, or contact a biller about shifting a due date. The mechanical event of overdrafting never occurs because the underlying situation that would have caused it gets resolved while it's still resolvable.

Reactive strategies operate at or near the moment your balance goes negative. They work by intervening on the transaction or the fee itself. Some cover the shortfall after it occurs by pulling funds from a linked account or extending credit. Some intervene just before the balance crosses zero by lending you money to keep it positive. Some decline the transaction so it doesn't process at all. In each case, the strategy activates in response to an overdraft that's imminent or already occurring — not in anticipation of one.

The mechanical distinction has practical consequences. Predictive strategies require forward visibility into your cash flow, which means they need information about your upcoming income and expenses. Reactive strategies require either a moment-of-crisis response mechanism — a linked account, a credit line, an app that can fund your checking in minutes — or a backup source of funds you've established in advance. These are different requirements, and they suit different situations.

The cost structures also differ. Predictive strategies are typically priced as flat subscriptions whose cost doesn't change based on how often you would have overdrafted. Most reactive strategies have costs that scale with overdraft frequency, either directly (paying per overdraft fee, per cash advance, per transfer) or indirectly (a base subscription plus per-event fees). The table that follows shows what this looks like in practice.

What it is. Checking account cash flow forecasting projects your checking account balance forward over a defined horizon — typically the next 1-2 months. You start with your current balance and add or subtract your expected cash flow events on the dates each is scheduled to occur. The result is a day-by-day trajectory of where your balance is heading, including any points at which it's projected to drop below $0.

What it costs. Forecasting tools designed for checking accounts are priced as flat subscriptions. Centinel costs $59.99/year on the annual plan or $6.99/month billed monthly. Quicken Simplifi bundles forecasting within a broader budgeting suite at a higher price point that varies by promotion. Manual forecasting in a spreadsheet costs nothing but requires real effort — typically 2-4 hours of upfront setup, plus roughly 30 minutes per week of ongoing maintenance to log new transactions and adjust for variance.

The defining feature of forecasting costs is that they don't scale with overdraft frequency. The annual cost is the same whether you would have otherwise overdrafted ten times or zero. A user who builds a stable cash flow over a year of forecasting doesn't pay less than a user still working through frequent shortfalls. The cost is for the visibility, not for any specific overdraft event.

What it requires. Automated forecasting tools like Centinel connect to your bank via Plaid and update the forecast daily as new transactions post. Manual forecasting requires you to maintain the inputs yourself in a spreadsheet.

Beyond setup, forecasting requires ongoing engagement: roughly 5-10 minutes per week with an automated tool to confirm transaction categorizations, add upcoming events, and review the forecast. A forecast that's not maintained becomes inaccurate; an accurate forecast that's not consulted is just data.

What’s worth knowing. Forecasting is the only strategy in this guide that operates by changing what you can see rather than by intervening at the moment of crisis. That distinction has two practical consequences worth understanding.

The first is that forecasting gives you more options than any reactive strategy. When a projected shortfall appears two weeks out, the response isn't limited to "transfer money from savings" — though that's one option. Forecasting adds the others: moving a bill payment date, contacting a biller about rescheduling, adjusting a discretionary purchase, or picking up extra hours. Reactive strategies offer one response: their own. Forecasting offers a menu, plus the time to choose among them.

The second is that forecasting tends to reveal things about your cash flow beyond the specific overdraft risk you started watching for. Recurring expenses you forgot you had. Bills landing on dates you could shift if you wanted to. Income timing that consistently creates tight weeks. Seeing these patterns repeatedly tends to change what you do about them — restructuring around the tight weeks, canceling the forgotten expenses, anticipating the timing collisions before they create overdraft risk. The forecast becomes a tool for understanding and managing your finances broadly, not just for preventing the event that originally motivated building one. The shift is from reacting to your checking account to managing it.

This is also where the real cost of forecasting sits — not in the subscription but in the engagement. Forecasting requires that you look at your cash flow regularly and respond to what you see. That's a real ask, and some readers will reasonably decide it isn't worth the trade. The compounding benefit only shows up if you stay engaged long enough for the patterns to emerge.

The three strategies below all activate at or near the moment of overdraft — covering the shortfall once it occurs, intervening just before it does, or declining the transaction so it doesn't process. They differ in mechanism, cost, and what they require, but they share a common feature: they wait for a problem to materialize before responding to it. Balance monitoring and low-balance alerts are the baseline behaviors that precede these interventions — both are free and useful as a first step, but they tell you what your balance is now rather than where it's heading, which makes them limited as standalone strategies.

What it is. Bank overdraft protection is a service that links a secondary account — usually a savings or money market account, sometimes a line of credit — to your checking account. When a transaction would take your checking balance below zero, the bank automatically transfers funds from the linked account to cover the shortfall.

What it costs. At most major banks, the transfer is now free. Chase, Wells Fargo, Capital One, and Citibank have eliminated overdraft protection transfer fees entirely. Some smaller banks and credit unions still charge $10-$12 per transfer. Lines of credit used as overdraft protection accrue interest at the credit account's rate — typically 18-21% on standalone overdraft credit lines, higher for credit-card-linked protection.

What it requires. A linked account at the same bank with sufficient funds available at the moment of overdraft. If your savings account is empty when the transfer is triggered, overdraft protection fails and you incur the standard overdraft fee anyway. For lines of credit, you need credit approval and an established account before the protection can activate.

What’s worth knowing. Overdraft protection covers the shortfall but doesn't prevent the underlying event — your checking balance still goes negative, and the protection just bails it out. The transfer happens on the bank's terms: the algorithm decides when to move money and how much, based on a transaction that's already attempted. You see the result on your statement. The other thing worth understanding is that "free" transfers aren't actually free — each one drains your linked savings. A customer who relies on overdraft protection four times a year quietly moves several hundred dollars out of savings; over years, that's a real cost that doesn't show up as a fee. Overdraft protection works well as a backup for genuinely unexpected events, but using it as your primary strategy means quietly funding your overdrafts from your own savings every time.

What it is. Under federal Regulation E rules in effect since 2010, banks cannot charge overdraft fees on debit card purchases or ATM withdrawals unless you've affirmatively opted in to their overdraft coverage program. If you've never opted in, debit and ATM transactions that would overdraft your account simply get declined — no fee, no further action. If you have opted in at some point (often during account opening or a later prompt), you can opt out at any time to return to the default protected state.

What it costs. Nothing directly. Declined transactions don't incur fees. The indirect cost is inconvenience: your card gets rejected at the register or the ATM doesn't dispense cash.

What it requires. Check your current opt-in status by reviewing your account's overdraft service settings (typically in online banking under "Services" or "Overdraft Options") or by calling your bank. If you're currently opted in and want to change that, the opt-out request takes effect within a business day.

What’s worth knowing. This strategy eliminates one category of overdraft risk entirely — but only one. The protection applies exclusively to debit card transactions and ATM withdrawals. It does not apply to checks, ACH payments, or recurring electronic transfers, which include rent, mortgage, car payments, insurance, utilities, and most other recurring bills. These are typically the largest transactions hitting your checking account, and they're the ones where this strategy provides no protection at all. Your bank can still pay or return them at its discretion and charge you accordingly. Declining debit card overdrafts is a worthwhile baseline, but it doesn't address the transactions that most commonly cause serious overdraft problems.

What it is. Cash advance apps are services that lend you money before payday in exchange for a fee, subscription, tip, or some combination. The mechanic is straightforward: when your checking balance is at risk of going negative, the app deposits funds into your account to keep it positive, then deducts the advance from your next paycheck.

What it costs. Pricing varies significantly across the category. Subscription-model apps charge a monthly fee — typically $8-$15 — which works out to $96-$180 annually before any per-advance fees. Per-advance models charge a flat service fee per advance (often 5% of the advance amount with a $5 floor and $15 cap) plus an instant-transfer fee if you need the money same-day. Tip-based models charge no subscription but solicit optional tips that average $3-9 per advance, plus instant-transfer fees of $4-6. At 4 advances per year, total costs range from roughly $70 to $140 across the category. At 10 advances per year, costs range from $130 to $280.

What it requires. Most cash advance apps require a connected checking account, verified recurring income (typically 2-3 qualifying direct deposits), and a subscription or fee agreement. Some apps require their own checking account; others connect to your existing bank via Plaid. Some require W-2 employment with verifiable hours, which excludes gig workers, freelancers, and contractors.

What’s worth knowing. Cash advance apps prevent the overdraft event by funding your account before the balance crosses zero. Although the overdraft fee is averted, the cost is paid through a different mechanism: subscription fees, per-advance charges, instant-transfer fees, or tips. The CFPB's 2024 Data Spotlight on the paycheck advance market documented that the typical employer-partnered earned wage advance carries an APR over 100%, with users averaging 27 transactions per year. User surveys cited in that report described "getting caught in a liquidity cycle" as a recurring concern. The structural feature of advance-based products that makes them difficult to exit without a separate change in behavior or cash flow: each advance covers one shortfall, but the next paycheck is reduced by the advance amount, creating the conditions for the next advance — a self-reinforcing cycle.

For most readers, the most effective approach is layered — using the strategies in combination rather than picking one. The components, in order of priority:

One threshold question comes first: if your bank still charges overdraft fees, consider whether a no-fee bank fits the rest of your needs. Switching eliminates the fee permanently — but only the fee, not the shortfall behind it. A no-fee bank that declines your rent payment has saved you $35 and left you with unpaid rent. That's why bank choice sits alongside the layered approach rather than replacing it: it zeroes out the price of a shortfall, while the strategies below address the shortfall itself.

Use forecasting. A 1-2 month forward view of your checking account is what gives you lead time on potential shortfalls. The best apps for overdraft prediction use this forward-looking view to surface shortfalls weeks before they reach your bank statement. Think of forecasting as headlights — it shows you what's coming so you can avoid the collision entirely.

Set up overdraft protection as a backup. If you have a savings account at the same bank as your checking, link them for overdraft protection. At most major banks this is free. Think of it as a seatbelt — it limits the damage if a collision happens despite your headlights. The point isn't to rely on it as your primary defense; it's to have a safety net for the genuinely unexpected event your forecast didn't anticipate.

Verify your debit overdraft opt-in status. If you've affirmatively opted in to debit card overdraft coverage at some point, opt out. There's no reason to be charged $35 for a $7 coffee.

Avoid building your strategy around cash advance apps. They mechanically prevent the overdraft event, but the cost structure tends to keep users in repeating cycles of advances. If you're already using one, the question is whether building a forecast would replace the need.

The reason for the layered structure: prevention and protection are different jobs, and you want both. Nobody recommends driving without a seatbelt because they drive carefully. Nobody recommends driving without headlights because they have a seatbelt. The two work together — they don't substitute for each other. When forecasting is working, your overdraft protection almost never activates. It stops being something you rely on and becomes what it should be — a backstop you barely think about.

Yes — and the most direct route is to use a bank that doesn't charge them. Some banks will either decline the transaction or cover small shortfalls at no cost. That removes the fee permanently, though it doesn't remove the shortfall behind it — a declined or covered transaction can still mean a missed payment. For anyone whose bank still charges, or for those who want to avoid the other downsides of a missed payment, a layered approach eliminates nearly all exposure: forecasting prevents the shortfall from happening by surfacing it weeks ahead, declining debit card overdraft coverage eliminates one category of fees outright, and bank overdraft protection covers the genuinely unexpected event. Used together, these close off virtually all overdraft fee exposure.

Overdraft protection is a bank service that activates after your balance goes negative — typically by pulling funds from a linked savings account or credit line to cover the shortfall. Overdraft prediction (through cash flow forecasting) identifies a potential shortfall in advance, giving you time to act before your balance crosses $0. Protection responds to a problem; prediction surfaces one so you can prevent it. Both can be used together, with prediction as the primary strategy and protection as a backup.

You can opt out of overdraft coverage for debit card purchases and ATM withdrawals — that's protected under federal Regulation E rules. Once you opt out, those transactions are declined when your available balance is insufficient, with no fee charged. The limitation is that opting out doesn't apply to checks, ACH transactions, or recurring electronic transfers. Your largest bills (rent, mortgage, car payments, utilities) typically fall outside opt-out protection, so it's a partial strategy rather than a complete one.

Mechanically, yes — cash advance apps deposit money into your account before your balance crosses $0, keeping the overdraft event from occurring. The advance is deducted from your next paycheck, which tends to reduce the next paycheck's coverage of upcoming bills, creating the conditions for the next advance. The CFPB's 2024 Data Spotlight on the paycheck advance market documented that the typical user takes 27 advances per year, with an effective APR over 100%. Cash advance apps prevent individual overdraft events but often replace overdraft fees with subscription fees, per-advance charges, and instant-transfer fees.

As a backup strategy, yes. As a primary strategy, no. Overdraft protection covers the shortfall after the balance goes negative, but it doesn't prevent the underlying timing collision. If you rely on overdraft protection as your only defense, you're systematically funding overdrafts from your linked savings account (or borrowing against a line of credit) every time the system activates. Used alongside forecasting, overdraft protection becomes what it's designed to be — a safety net for the genuinely unexpected event, rarely activated.

The direct savings depend on your overdraft frequency. A user who overdrafts 4 times per year at the $35 average fee charged by most large banks pays $140 in overdraft fees annually; eliminating those overdrafts saves $140. A user with 10 overdrafts per year saves $350. For users who overdraft more than 10 times annually, CFPB research has found the average annual cost is $380.

Yes, most large banks still charge overdraft fees, typically $35 per overdraft. Some banks have reduced fees (Bank of America charges $10) and others have eliminated them entirely (Capital One, Citibank, Ally Bank). The CFPB's December 2024 final rule that would have capped overdraft fees at $5 for very large banks was overturned by Congress in 2025, so the regulatory cap is no longer in effect. Banks remain free to set their own overdraft fee amounts, subject to disclosure requirements.

STAY A STEP AHEAD