How Centinel's checking account forecast works under the hood: the deterministic 2-month walk-forward engine and its outputs.

May 29, 2026

Most personal finance tools don't explain how they work. Budgeting apps categorize your spending without disclosing their logic. Bank balance projections don't reveal their assumptions. When a tool produces a number, you're expected to trust it without understanding where it came from.

Centinel takes the opposite approach. The forecast is built on a methodology transparent enough to explain in plain language — and understanding it makes the outputs meaningfully more useful. This article is that explanation: what goes into Centinel's checking account cash flow forecast, how the engine processes it, and what it produces — including the specific design decisions that make the forecast reliable rather than misleading.

Centinel's forecast has four layers: a design philosophy (deterministic calculation rather than AI prediction), the inputs (your current balance and your defined cash flow events), the engine (a walk-forward algorithm that steps day by day through a 2-month window), and the outputs (Account Low, a dual-threshold comparison, and proactive alerts). A fifth concern — keeping the forecast accurate as reality unfolds — runs underneath all of them. Everything that follows takes these in turn.

Everything about how Centinel's forecast works follows from a single architectural choice: it's deterministic, not predictive. That decision governs the inputs it asks for, the way the engine processes them, and why you can trust what it produces.

A deterministic forecast calculates projected balances from the cash flow events you have explicitly defined. A predictive forecast uses machine learning or pattern recognition to infer future transactions from historical spending data. Both produce a projected balance trajectory, but they work from fundamentally different assumptions — and those assumptions have practical consequences for reliability, transparency, and responsiveness.

Deterministic forecasting is the right architecture for short-term checking account cash flow projection for three reasons.

Immediate Responsiveness to Changes. When you update a pay date, adjust a bill amount, or add a new recurring expense, a deterministic forecast recalculates instantly because the engine is working directly from the updated inputs. Predictive models need weeks of new transaction data before they can adjust to a changed pattern. The model's internal weights were trained on the old pattern, and the new pattern has to accumulate enough data points to shift them. So a predictive forecast lags behind reality precisely when your situation is changing — which is exactly when forecast accuracy matters most.

No Historical Data Required. You get a fully functional forecast from Day 1 once you've entered your cash flow events. Predictive models require a cold-start period of accumulated history before they can generate meaningful projections. The tool is therefore least useful when you need it most: right after onboarding, when there's no track record in the system.

Full Transparency of Assumptions. You always know exactly what the forecast is based on — your balance and the events you've defined. There is no opaque model making inferences you can't inspect or override. If the forecast is wrong, you can identify exactly which input caused the discrepancy and correct it. With a predictive model, a wrong forecast is much harder to diagnose, because you can't see what patterns the model inferred or what weights it assigned.

The Tradeoff. The honest tradeoff is that deterministic forecasting requires more upfront effort. Rather than connecting an account and waiting for a model to learn, you need your recurring events identified and entered. Centinel reduces that cost by detecting your recurring events from your transaction history during onboarding and asking you to confirm them — but the setup step is real and shouldn't be glossed over. What you get in return is a forecast you can fully understand and trust, because every assumption in it is visible.

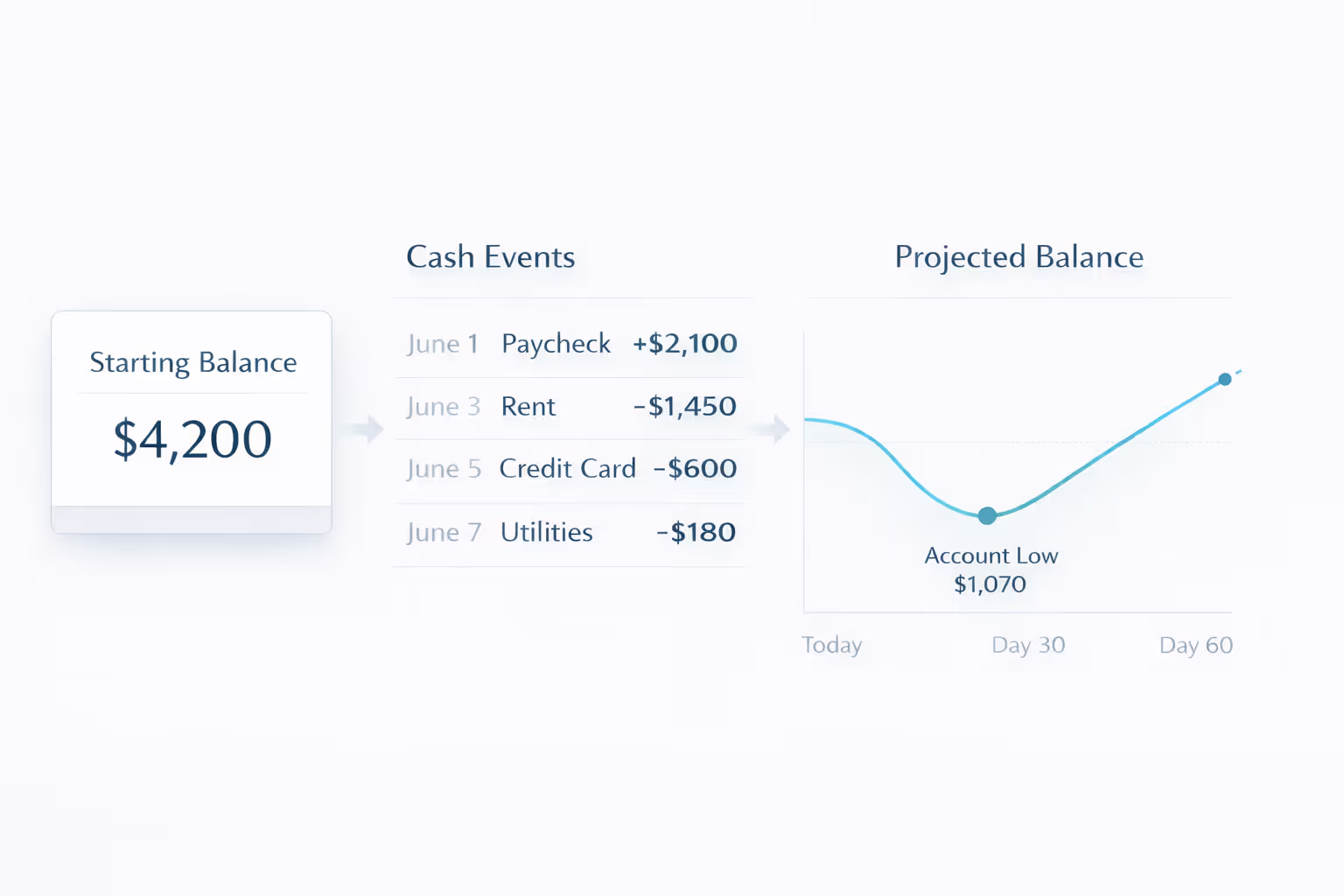

Because the forecast is deterministic, it works from inputs you define rather than patterns it infers. There are two: a starting balance and a cash flow schedule. The quality of those inputs determines the quality of everything the forecast produces.

Every forecast starts with a known, real number: your actual checking account balance right now. Not an estimate, not a historical average, not a projection from yesterday's number — the real balance as of today.

This matters more than it might seem. A forecast that starts from an approximate balance inherits that error across every subsequent day. If the starting balance is off by $200, every projected daily balance in the window is off by $200 before any other discrepancy is introduced. Starting from the real number eliminates baseline error at the source.

Centinel pulls your real checking balance each day via Plaid and re-anchors the projection to that number automatically. This daily refresh means the walk-forward always starts from where the account actually is today, not from where the forecast calculated it should be yesterday. Drift — the gradual divergence between projected and real balances that accumulates when a forecast runs from a stale starting point — is eliminated by design.

The second input is your complete set of defined cash flow events: every recurring income source, every recurring expense, and any known one-time items. Each event has four attributes: an amount, a direction (income or expense), an anchor date, and a frequency. Centinel supports nine frequencies — one-time, daily, weekly, biweekly, semi-monthly, monthly, quarterly, semi-annual, and annual — so the schedule can represent your actual cash flow pattern rather than forcing everything into a monthly approximation.

During onboarding, Centinel analyzes your recent transaction history, detects the recurring patterns in it, and surfaces them for you to confirm — so most of your schedule is built from your real bank data rather than from memory. Adding the rest is a matter of selection, not data entry: when you add income or an expense, Centinel surfaces your bank transaction ledger, filtered to inflows or outflows depending on which you're adding, and you turn a real transaction into a recurring event with a tap. If something isn't in the feed yet, you can enter it manually. And events aren't fixed at onboarding: you can add a new one at any time from the floating + button, so the schedule keeps pace as your financial life changes.

Some recurring events behave differently from the rest. Credit card payments are the main case: the amount is variable and isn't known until the statement closes, so Centinel handles them automatically. You connect the card via Plaid (read-only), set a payment preference — full statement balance, minimum payment, or a custom fixed amount — and select the payment date, such as the card’s due date or a custom day of the month. As each billing cycle closes, Centinel detects the new statement and updates the forecast so the right credit card payment appears on the right date.

Centinel takes one more input beyond cash flow events: the Floor. The Floor is the minimum balance you want to maintain in your checking account at all times. It isn't a cash flow event — it doesn't add to or subtract from projected balances. Its role is in the output layer, where the forecast's projected balance is compared against it to determine whether your checking account is safe or at-risk.

With the philosophy and the inputs established, here's how the engine works.

Starting from today's real checking balance, Centinel's algorithm steps forward one day at a time across the 2-month forecast horizon. On each day, it checks whether any scheduled cash flow events fall on that date. Expenses reduce the projected balance; income increases it; when both fall on the same day, expenses are applied first to err on the side of caution. The result is a projected balance for that day, which becomes the starting point for the next. Days with no scheduled events carry the previous balance forward unchanged. By the end of the horizon, the algorithm has produced a complete day-by-day trajectory — a projected balance for every day across the next 2 months.

The following table shows the first 14 days of a forecast for an individual with a starting balance of $1,900, biweekly pay of $1,750, and a typical set of monthly expenses. Days with no scheduled events are omitted — the balance simply carries forward.

The 2-month horizon isn't arbitrary. It's the span where the forecast is long enough to be useful and short enough to stay accurate.

A shorter horizon is often too late. If you only look 1-2 weeks ahead, you may miss the bill cycle that actually creates the problem. A paycheck can make today’s balance look comfortable, while a rent payment or credit card draft just beyond the window can still push the account uncomfortably low. A short forecast can show what is about to happen, but it often does not give you enough foresight to see the next real cash-flow pinch or enough time to plan around it.

But the horizon cannot be too long either. The further out a cash-flow forecast reaches, the more it depends on assumptions. Like a weather forecast, it becomes less reliable the farther it looks into the future. A forecast 6 months from now is mostly guesswork. Cash flow works the same way. 6-12-month projections can help with broad planning, but they are less reliable for day-to-day checking-account decisions because too many things can change.

2 months is the middle ground. It is long enough to capture more than one cycle of most recurring household cash flows, but short enough that the forecast can still be grounded in real paychecks, bills, transfers, and known events. That makes it long enough to matter and short enough to trust.

Once the walk-forward is complete, Centinel has a projected balance for every day of the 2-month window. The algorithm scans them all and identifies the projected minimum balance over the entire forecast window – the Account Low.

Account Low is the most important number the forecast produces, because it represents the tightest day: the single point in the next 2 months when the checking account is under maximum pressure. Every other day in the window has a higher projected balance. If the account can get through the tightest day, it can get through every day.

Account Low is a number. It becomes actionable when compared against thresholds that represent meaningful risk levels. Centinel compares Account Low against two thresholds, producing two possible forecast states.

Centinel compares Account Low against two thresholds. The first is $0: if Account Low is projected to go below zero, the account is projected to overdraft. The second is the Floor — the minimum balance you want to stay above, which you define yourself. The Floor is the early warning that fires before overdraft territory is reached.

Safe. Account Low is at or above your Floor: your balance is projected to stay at or above your minimum comfort level throughout the forecast. In this state, Centinel surfaces Available Cash: Account Low minus Floor, which is how much is safe to spend or move out of checking — to savings, investments, or debt paydown — without ever dipping below your Floor, even on your most constrained day.

At-Risk. Account Low is below the Floor, or below $0. This state raises an immediate question: when does the problem occur, and how much is needed to fix it? Centinel answers with two metrics — First and Total Needed.

Account Low tells you the worst point in the balance trajectory, but not the first point. These can be different days. That distinction matters because the most urgent problem and the most severe problem may require different responses on different timelines.

To illustrate, consider the following example:

Centinel surfaces two metrics from this trajectory.

First is the date and amount of the earliest projected overdraft: March 3, -$150. This is the most time-sensitive signal, because it defines how much lead time you actually have. If today is February 24th, you have 7 days to address the first problem.

Total Needed is the amount required to cure all overdrafts across the entire 2-month window: $540 — the Account Low. Here's why that single number works: the forecast is a connected, day-by-day calculation, so depositing $540 today raises every projected balance uniformly by $540. Account Low on April 16 goes from −$540 to exactly $0 — the overdraft is eliminated. The March 3 shortfall goes from −$150 to $390 — well above $0. One deposit, sized to the worst point, cures every overdraft in the window.

The distinction between First and Total Needed prevents two mistakes. The first is underreacting — ignoring the March 3 overdraft because it's smaller and assuming the bigger number is the only one that matters. The March 3 overdraft will trigger real fees in 7 days regardless of what happens in April. The second is overreacting — scrambling to produce $540 immediately when the most urgent need is $150 and there are 6 weeks to plan for the remaining $390. Knowing which problem is first and which is worst lets you respond deliberately rather than reactively. You might triage — cover the $150 now and build toward the remaining $390 with the lead time the forecast gave you — or deposit the full $540 today and clear the entire window with a single transfer. Either way, you're deciding with complete information about what's urgent, what's severe, and how much time you have.

A forecast that surfaces risk only when you open the app leaves value on the table. The point of identifying a future shortfall is to act on it before it arrives — and that requires the information reaching you proactively rather than waiting for you to come looking.

Centinel translates the forecast outputs into push notifications. When the forecast detects that Account Low has crossed below the Floor or below $0, Centinel sends a notification containing three things: the current forecast status, the date or dates in question, and the shortfall amount. Not a vague "balance is getting low" message — a specific, forward-looking warning that names when the problem will occur and how short the account is projected to be.

This is fundamentally different from a standard bank low-balance alert. A bank alert fires after the balance has already dropped below a threshold; it reports a problem that has already happened. By the time you read it, the overdraft fee may already be assessed and the transaction already declined. Centinel's alerts fire when the forecast crosses a threshold — meaning the problem is projected to happen days or weeks from now, with enough lead time to prevent it entirely.

The walk-forward explains how the forecast is built. But a forecast calculated once is only accurate until something changes — a transaction posts late, an amount differs from what was scheduled, an unexpected charge appears. Accuracy rests on the same two inputs the forecast started with: the balance and the events. Keep both current and the forecast stays trustworthy; let either drift and the numbers quietly stop meaning anything.

Centinel keeps them current through two mechanisms — one for each input. Balance anchoring keeps the starting balance fresh via the daily Plaid resync described above. Reconciliation — the heavier lifting — keeps the cash flow events current.

Reconciliation is the ongoing process of comparing what the forecast projected against what actually posted to your bank, and resolving the difference. Centinel’s automated core is transaction matching: each posted transaction is scored against your scheduled events on four signals — amount, date, merchant, and category — and the high-confidence cases resolve silently, capturing the real amount and recalculating the forecast without involving you. The cases that need a human judgment call surface for review: a transaction that posted but couldn't be confidently matched, or a forecasted event that was expected but never appeared.

Together, balance anchoring and reconciliation keep the forecast accurate and actionable.

Forecasting only helps if you trust it, and trust requires understanding. This article exists so that anyone evaluating Centinel's methodology can see exactly how it works and judge for themselves whether the approach is sound. The principles described here are not proprietary. They are adapted from decades of corporate treasury practice and made accessible to individuals rather than Fortune 500 finance teams.

Centinel is currently accepting early access signups.

STAY A STEP AHEAD