Biweekly pay doesn't make budgeting harder—it creates a liquidity management problem that budgeting can't solve. Understand what you're actually facing.

November 21, 2025

When I switched from semi-monthly to biweekly pay, something got noticeably harder. I'd look at my checking account balance and feel uncertain in a way I never had before. Was there enough to cover next week's bills? Could I move some to savings? The answer seemed to shift every time I checked.

I was already using a budgeting app. I was already organized – I tracked every dollar; I set up categories. I knew exactly where my money was going each month. And yet the feeling of being one step behind never went away. I was constantly recalculating which bills my next paycheck needed to cover, always running mental math about whether my balance would hold until the next paycheck. I felt like I was working twice as hard at my finances and getting worse results. Did I just need to budget better?

Here's what I eventually realized: I wasn't failing at budgeting. The problem wasn't that I needed to budget better. The problem was that I was using budgeting to solve something budgeting wasn't designed to solve. What made biweekly pay feel harder wasn't about resource allocation or spending discipline. It was about something else entirely—something that had been invisible when I was paid semi-monthly but became impossible to ignore when I switched to biweekly. And once I understood what that something was, everything changed.

When people struggle with biweekly pay, the advice follows a predictable script. Budget more carefully. Track every expense. Try zero-based budgeting. Use the envelope method. Download this app, set up that spreadsheet, be more disciplined.

And then there's the signature piece of biweekly budgeting wisdom that everyone seems to share: budget based on two paychecks per month instead of the actual twenty-six you receive per year. That way, twice a year when you get a third paycheck in a month, you can treat it as "bonus money" and put it toward savings, debt paydown, or larger expenses. It's presented as the clever solution that makes biweekly pay work in your favor instead of against you.

The message underneath all of this is clear: you're struggling because you're not managing your money well enough. You need better organization, more willpower, tighter control.

This advice comes from a good place. Budgeting is genuinely important. It's the foundation of sound personal finance. When someone is struggling financially, helping them create a better budget is often exactly the right move. So when someone says they're having trouble managing their money on biweekly pay, it makes perfect sense to assume the answer is better budgeting.

But here's what's interesting. When you talk to people who struggle with biweekly pay, many of them are already doing all the things they're supposed to do. They're not financially reckless. They know what their bills are and when they're due. They're tracking their spending. They're not blowing money on luxuries they can't afford. They're organized, disciplined, and intentional about their finances. And yet they still feel like they're constantly scrambling.

The standard advice helps a little. Better tracking gives them slightly more information. Better categories help them see their spending patterns more clearly. But the core struggle doesn't go away. They're still recalculating constantly. They're still uncertain about whether their current balance is truly enough. They're still working much harder at their finances than they feel they should have to.

If you recognize yourself in this description, I want you to know something important. The struggle you're experiencing isn't evidence that you're bad at budgeting. It's evidence that budgeting—no matter how well executed—can't solve the problem you're actually facing. To understand why, we need to be really clear about what budgeting is and isn't designed to do.

Budgeting, at its core, is about resource allocation. It's a tool that helps you answer a specific question: given that you have a certain amount of money, how should you divide that money across your various needs and priorities? Should you spend $500 on groceries or $600? How much should go to entertainment versus savings? Should you prioritize building your emergency fund or paying down debt faster?

These are important questions. Budgeting helps you make intentional choices instead of spending reactively and wondering where your money went. A good budget ensures your spending aligns with your values. It helps you identify areas where you might be overspending or under-saving. It creates accountability and awareness. When someone is struggling because they're spending more than they earn, or because they don't know where their money is going, budgeting is absolutely the right tool to deploy.

The beauty of budgeting as a tool is that it works regardless of how you're paid. Whether you receive your monthly income in one lump sum payment, two semi-monthly paychecks, or multiple biweekly installments, you can still create a budget that allocates your total income across your expense categories. A budget that says "$500 to groceries, $200 to entertainment, $1,500 to rent, $300 to savings" functions exactly the same way whether you earn $4,000 once per month or in smaller, more frequent chunks. The total income is the same. The expense categories are the same. The allocation decisions you need to make are the same.

But budgeting treats money as an abstraction. When you create a monthly budget, you're implicitly treating your monthly income as if it all arrives at the beginning of the month and you're simply deciding how to divide it up across your spending categories. The budget doesn't concern itself with the actual timing of when specific dollars flow into and out of your checking account. It deals with monthly totals, not daily cash positions.

This abstraction works perfectly well for what budgeting is designed to do—helping you make intentional choices about where your money goes and ensuring your spending aligns with your priorities. But it completely fails to address a different question that often matters just as much: will I have enough cash in my checking account at the specific moment each bill comes due?

That question isn't about allocation. It's about timing. And that's a completely different problem.

When you're struggling with biweekly pay, the question keeping you up at night isn't "am I allocating my income wisely across my priorities?" It's "will my checking account have enough money in it on the 12th when my credit card payment is due, given that I don't get paid until the 14th?"

You're not struggling with how to divide your resources. You're struggling with whether you'll have sufficient cash available at specific points in time to cover specific obligations as they come due.

This is liquidity management. And it's fundamentally different from budgeting.

Liquidity management is about ensuring that cash is available in your checking account when bills hit, accounting for the actual timing of when money flows in and out. It's not about whether you can afford your expenses in aggregate over the course of a month. It's about whether you can cover them in the specific sequence they occur, given the specific rhythm of when your income arrives.

Think about the difference. A budget might tell you that your monthly income is $5,000 and your monthly expenses are $4,800. You're in the positive. You can afford your life. But that budget doesn't tell you whether you'll have enough cash on hand to cover your $2,000 credit card payment on the 12th of the month if you've only received one of your two biweekly paychecks by that point and several other bills have already come out.

The budget says you can afford that payment. Liquidity management asks whether you'll have the cash when the payment is actually due. These are different questions requiring different kinds of analysis.

Here's what's crucial to understand: everyone who has a checking account and regular bills manages liquidity, whether they realize it or not. If you're paid monthly or semi-monthly, you're managing liquidity. The difference is that for some pay schedules, liquidity management is so straightforward that it becomes invisible. You're doing it, but you're not consciously aware you're doing it as a separate activity from your regular financial management.

The reason liquidity management feels easy—almost effortless—when you're paid monthly or semi-monthly has nothing to do with budgeting methodology or financial discipline. It's purely a function of calendar alignment.

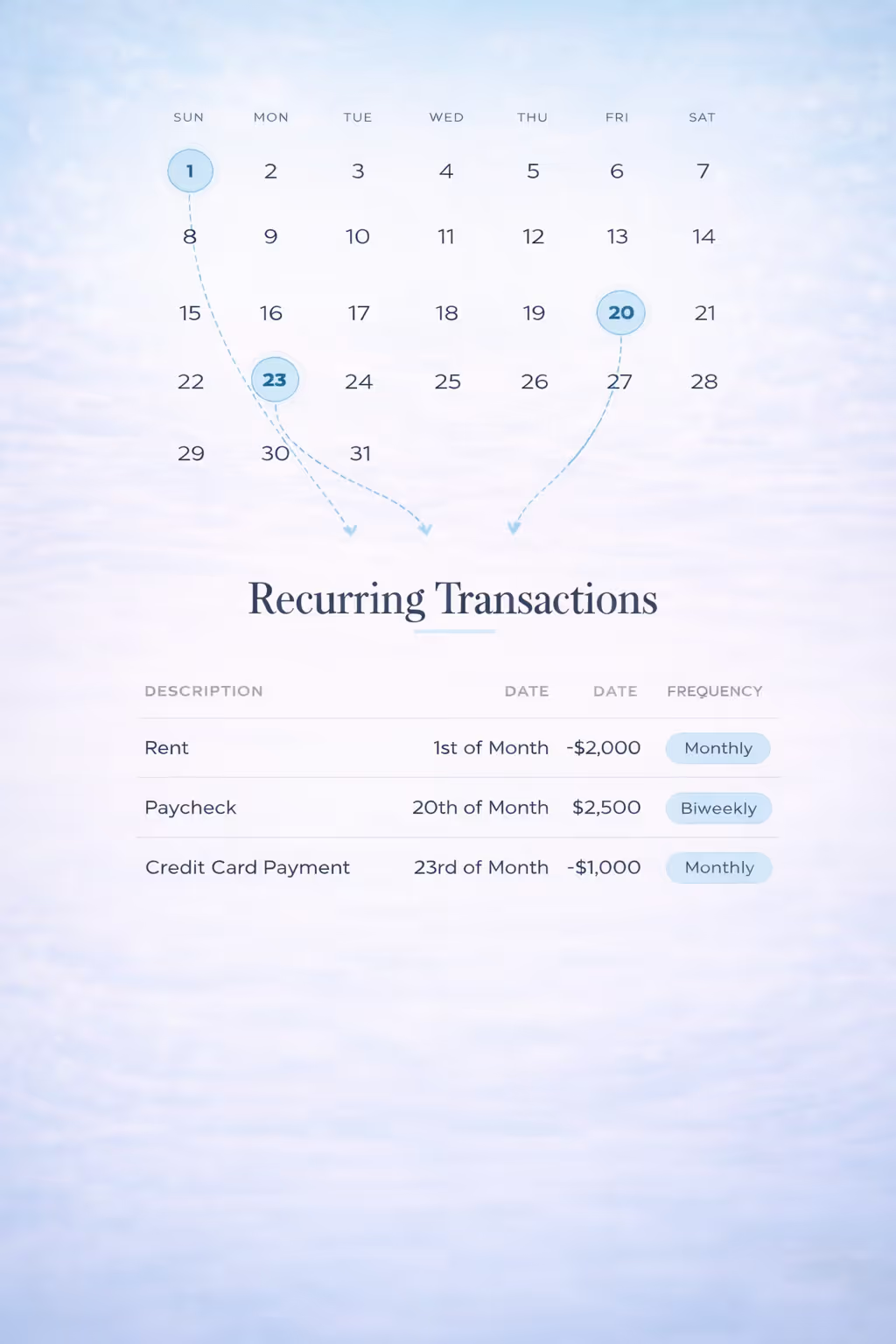

When you're paid on a monthly or semi-monthly schedule, your income and your bills are both anchored to the same calendar system. Your rent is due on the 1st of the month. Your car payment is due on the 4th of the month. Your credit card payment is due on the 19th of the month. Your paychecks arrive on the 1st and the 15th of the month. Notice how both income and expenses are described using the same language—days of the month? That's because they're both synchronized to the calendar. This alignment between when money arrives and when obligations are due creates stable, predictable mappings that solve the liquidity problem automatically.

You learn through simple observation that your 1st-of-the-month paycheck always covers rent and your car payment. Your mid-month paycheck always covers your credit card payment. This mapping is stable—it's the same every single month. The same paycheck is always responsible for the same bills. You figure this out once, and then you can rely on it forever without thinking about it.

This has nothing to do with how well you budget. Someone who does no budgeting at all but happens to be paid semi-monthly still benefits from this stable mapping. The first-of-month paycheck still reliably arrives when first-of-month bills are due, regardless of whether that person carefully allocates income across spending categories. Conversely, someone with sophisticated budgeting tools and perfect allocation discipline but biweekly pay still faces the coordination challenge we're about to describe. The difference is structural, not behavioral—it's about system alignment, not personal discipline.

Biweekly pay shatters this stable pattern completely. The liquidity management challenge doesn't change—you still need to ensure cash is available when bills come due. But the ability to solve it once and rely on a stable pattern disappears entirely.

What makes biweekly pay fundamentally different is that your income and your bills are no longer operating on the same system. Your bills remain anchored to the calendar just like before. But your biweekly paychecks are anchored to something completely different. They're anchored to the weekday. If you're paid every other Friday, your income arrives based on a strict 14-day cycle that has absolutely nothing to do with calendar dates or months. Your paycheck no longer has anything to do with monthly timing. It arrives every other Friday simply because that's when the two-week counter resets.

Each system on its own is perfectly predictable. But when these two predictable systems have to coordinate with each other to answer the question "which paycheck covers which bills?", they never align. The relationship between them is constantly shifting. Your October paycheck might cover two credit card payments, but your November paycheck—arriving just a few days earlier or later in the month—suddenly needs to cover one credit card payment plus rent and a car payment.

The bills didn't change. Your income didn't change. But which paycheck is responsible for which obligations completely shifted because the 14-day rhythm and the monthly rhythm slid past each other. This happens every single month. The pattern never stabilizes. You can't learn it once and then rely on it. You have to recalculate it fresh every few weeks as the two misaligned systems continue their endless slide past each other.

This is why you feel like you're constantly doing mental math. This is why you can't seem to internalize a system that just works. This is why you're always checking and rechecking whether you're safe — and why, when the math doesn't work out, the result is overdraft fees that hit the same households repeatedly. The liquidity management problem that people on monthly or semi-monthly pay solved once and then forgot about is something you have to actively solve over and over again. The pattern never becomes automatic. It can't become automatic because it's never the same pattern twice.

The exhaustion you feel isn't from a lack of discipline or organization. It's the natural result of trying to manually coordinate two systems that are fundamentally misaligned and will never sync up.

Now we can see clearly why the advice to budget better doesn't fix the struggle you're experiencing with biweekly pay. Budgeting is a tool for resource allocation. It helps you decide how to divide your income across competing priorities. But biweekly pay doesn't create an allocation problem. It creates a coordination problem between two systems operating on different rhythms.

This is why advice like "try zero-based budgeting" or "use the envelope method" helps at the margins but doesn't eliminate the core struggle. These are more rigorous frameworks for allocation. They force you to be more intentional about every dollar, which is genuinely valuable. But they're still fundamentally about deciding how to divide your money across categories. They don't address the timing question at all. They don't tell you what your checking account balance will be on the 12th when specific bills hit. They don't show you whether you're on track to dip dangerously low between paychecks. They can't, because that's not what they're designed to do.

The problem isn't that you need to budget harder or better or more carefully. The problem is that budgeting—no matter how well executed—is the wrong tool for the challenge you're facing. You're trying to use an allocation tool to solve a coordination problem. It's like trying to use a hammer to tighten a screw. The hammer isn't defective. It's just not the right tool for what you're trying to accomplish. The reality is that budgeting and forecasting solve fundamentally different problems — and biweekly pay exposes exactly where the gap is.

Once you understand that biweekly pay creates a coordination challenge rather than an allocation challenge, the path forward becomes clear. You need to address the coordination problem directly—and there are two fundamental ways to do this.

The first approach is to change your financial position so that timing becomes irrelevant. If you can build enough cushion that you're always using last month's income to fund this month's expenses, the coordination problem essentially disappears. When you're truly one month ahead, that core assumption of budgeting—that your income for a period is available at the beginning of that period—becomes true again. The misalignment between biweekly paychecks and monthly bills still exists structurally, but it no longer affects you because you've decoupled when bills get paid from when paychecks arrive.

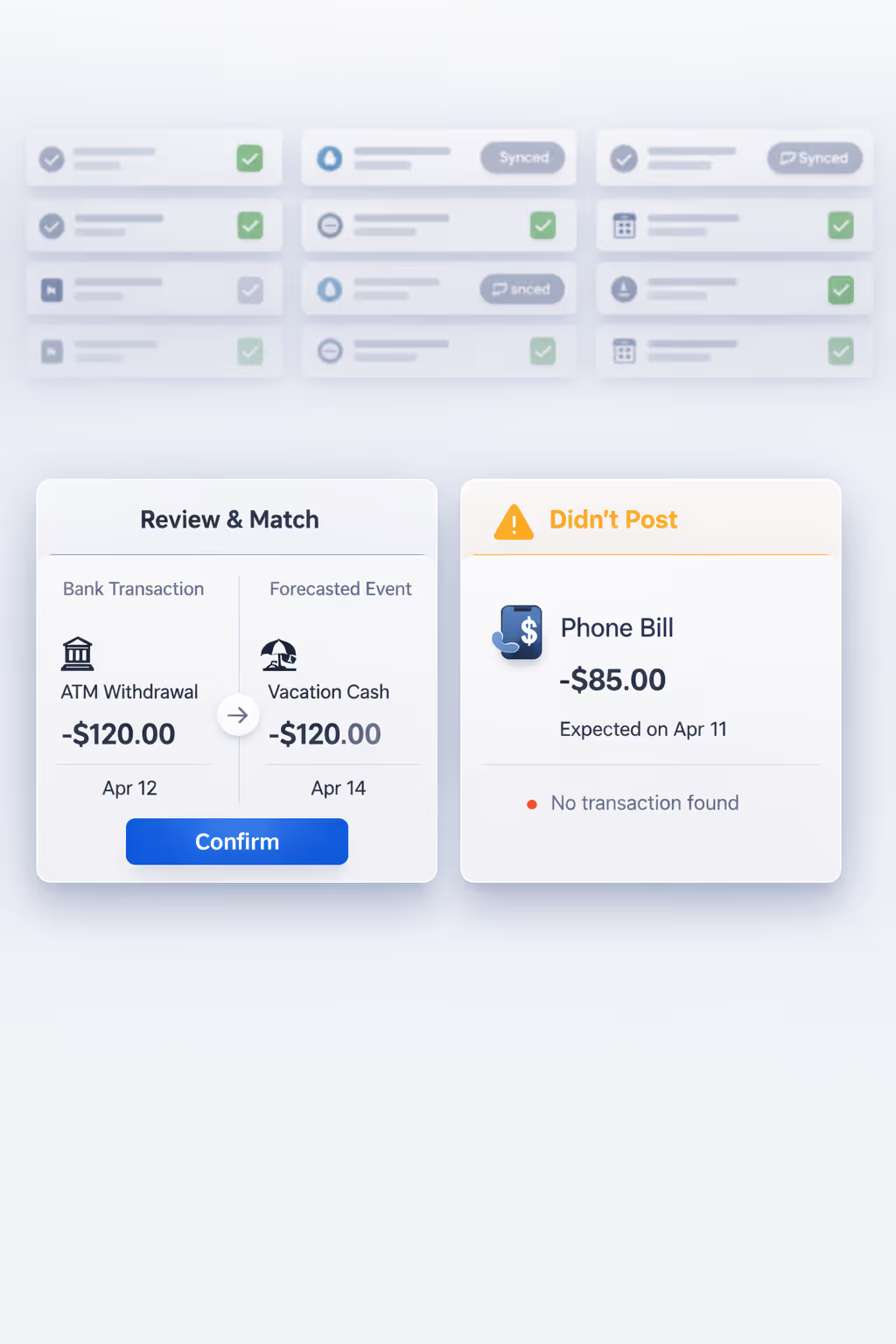

The second approach is to gain forward-looking visibility into how your paychecks and bills will coordinate over time through checking account cash flow forecasting. You don't eliminate the coordination problem, but you make it explicit rather than invisible. You can see the actual timeline of how cash will flow through your account as these misaligned systems interact, which allows you to identify tight spots before they happen and make decisions based on what's actually coming rather than guessing and hoping. Instead of staring at your balance and wondering whether it's safe to spend, you can see how much is genuinely available. The mechanics behind that visibility — how the forecast simulates your checking account forward day by day using your actual paycheck rhythm and bill schedule — are what make the coordination between those two misaligned systems concrete and inspectable rather than something you're constantly recalculating in your head.

So how do you actually implement these approaches? How do you build buffer strategically without creating new problems? How do you gain the forward-looking visibility you need to manage cash flow confidently? That's where we turn from understanding why biweekly pay is hard to learning the specific tools and methods that make it manageable.

STAY A STEP AHEAD