Banks process transactions in batches, and the order matters. Here's how posting order can trigger overdraft fees — and how to protect against it.

January 31, 2026

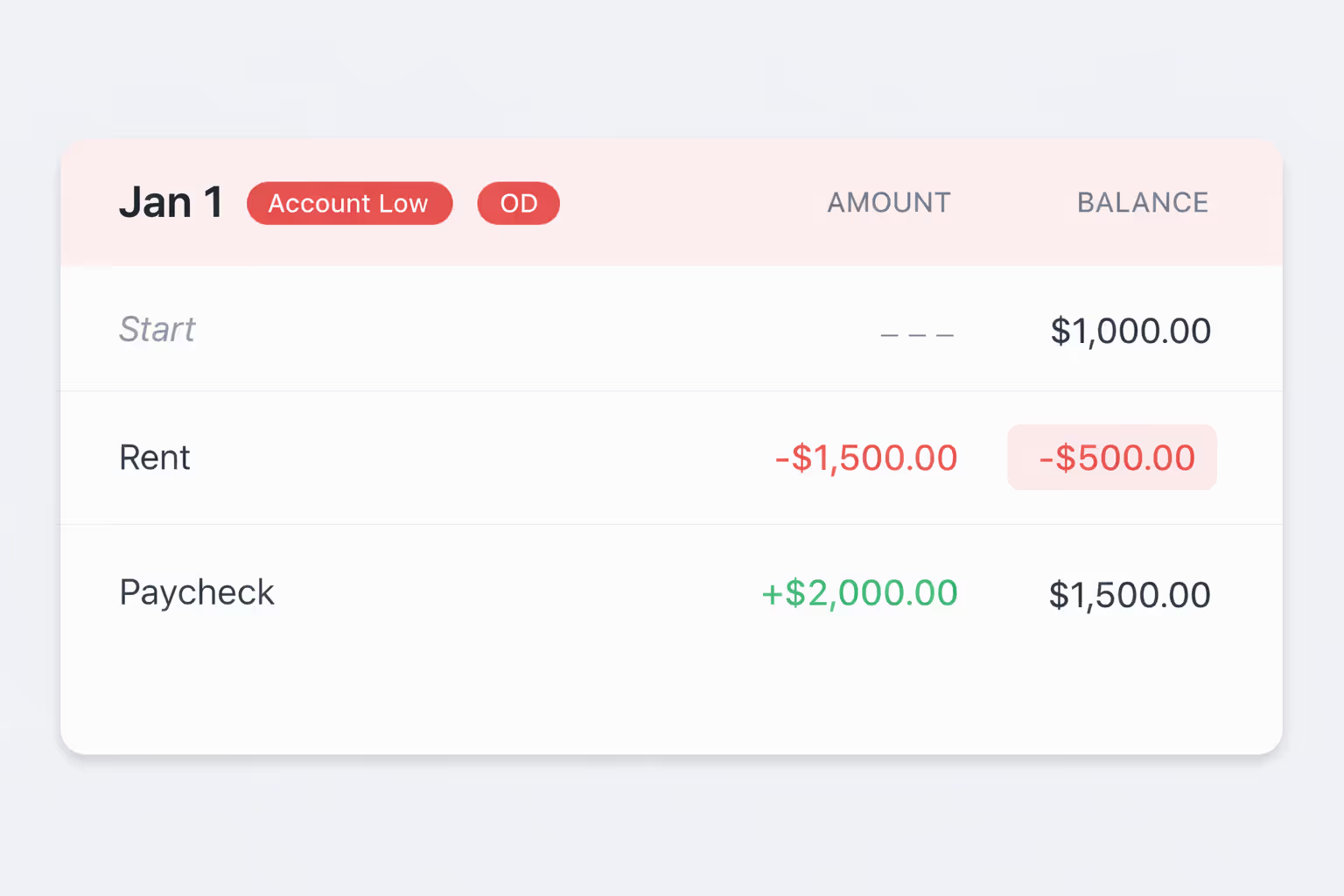

You know your checking account balance: $1,000. You know your paycheck of $2,000 hits tomorrow. You know your rent of $1,500 is scheduled to come out tomorrow. You've done the math—$1,000 + $2,000 - $1,500 = $1,500. Plenty of cushion. You go to bed confident. You wake up to an overdraft fee.

What happened?

This is the posting order problem—a consequence of how banks process transactions that can cost you money even when you've planned carefully. The order in which transactions post to your account isn't always predictable, and when timing doesn't go your way, you can overdraft even when the math should work out.

This isn't carelessness. This isn't poor planning. This is a structural feature of how banking works, and most people don't know about it until it costs them. In this article, we'll explain what posting order is, the two ways it can cost you money, and what you can do to protect yourself from an uncertain system.

When you swipe your card, write a check, or have an automatic payment go through, the transaction doesn't immediately and permanently affect your account balance. There's a gap between when a transaction happens and when it officially counts.

Every transaction moves through two distinct stages. The first is authorization, when the bank approves the transaction. For debit card purchases, this happens in real-time at the point of sale—the merchant's terminal communicates with your bank, confirms you have sufficient funds, and the bank gives the green light. The second stage is posting, when the transaction is finalized and permanently applied to your balance.

The key insight is that most transactions aren't posted in real-time. Instead, they're processed in batches at the end of each business day. Think of your bank as sorting mail: transactions arrive throughout the day, but the bank opens, sorts, and processes them all at once after business hours. This batch processing is when your balance officially changes and when overdrafts are determined.

Banks have policies governing the sequence in which they apply transactions during that nightly processing. The general structure at many banks works like this: credits such as deposits post first, then debits such as withdrawals and payments, then fees. Within each category, banks may sequence transactions by chronological order, by check number, or by dollar amount from lowest to highest or vice versa.

These policies vary significantly by institution and are often buried in lengthy account agreements that most consumers never read. The critical point is that the order in which transactions post can affect whether you overdraft and how many overdraft fees you incur. Two people with identical transactions and identical starting balances can end up with different outcomes depending on their bank's posting order policy.

Your banking app shows you two numbers that sound similar but mean different things. Your current balance is the balance after all posted transactions—it doesn't reflect pending activity. Your available balance is your current balance adjusted for pending transactions, representing what you can theoretically spend right now.

The catch is that even your available balance may not tell the whole story. Pending deposits might be held and not yet accessible. Pending debits might not appear yet if the merchant hasn't submitted them. A balance check in the afternoon doesn't guarantee that same balance after tonight's batch processing applies all the day's transactions. This is why you can check your balance, see sufficient funds, and still overdraft hours later.

Now that you understand how posting order works, let's look at two specific ways it can cost you money. The first is debit reordering, where banks sequence your debits in ways that maximize overdraft fees. The second is same-day timing uncertainty, where you can't predict whether a deposit or a payment will post first when both are scheduled for the same day. These are related but distinct problems with different causes, different histories, and different implications for how you manage your money.

Some banks have processed debits from largest to smallest, regardless of when the transactions actually occurred. This practice, known as high-to-low posting, can dramatically multiply your overdraft fees.

Consider this example: you have $100 in your account and make four purchases throughout the day for $10, $20, $25, and $80. If your bank processes these transactions in chronological order or from lowest to highest, the $10, $20, and $25 clear successfully, leaving you with $45. Only the $80 purchase overdrafts, resulting in one overdraft fee. But if your bank uses high-to-low posting, the $80 posts first and leaves you with $20. Then the $25 overdrafts. Then the $20 overdrafts. Then the $10 overdrafts. Same transactions, same starting balance, same ending balance—but three overdraft fees instead of one.

Banks justified this practice by arguing it ensures important transactions like rent and mortgage payments clear first. Consumer advocates responded that this systematically maximized fee revenue at the expense of the most financially vulnerable customers—those with low balances who could least afford multiple fees.

The legal reckoning was significant. Class action lawsuits resulted in over $370 million in settlements against banks including Wells Fargo, Bank of America, U.S. Bank, and others. The Consumer Financial Protection Bureau issued guidance identifying unanticipated overdraft fees as potentially unfair practices.

Where do things stand today? Many banks have moved away from high-to-low posting for debit card transactions following litigation and regulatory pressure. However, practices still vary by institution and transaction type. High-to-low posting may still apply to checks at some banks. The takeaway is that you should check your bank's deposit agreement to understand their specific posting order policy—don't assume your bank follows consumer-friendly practices just because others have changed.

Let's return to the scenario from the introduction. Your paycheck of $2,000 and your rent payment of $1,500 are both scheduled for the same day. You start with $1,000. If the paycheck posts first, you're fine—your balance rises to $3,000 and then drops to $1,500 after rent. If rent posts first, you temporarily overdraft by $500 before the paycheck brings you back positive. Depending on your bank's policies, that momentary dip could trigger an overdraft fee.

The good news is that many banks have policies to post credits before debits during their end-of-day batch processing. In a straightforward scenario, your paycheck should post before your rent. But banking is a complex system with multiple moving parts, and "credits post first" doesn't eliminate all timing risk. Here's where uncertainty still lives.

Not all banks follow the same rules. Posting order policies vary by institution. While major banks have largely moved toward credits-first processing, not all banks and credit unions follow the same practices. Your specific bank may do things differently, and you may not know unless you've read your deposit agreement carefully.

Transactions types follow different paths. The credits-first rule typically applies within a batch of similar transactions, but different transaction types may be processed in different batches at different times. Your employer submits payroll as an ACH credit. Your landlord processes rent as an ACH debit. If these files arrive at your bank at different times—say, the rent debit file arrives in the morning batch and the payroll credit arrives in the afternoon batch—the debit might post first even at a credits-first bank.

Cutoff times create edge cases. Banks have daily cutoff times for processing transactions. If your employer's payroll provider submits the file late and misses your bank's cutoff, your paycheck might not post until the following day, while your rent posts on time. You thought both would hit the same day. They didn't. And you overdrafted.

Rules may differ by transaction type. The CFPB has noted this complexity: different rules may apply to debit card transactions versus ACH versus checks versus wire transfers. A bank might post ACH credits before ACH debits but handle debit card transactions on a different schedule entirely.

The bottom line is this: even if the system usually works in your favor, you can't know it will for your specific transactions on any given day. You're relying on your employer's payroll timing, your landlord's payment processing, your bank's batch schedules, and the interaction of multiple transaction types—none of which you fully control. This isn't necessarily about banks acting maliciously, though some have. It's about genuine complexity in a system that wasn't designed with consumer visibility in mind. The result is uncertainty, and uncertainty is what costs you money when timing doesn't go your way.

Now that you understand the problem—both the historical debit reordering issue and the ongoing timing uncertainty—let's talk about what you can do. There's no way to fully control how your bank processes transactions. But there are strategies to reduce your exposure and tools that can give you certainty even when the system doesn't.

The first step is knowing how your specific bank operates. Read your deposit account agreement, or at least search it for "posting order" or "transaction processing." Know which transaction types your bank processes first and how they sequence debits within categories.

If your bank still uses high-to-low posting for any transaction types, consider whether that's acceptable to you—or whether it's time to shop for a new bank. You can also call your bank directly and ask how they handle same-day debits and credits.

The traditional advice is to keep a cushion in your checking account to absorb timing variations. This works, but it has limitations. Maintaining a buffer requires extra money that many consumers don't have sitting idle. And without knowing how much cushion you actually need, you're guessing.

If possible, avoid scheduling large outflows on the same day as expected inflows. Pay bills a day or two after payday rather than on payday itself. This isn't always possible—automatic payments and employer-controlled deposit timing may not give you flexibility—but reducing same-day collisions where you can reduces timing risk.

The most robust way to avoid overdraft fees caused by posting-order uncertainty is to stop reacting to your balance after the fact and start projecting it forward. A checking account cash flow forecast simulates your account balance day by day based on your scheduled income and expenses, showing you where you are headed rather than just where you are.

The key feature to look for in a forecasting tool is conservative timing assumptions. The most useful tools don't assume everything will post in the best possible order. They assume debits post before credits on any given day, showing you the worst-case scenario.

Why does this matter? If your projected balance stays positive using pessimistic assumptions, you know you'll stay positive regardless of how transactions actually post, which is why conservative same-day timing is a key criterion for evaluating the best apps that predict overdrafts.

Most banks offer alerts when your balance drops below a threshold you set. These are useful as a backup but limited in scope. Alerts are reactive—you find out after your balance has dropped, which may be too late to prevent an overdraft that's already in processing. Better than nothing, especially for catching unexpected transactions, but not a substitute for forward-looking visibility.

The posting order problem is real, even if it doesn't affect every transaction you make. You don't have to accept this as an unavoidable cost of banking. Start by understanding your bank's specific policies so you're not operating blind. Maintain an appropriate buffer, ideally informed by a forecast of what you actually need rather than a guess. And consider using tools with conservative assumptions that show you the worst-case outcome, so you're never surprised by the best case not happening. With the right visibility and the right assumptions, you can anticipate problems before they happen and make confident decisions about your money.

STAY A STEP AHEAD