Biweekly and semi-monthly pay look similar, but they affect your finances differently. Learn how each schedule works and why the difference matters.

June 2, 2026

A job offer says you'll be paid biweekly, or your employer switches you from semi-monthly, and the two words start to blur. They sound like the same thing said two ways — both land somewhere around twice a month — so it's easy to treat them as interchangeable. They aren't. They differ in one structural way, and while the difference sounds trivial when you state it, it changes how your pay lines up with your bills for as long as you hold the job.

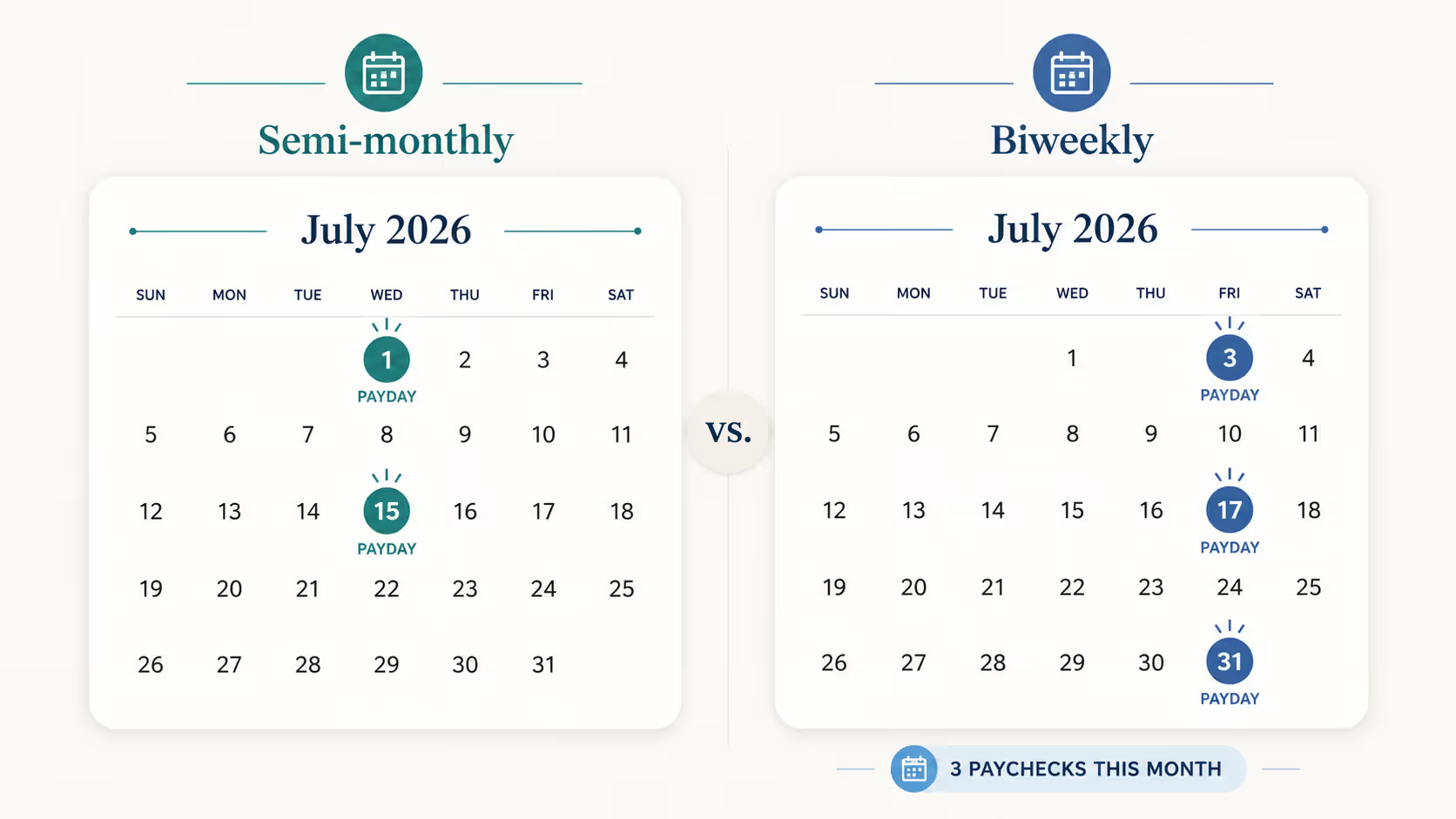

Semi-monthly pay arrives twice a month on fixed calendar dates — usually the 1st and the 15th, or the 15th and the last day of the month. That's 24 paychecks a year, two in every month, each one the same size.

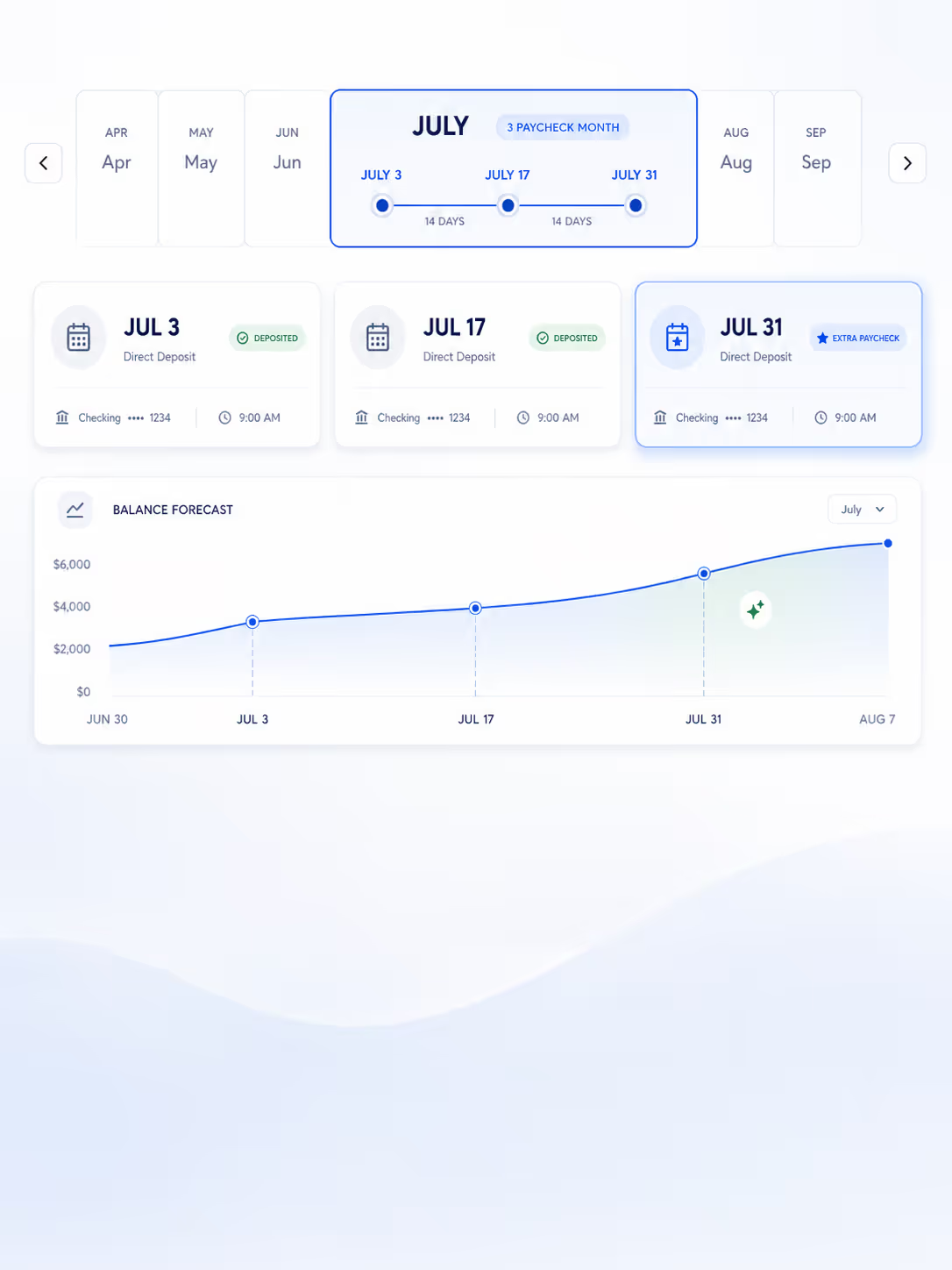

Biweekly pay arrives every two weeks on a fixed weekday — e.g., every other Friday — regardless of the date. Fourteen days, then payday, on repeat. Because a year holds slightly more than 52 weeks, that comes to 26 paychecks a year, and occasionally 27, rather than 24.

Two consequences fall out of that table. The first is paycheck size: on the same salary, semi-monthly checks are a little larger, because the year's pay is split into 24 pieces instead of 26 — though the annual total is identical either way. The second is that biweekly pay produces 26 checks, which is why two months each year give you a third paycheck instead of the usual two.

The confusion is understandable. Both schedules drop money into your account roughly twice a month, and over a year the difference is just two extra checks. If all you're tracking is how much you earn, the two are close enough to feel identical.

But the difference that matters isn't how much or how often. It's what each schedule is anchored to. Semi-monthly pay is anchored to the calendar — the 1st, the 15th, dates that never move. Biweekly pay is anchored to the weekday — every other Friday, which marches through the calendar on its own 14-day rhythm and lands on a different date every time.

That single distinction is virtually invisible on payday. Your paycheck is your paycheck. Where it surfaces is in the relationship between your pay and your bills — and that's where one of these schedules quietly makes your financial life harder than the other.

Your bills run on the calendar. Rent is due on the 1st, the car payment on the 4th, the credit card on the 19th — fixed dates, month after month.

Semi-monthly pay runs on the calendar too. Because your paychecks land on fixed dates, they keep a stable relationship with your fixed-date bills: the 1st-of-the-month check covers the bills early in the month, the 15th check covers the rest, and that mapping holds every month. You learn it once and stop thinking about it.

Biweekly pay doesn't keep that relationship, because it isn't on the calendar's clock. Your paychecks slide forward two days, then two more, drifting against your fixed bill dates until the alignment that worked last month doesn't work this month. One month a mid-month paycheck clears the credit card before rent is due; the next, the same check lands later, rent clears first, and the timing is suddenly tight. Your income didn't change and your bills didn't change — only which paycheck is responsible for which bill, and that shifts on its own every month.

This is why the same person who coasted on semi-monthly pay can feel like they're scrambling on biweekly pay despite earning the same money. It isn't a discipline problem and it isn't a math problem. It's a timing problem, created by two schedules running on two different clocks — and it's exactly the problem that budgeting on biweekly pay has to be built to handle, because a budget that only tracks monthly totals can't see it coming.

Neither schedule pays you more. On the same salary, semi-monthly and biweekly deliver the identical annual total — semi-monthly in 24 larger checks, biweekly in 26 smaller ones plus two months that carry a third. If you're choosing between two jobs and the only difference is the pay schedule, it's not a real difference to your bottom line.

The honest answer to "which is better" is that the question is about your budget, not your pay. Semi-monthly is easier to budget because it aligns with your bills automatically. Biweekly is harder because it doesn't — but harder isn't unmanageable. The misalignment is predictable; it just has to be made visible instead of carried in your head. If your pay is biweekly, the schedule isn't something to fix. The timing is something to see.

No. Semi-monthly pay arrives twice a month on fixed dates (such as the 1st and 15th), for 24 paychecks a year. Biweekly pay arrives every two weeks on a fixed weekday, for 26 paychecks a year — sometimes 27. They land at similar frequencies but on different schedules.

Not exactly. Biweekly pay is every two weeks, which usually works out to twice in a month but produces a third paycheck in two months each year. Semi-monthly pay is the one that's truly twice a month, every month.

Semi-monthly pay gives you 24 paychecks a year. Biweekly pay gives you 26, and 27 in certain years, depending on when your first payday of the year falls.

Neither. The annual total is identical. Semi-monthly splits it into 24 larger checks; biweekly splits it into 26 smaller checks plus two three-paycheck months. The difference is timing, not amount.

The main one is budgeting. Because biweekly pay follows a weekday cycle while your bills follow calendar dates, the two drift against each other and which paycheck covers which bill changes every month. That makes it harder to know whether your account will hold on any given date, even when your income comfortably covers your expenses.

For ease of budgeting, semi-monthly has an edge, because it lines up with monthly bills automatically. For pay, they're equal. And biweekly's timing challenge is solvable once you can see your balance projected forward rather than guessing at it.

STAY A STEP AHEAD