From retirement planning to checking account cash flow, here are the major types of personal finance forecasting — what each one does and who it's for.

March 3, 2026

Personal finance has built an entire industry around long-term forecasting — retirement calculators, net worth trackers, investment projections. But almost no one is forecasting the thing that causes the most day-to-day financial stress: what's happening in their checking account over the next 30 to 60 days.

When most people hear "financial forecasting," they think of retirement. They picture compound interest charts stretching decades into the future, Monte Carlo simulations spitting out probabilities, and the perennial question: Am I saving enough?

That's one type of forecasting. It's important. But it's far from the only type, and it might not even be the most urgent one for your daily financial life.

Personal finance forecasting actually spans a wide range of methods, each designed to answer a different question across a different time horizon. Some look decades ahead. Others look weeks ahead. Some track your total wealth. Others track the exact balance in your checking account on a specific Tuesday. The major types include retirement forecasting, net worth projection, investment return forecasting, goal-based savings forecasting, tax forecasting, debt payoff forecasting, income forecasting, expense forecasting, and checking account cash-flow forecasting.

This guide maps the full landscape. For each type, we'll cover what it is, what question it answers, who it's for, the time horizon it covers, and the tools people use to do it. By the end, you'll have a clear picture of which types of forecasting you're already doing — and which ones you might be missing.

Before diving into the taxonomy, it's worth defining what forecasting actually means in a personal finance context — because it often gets conflated with related but distinct concepts.

Forecasting is the practice of using data and assumptions about the future to project financial outcomes forward in time. It answers variations of the question: Based on what I know today, what's likely to happen next? That "next" could be next week, next year, or thirty years from now. The key characteristic is that a forecast is forward-looking. It uses what you know to estimate what you don't yet know.

This makes forecasting different from tracking, which is backward-looking. Tracking records what has already happened — transactions that have posted, money that has been spent, gains that have been realized. It tells you where you've been, not where you're going. Forecasting is also different from budgeting, which is a plan for how you intend to allocate resources. A budget says "I plan to spend $500 on groceries this month." A forecast says "Based on your scheduled bills and income, your checking account will drop to $342 on the 18th before your next paycheck hits on the 20th." The budget is aspirational. The forecast is predictive. Both are useful, but they answer different questions.

With that foundation in place, here's the full taxonomy.

The table below summarizes the major types of personal finance forecasting. Each is covered in detail in the sections that follow.

The types of forecasting most people are already familiar with operate on long time horizons — years, decades, or even a full lifetime. These are the tools the financial planning industry has been building for generations, and for good reason. Long-term forecasting helps you answer the big structural questions about your financial life: whether you're building wealth, whether you'll be able to retire, whether you're on track toward your biggest goals.

Retirement forecasting is the most widely practiced form of personal finance forecasting, and for many people, it's the only type they've ever encountered. The question it answers is straightforward: Am I saving enough to retire when I want to, and will my money last?

The mechanics are more complex than they appear. A credible retirement forecast needs to account for current savings, ongoing contributions, expected investment returns (usually modeled across a range of scenarios), inflation, Social Security timing and benefit amounts, pension income, tax treatment of different account types, healthcare costs, and your planned spending level in retirement. The best retirement forecasting tools use Monte Carlo simulations — running hundreds or thousands of scenarios with randomized return sequences — to express the result as a probability rather than a single number. Instead of "you'll have $1.2 million at 65," they say "you have a 78% chance of not running out of money before age 90."

The tools in this space are mature and abundant. Empower (formerly Personal Capital) offers a free retirement planner that links to your investment accounts and runs Monte Carlo analysis. Boldin (formerly NewRetirement) provides detailed scenario modeling with tax impact analysis. ProjectionLab is popular in the FIRE community for its granular control and clean interface. Fidelity, Vanguard, and Schwab all offer their own retirement calculators. And, of course, there's the ever-present spreadsheet.

Retirement forecasting is essential. But it's worth recognizing its limitations as a practical, day-to-day tool. A retirement forecast can tell you that you're on track for a comfortable retirement while you're simultaneously three days away from an overdraft. The time horizon is too long and the granularity is too coarse to help with the near-term timing problems that cause most financial stress.

Net worth projection tracks your total assets minus your total liabilities over time and projects the trajectory forward. If retirement forecasting asks "will I be okay at 65?", net worth projection asks a broader question: Is my overall financial position improving, and at what rate?

Your net worth is a composite number. It includes the equity in your home, the balance in your investment and retirement accounts, your cash savings, and any other assets — minus your mortgage balance, student loans, credit card debt, car loans, and other liabilities. Projecting it forward means estimating how each of these components will change over time: your home equity grows as you pay down the mortgage and (hopefully) as the property appreciates. Your investments grow with contributions and market returns. Your debts shrink as you make payments.

Net worth projection is most valuable as a macro health metric — a zoomed-out view of whether you're heading in the right direction. It's particularly useful for people with complex financial pictures (multiple debt types, a mix of investment accounts, real estate) who want a single number that captures the whole story. Empower, Monarch Money, and various spreadsheet templates are the most common tools. The limitation is the same as with retirement forecasting: net worth tells you nothing about liquidity or timing. You can have a net worth of $500,000 and still not be able to cover rent this month if your wealth is locked up in a house and a 401(k).

Investment return forecasting projects how your portfolio will grow under various assumptions about returns, asset allocation, and contribution schedules. The question: What will my investments be worth in X years, and how do different strategies affect the outcome?

This is closely related to retirement forecasting, but the focus is narrower — it's about the investment engine itself rather than the full retirement picture. Someone might use investment return forecasting to compare the long-term impact of different asset allocations (80/20 stocks-to-bonds versus 60/40), to model the effect of increasing their 401(k) contribution by 2%, or to understand the range of outcomes they might face given historical market volatility.

The tools overlap heavily with retirement forecasting. Monte Carlo simulations and historical backtesting are the standard methods. Robo-advisors like Betterment and Wealthfront build basic versions of this into their platforms. For the more hands-on crowd, platforms like Portfolio Visualizer allow granular backtesting and projection of specific asset allocations. The key insight from investment return forecasting is that returns aren't deterministic — the sequence of returns matters enormously, especially near retirement (this is the "sequence-of-returns risk" that financial planners talk about). A good forecast accounts for this uncertainty rather than assuming a smooth average growth rate.

Goal-based savings forecasting is the most accessible form of long-term forecasting because the math is straightforward and the target is concrete. The question: When will I have enough saved for [specific goal], and how much do I need to set aside each month to get there?

The goals can be anything: a house down payment, a child's college education, an emergency fund, a wedding, a car, a vacation. The inputs are simple — your target amount, your current savings, your expected monthly contribution, and the interest or return rate on whatever account you're saving in. The output is equally simple: a date when you'll reach your goal, or the monthly amount required to reach it by a specific date.

Nearly every banking app with a "goals" feature is doing a version of this. Compound interest calculators perform the same function. What makes this type of forecasting valuable isn't its sophistication — it's its concreteness. People are more motivated to save when they can see a specific target getting closer.

Tax forecasting estimates future tax liability to inform decisions about withholding, Roth conversions, capital gains harvesting, and quarterly estimated payments. The question: What will I owe in taxes, and how can I minimize the total through timing and strategy?

This is more specialized than the other types and is most relevant for people with complex tax situations: higher earners, self-employed individuals making quarterly estimated payments, retirees strategizing about which accounts to draw from and when, and anyone considering Roth conversion ladders or capital gains harvesting. The time horizon is typically annual, but multi-year planning is common for strategies like systematic Roth conversions during lower-income years.

Tax forecasting is often done in partnership with a CPA or financial planner, though tools like Boldin and ProjectionLab include tax modeling features that allow individuals to run their own scenarios. The value is real — the difference between a naive approach to distributions and a tax-optimized one can be worth tens of thousands of dollars over a retirement.

Debt payoff forecasting models repayment timelines and total interest costs under different strategies. The question: When will I be debt-free, and what's the optimal path to get there?

If you're carrying student loans, credit card balances, an auto loan, and a mortgage, you have choices about how to allocate extra payments. The debt avalanche method prioritizes the highest-interest-rate balance first to minimize total interest paid. The debt snowball method prioritizes the smallest balance first to build psychological momentum. Refinancing, consolidation, and balance transfers introduce additional variables. Debt payoff forecasting lets you model these different scenarios and see the concrete impact — often measured in months shaved off the timeline and dollars saved in interest.

Tools like Undebt.it are purpose-built for this. Many budgeting apps (Monarch Money, YNAB) include debt tracking and projection features. Amortization calculators handle individual loans. The math is deterministic — unlike investment returns, loan terms and interest rates are fixed (or at least knowable), so the projections tend to be reliable.

Here's where the map gets sparse. The types of forecasting above are well-established, well-tooled, and widely practiced. The financial planning industry has spent decades building infrastructure for long-term forecasting — but almost nothing for the short-term. They all operate on time horizons of months, years, or decades.

Financial stress, though, is most often caused by near-term timing problems. Not "will I have enough at 65?" but "will I have enough on the 15th?" Not "am I spending too much in general?" but "can my checking account handle the rent, the car payment, and the credit card bill all posting in the same week?"

Short-term forecasting is the domain that answers these questions — and it's dramatically underserved.

Income forecasting is the practice of projecting future earnings when they aren't fixed or predictable. The question: What can I expect to earn in the coming weeks or months, and how do I plan around that uncertainty?

This is most relevant for freelancers, gig workers, commission-based salespeople, seasonal workers, and anyone else whose income fluctuates. If you receive a fixed salary on a predictable schedule, your income is already "forecasted" — you know what's coming and when. But a growing share of the workforce doesn't have that certainty. For variable earners, income forecasting might involve calculating a rolling average of the past three to six months of earnings, building a pipeline-based estimate from current contracts and proposals, or simply making conservative assumptions based on historical patterns.

Income forecasting is important because it's a prerequisite for effective cash-flow forecasting. If you don't know what's coming in, you can't project your balance forward with any confidence. Some accounting and invoicing tools offer basic income tracking and trend analysis, but purpose-built income forecasting tools for consumers are rare. Most variable earners end up doing this informally — which is better than not doing it at all, but leaves significant room for improvement.

Expense forecasting predicts future spending based on historical patterns, known upcoming bills, and anticipated one-time costs. The question: What will I spend next month, and are there any unusual expenses ahead that I need to prepare for?

This is relevant for everyone, but it's especially critical for people with irregular expenses — annual insurance premiums, semi-annual property taxes, quarterly estimated tax payments, back-to-school costs, holiday spending, or that car registration renewal that always seems to arrive unexpectedly. Expense forecasting involves looking forward at the calendar and identifying what's coming rather than looking backward at what's already been spent.

Many budgeting apps offer historical trend analysis that can help with this. If you've been tracking your spending in Monarch Money, YNAB, or a similar tool, you can see average spending by category over the past several months. But trend analysis alone isn't expense forecasting — it tells you what you typically spend, not what you're specifically going to spend next month. True expense forecasting requires layering in the known upcoming charges: the insurance premium due on the 12th, the property tax payment on the 15th, the holiday travel you've already booked. Pairing income forecasting with expense forecasting is what produces a cash-flow forecast — which brings us to the type of forecasting that most people are missing entirely.

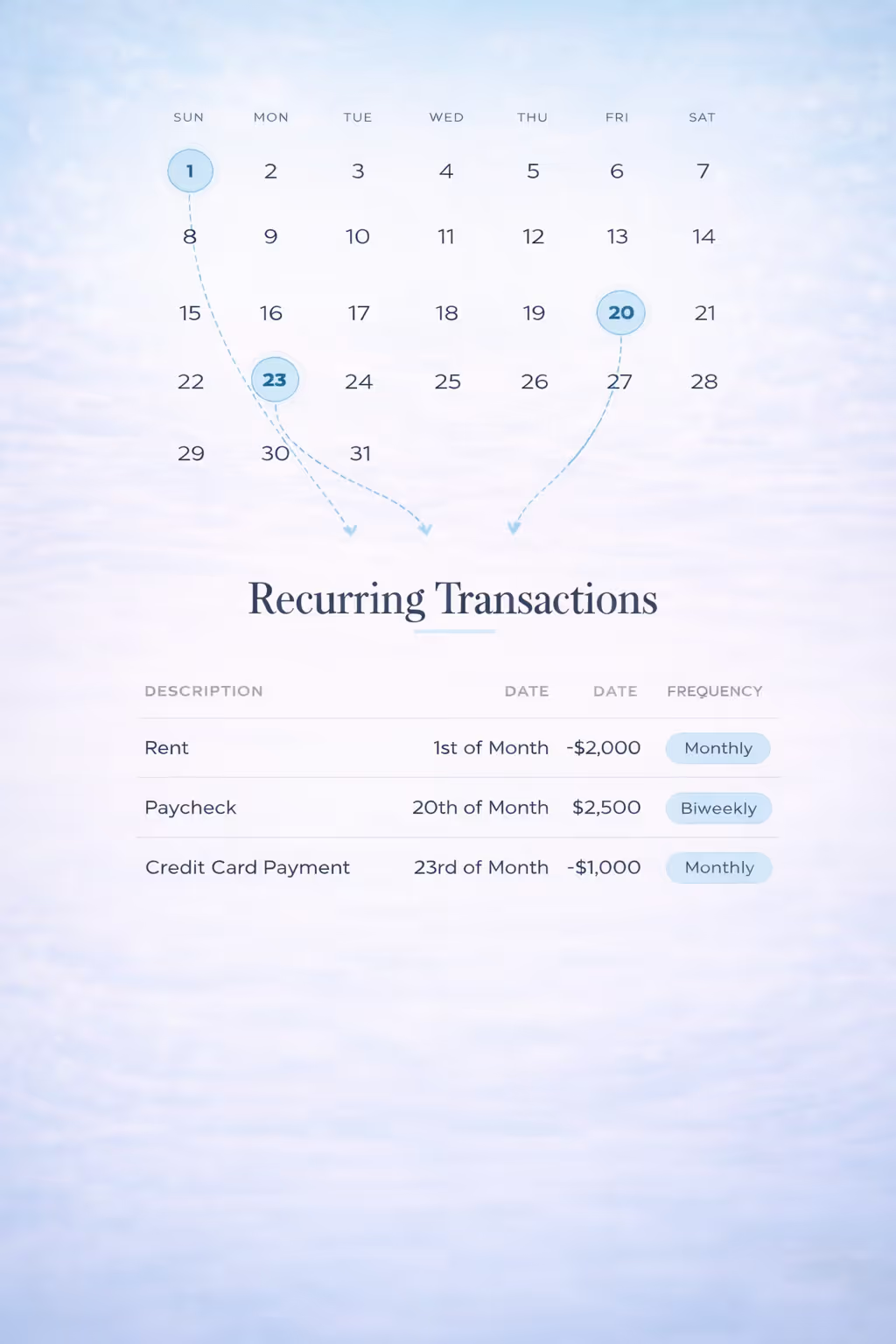

Checking account cash-flow forecasting is the most practical and arguably the most underserved form of personal finance forecasting. It answers the question that causes more day-to-day financial stress than any other: Will I have enough money in my checking account when my bills hit — and is there any surplus I can confidently put to use?

Here's how it works. You start with your current checking account balance. Then you walk forward day by day, adding projected income on the dates it's expected to arrive and subtracting projected expenses on the dates they're expected to post. The result is a running projection of your future checking account balance — a line that rises when paychecks land and falls when bills hit, showing exactly how your balance will move over the next 30 to 90 days.

This is fundamentally different from every other type of forecasting on this list. Retirement forecasting tells you about decades from now. Net worth projection tells you about your total wealth. Budgeting tells you about spending categories. None of them tell you about timing and liquidity — the specific sequence in which money arrives and departs your checking account and whether the balance stays positive throughout. A retirement forecast can say you're on track. A budget can say you're living within your means. And your checking account can still drop below zero next Thursday because your rent posted before your paycheck.

What a checking account cash-flow forecast reveals is a metric you can't get from any other type of forecast: your projected minimum balance — the lowest point your account will reach over the forecast period. This single number is powerful because it unlocks two critical insights. First, it tells you whether you're at risk of overdrafting (or dipping below whatever minimum balance you're comfortable with). Second, it tells you how much surplus cash you actually have available to spend or optimize your checking account — money you can confidently move to savings, investments, or debt payments without risking a shortfall.

This is beginning to change. Centinel, for example, is built specifically around this concept — it takes your current checking account balance, your scheduled income and expenses, and runs a daily 60-day forecast that surfaces your projected available cash and flags shortfall risks before they happen. But regardless of the tool, the underlying idea is the same: instead of glancing at your balance and hoping it's enough, you project forward to forecast whether it is enough. That day-by-day simulation involves specific design decisions — a deterministic rather than predictive approach, conservative assumptions about same-day transaction ordering, and a calibrated forecast window — that together determine how the mechanics of a checking account cash flow forecast translate into numbers you can reliably act on. It's the consumer version of what corporate treasury departments have been doing for decades.

This is the type of forecasting that sits at the core of everything else. Your retirement contribution doesn't matter if it triggers an overdraft. Your debt payoff strategy doesn't matter if following it leaves your checking account short. Checking account cash-flow forecasting is the operational layer that makes all your other financial plans executable.

The most important takeaway from this taxonomy isn't "there are nine types of forecasting and here's what they all do." It's that these aren't competing approaches — they're complementary layers. Most people need at least two or three types working together, and the ones they're missing are almost always on the short-term end.

Think of it as a forecasting stack. Retirement forecasting tells you whether you're saving enough for the long run. Investment return forecasting tells you whether your allocation is right. Debt payoff forecasting tells you the most efficient path to becoming debt-free. But none of these can tell you whether your checking account can absorb the action they recommend this month. That's the role of checking account cash-flow forecasting — it's the operational foundation that turns long-term financial plans into decisions you can actually execute without putting your near-term stability at risk.

If you're reading this and recognizing that you've built a solid long-term forecasting practice — you check your retirement projections, you track your net worth, you model your investment returns — but you still occasionally get surprised by your checking account balance, you're not alone. That gap between long-term visibility and short-term visibility is the norm for most people, and closing it is one of the highest-leverage things you can do for your day-to-day financial confidence.

Audit your own forecasting stack. Which of these nine types are you already doing, even informally? Which ones are you missing? For most people, the answer to that second question is checking account cash-flow forecasting — the one type that addresses the financial question they face most often: Can I afford this right now, and will my account be okay next week?

Centinel lets you build and manage a 60-day checking account forecast — either by entering your cash flow manually or by connecting your accounts to automate the process — and shows you both your risk points and your available surplus.

STAY A STEP AHEAD