PocketSmith plans your long-term financial life; Centinel forecasts your checking account day by day over two months. See which fits you.

June 4, 2026

PocketSmith and Centinel both forecast your cash flow, and both do it the same fundamental way: a deterministic, calendar-based projection that walks your balance forward from known inputs, rather than a statistical guess.

PocketSmith plans your whole financial life across years, even decades. Centinel answers a narrower, more immediate question: will your checking account survive the next two months, and what's safe to spend right now? That difference in purpose runs deeper than it looks — it reaches all the way down to what each app treats as the basic unit of a forecast — and it's why the two are best understood as adjacent rather than head-to-head. One is a long-range planning instrument; the other a short-term liquidity tool. A person with both needs is plausibly served by both.

Disclosure: we make Centinel, so we have a stake in this comparison. We've worked to represent both tools accurately, and where PocketSmith is the better tool, we say so.

PocketSmith's forecast is a long-range planning canvas — a view of where your entire financial picture is headed over years. Centinel's forecast is a single-account liquidity engine — it tells you whether your checking account can absorb what's coming over the next two months and hands you specific numbers to act on.

PocketSmith is built around a calendar that projects your future balances from your budgets — your categorized income and spending. It connects checking, savings, credit cards, loans, and investments; tracks net worth; supports multiple currencies; and lets you layer "what-if" scenarios on top — model a raise, a house, a wedding, a change in spending — and compare how each one bends the trajectory. Its forecasting calendar is consistently the feature its users praise most, and for long-range, multi-account, multi-currency planning, it's one of the strongest consumer tools available. Its natural user is the "household CFO": financially engaged, juggling several accounts, often planning major life events years out.

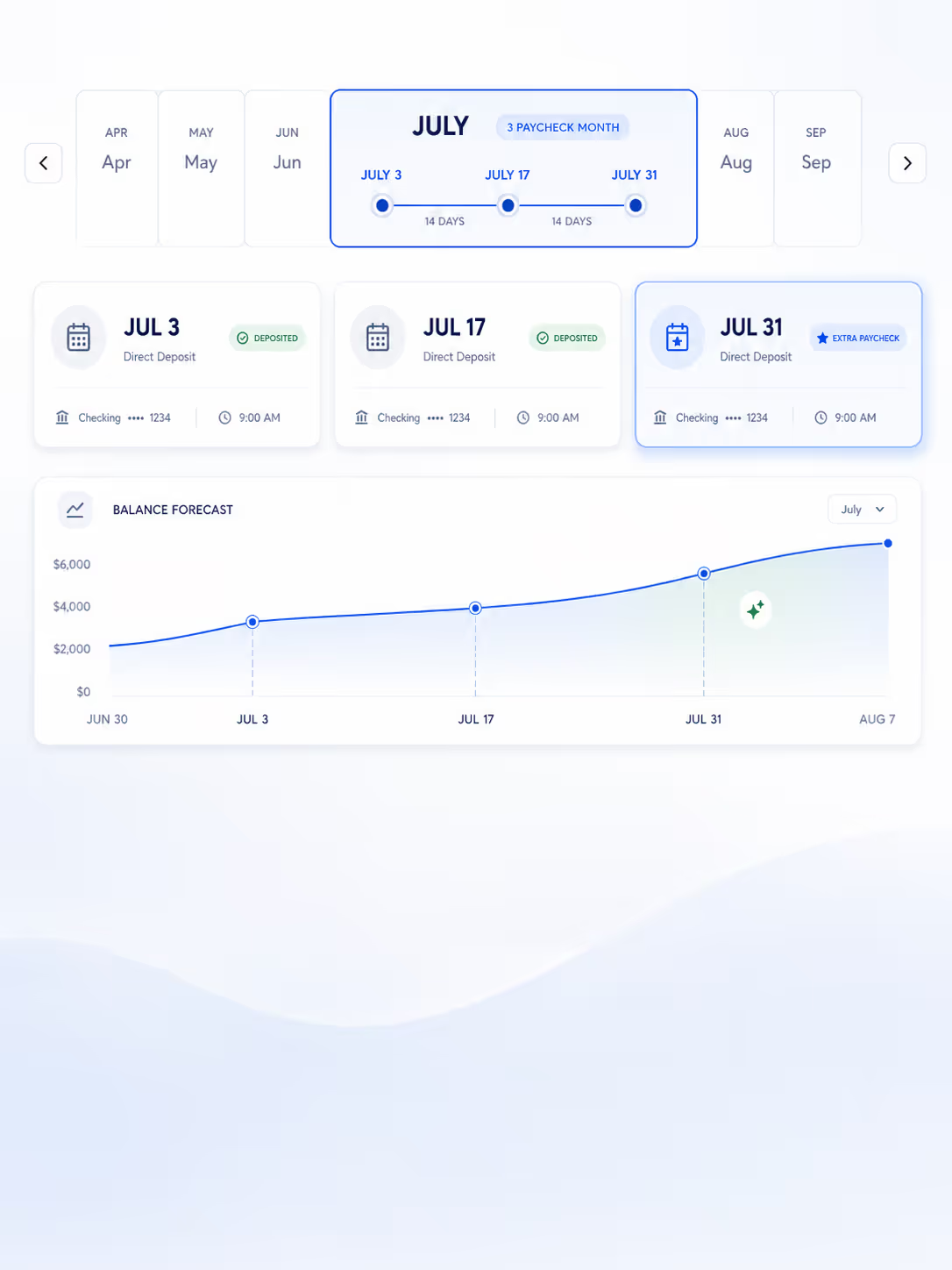

Centinel's checking account forecast is the whole product: a two-month, day-by-day projection of your checking account. Every feature — the ledger, the action metrics, the reconciliation system, the alerts — exists to serve it.

The forecast answers two questions. First, is the account safe? Centinel projects your balance for every day over the next two months and checks each day against both $0 and a personal threshold you set, called your Floor. If you stay above your Floor the whole window, you're in good shape — and Centinel tells you the surplus you have to spare, based on the lowest point your balance is projected to reach. If you're headed below your Floor or below $0, it tells you when and by how much, so you can act before it happens. The horizon is short on purpose: two months is far enough to catch bills that aren't imminent yet, and close enough that a day-by-day projection stays reliable.

Both apps connect to your accounts, re-anchor the forecast to your real balance as it changes, and project forward from there. The differences are in how far each one reaches in daily detail, what data drives the projection, how it keeps up as life happens, what it hands you at the end, and what it asks of you.

PocketSmith projects from six months to sixty years out, depending on tier; Centinel projects two months. But the sixty-year figure is upmarket positioning, not a daily forecast: PocketSmith shows daily balances only about three months out, and switches to weekly balances beyond that. Centinel shows daily balances across its full two-month window.

This is the deepest difference between the two products, and it's easy to miss because both apps look similar on the surface. In PocketSmith, the basic unit of a forecast is a budget — a recurring amount tied to a category, like "$400 a week on groceries." The forecast is a byproduct of those budgets: to put anything on the calendar, it has to flow through a category and a budget. In Centinel, the basic unit is the cash flow event — a single dated event on your checking timeline, like "rent, $1,800, on the 1st" or "vet bill, $300, next Thursday." There's no category layer in between.

That sounds abstract, but it shows up the moment your cash flows don't line up with categories. Three different credit-card payments due on three different dates are, to a forecast, just three outflows — but in PocketSmith they share the "credit card payments" category, and the app steers you toward building sub-categories to keep them from colliding in its budgeting math. Category envelopes are genuinely better for life planning, where "about $400 a week on food" is exactly how you think years ahead. But for short-term checking liquidity, where one bill landing on the wrong day can swing your balance by hundreds of dollars, the budget layer adds setup and abstraction between you and the question you're trying to answer.

When a transaction posts, the two apps reconcile it differently — and this is where short-term accuracy is won or lost. PocketSmith counts a posted transaction toward its category's budget for the period rather than matching it to a specific scheduled event, and it re-anchors the forward forecast to your current actual balance. What it doesn't do is pair "this transaction" with "that expected event." PocketSmith's own troubleshooting documentation describes the consequences: pay a bill early or late and the budgeted event stays in the forecast, double-counting against your balance until you manually drag it to the date it actually happened. And if a scheduled payment simply doesn't post on its expected day, the re-anchored forecast reflects a balance that's still carrying money you've effectively already committed — so it can read more optimistically than reality until you move the event or turn on Safe Balance (described below) to carry it. For a long-range planner, these are minor housekeeping tasks. For a day-by-day checking view, they're the difference between a number you can trust and one you can't.

Centinel matches each posted transaction to its scheduled event automatically, removes it from the forward projection, and alerts you about anything that doesn't line up — a projected charge that didn't post, or an unexpected one that did. You can resolve the discrepancy in a couple of taps. The forecast detects the mismatch rather than waiting for you to notice it, and it stays grounded in confirmed inputs rather than drifting. Both apps re-anchor to your actual balance; the difference is at the level of the individual event, and that's the level that decides whether tomorrow's projected balance is trustworthy.

PocketSmith hands you a picture to interpret: a calendar of projected balances, scenario comparisons, net-worth curves, and reports — even a view of how an earlier forecast compared against what actually happened, which is a useful diagnostic for a planning tool. You read the trajectory and draw your own conclusions.

It also has a feature aimed squarely at "how much can I spend right now," called Safe Balance, and understanding it requires a distinction that's the real crux of this comparison. "Safe to spend" can mean two different things. One is a budgeting question: given my income and what I've allocated and spent this period, what’s available for me to spend? The other is a checking account question: given current balance and scheduled inflows to and outflows from checking account, will my checking balance stay above my cushion, and if so, how much is available above that to spend? They sound alike but run on different inputs — the budgeting question is about category allocations over a period and barely cares about your balance or which account money moves through; the checking account question is about dated dollars entering and leaving one specific account.

PocketSmith’s Safe Balance answers a narrower question. It starts from your current balance and subtracts the unspent portions of selected budgets, giving you a today-based safe-to-spend number rather than a day-by-day projection of where your checking balance is headed. That is useful for budget-minded users, but it is not the same as a liquidity forecast. PocketSmith also notes practical limits: Safe Balance is beta, opt-in, unavailable in the mobile app, and depends on repeating budgets rather than standalone one-off budgets. That matters because checking risk often comes from timing-specific events — a card payment, rent draft, annual bill, or one-time repair — not just whether a category has budget left.

Centinel's ‘Available’ metric is purely the checking account liquidity answer. How much is safe to spend is your lowest projected balance over the next two months minus the Floor you set, with every dated event already in the forecast — recurring or one-off, and a credit-card payment counted as the single outflow it actually is on the checking account, no matter what was bought. There's nothing to include or exclude and nothing to configure. It's the consumer version of what a corporate treasurer does: not "are we within budget?" but "will we have the cash to cover what's coming?"

PocketSmith is powerful, and that power has a cost in both senses. It is a deep, flexible tool with more setup and maintenance than a simpler checking-focused app, and its richest experience is still centered on the web app. PocketSmith does have iOS and Android apps, but the company describes them as companion apps rather than standalone products, with a streamlined version of the full web feature set. That matters for forecasting: although the mobile apps can show calendar budgets and forecast balances, PocketSmith’s broader planning workflow is still built around the full web product. Its forecast horizon and account connections are also tier-gated: the free plan is limited to 2 accounts and a 6-month projection, while the longest projections and most connected banks sit on upper plans, up to $26.66 per month billed annually — about $320 per year — or $39.95 billed monthly.

Centinel is the opposite shape: one job, built for the phone, minimal configuration/upkeep. Its free tier covers manual entry; the premium tier — bank connectivity, automatic syncing, reconciliation, and alerts — is $6.99 a month or $59.99 a year, with a 30-day free trial. You're not paying for breadth, because there isn't any. You're paying for one forecast, on your phone, kept accurate.

It depends on what you use PocketSmith for. If you use it to plan across years — net worth, scenarios, multiple accounts and currencies, long-range projections — Centinel replaces none of that. It doesn't budget, doesn't track investments, doesn't model decades, and touches only your checking account.

But if the reason you opened PocketSmith was to see the near-term future of your checking account — to know whether the balance survives the month and what's safe to spend — then yes, Centinel is a PocketSmith alternative: a focused, mobile-first, short-term checking forecast. If you want both the long view and the short one, they run side by side.

Choose PocketSmith if you want to plan your whole financial life: long-range projections, what-if scenarios, net worth, multiple accounts and currencies, and the reports to match. It's one of the few consumer tools that genuinely forecasts years out, and if that's the question keeping you up, the depth earns its price — provided you're comfortable doing that work on the web and maintaining your categories and budgets.

Choose Centinel if your live question is in the next two months, not the next sixty years — whether your checking account covers what's coming, how much room you have, and when a shortfall lands — and you want a specific, trustworthy number about one account, on your phone, rather than a trajectory to interpret.

The two aren't mutually exclusive, and they barely overlap: PocketSmith for the long arc and the overall picture, Centinel for short-term checking account liquidity. If you're deciding which to set up first, start with whichever question is actually pressing for you.

Centinel is currently in pre-launch. If you'd like to be among the first to try it, you can join the waitlist.

Yes — it's PocketSmith's defining feature. A calendar-based, deterministic forecast projects your future balances from your budgets, with what-if scenarios you can layer on top. It spans all your connected accounts, not just checking, but it's built for long-range planning, not short-term checking account liquidity.

The projection window is tier-gated: six months on the free plan, ten years on Foundation, thirty on Flourish, and up to sixty years on Fortune. One caveat worth knowing: in PocketSmith’s forecast graph, daily balances are shown only up to three months into the future, with weekly balances beyond that. So the longer horizons are best understood as planning-grade projections rather than the same kind of near-term, day-by-day checking view.

Safe Balance is PocketSmith’s “how much can I spend right now” feature. It takes your current balance and subtracts the unspent portion of the budgets you choose to include — a present-day snapshot against your remaining plan. It’s budget-based rather than forecast-based, so it does not walk your balance forward to find your lowest future day. It also depends on repeating budgets: standalone one-off budgets do not work, though one-off events can be included when attached to an ongoing repeating budget. By PocketSmith’s own description, Safe Balance is a beta, opt-in feature and is not displayed in the mobile app. Centinel's equivalent, Available, is a forward liquidity number: your lowest projected balance over two months minus the cushion you set, with one-off events included.

PocketSmith’s richest forecasting experience is still centered on the web app, but the forecast is not web-only. PocketSmith’s iOS and Android apps include a Calendar view that can show budget events and forecast balances, while PocketSmith positions Sidekick as a companion to the web app rather than a standalone replacement. So the mobile app can show forecast information, but the full planning workflow is still better understood as web-first.

PocketSmith offers a limited free plan and three paid tiers. When billed annually, Foundation is $9.99/month, Flourish is $16.66/month, and Fortune is $26.66/month. Month-to-month pricing is higher: Foundation is $14.95/month, Flourish is $24.95/month, and Fortune is $39.95/month. Rather than advertising a time-limited free trial, PocketSmith offers a 14-day money-back guarantee on paid plans, while the free tier works as an open-ended way to try the product.

Centinel offers a free tier for manual entry of recurring transactions. The premium tier — bank connectivity, automated syncing, transaction matching, and push notifications — is $6.99/month or $59.99/year, with a 30-day free trial.

Yes. They solve different problems at different horizons. PocketSmith handles long-range planning and your overall financial picture; Centinel handles short-term checking liquidity over the next two months.

Yes, but in a narrow sense. Centinel is a good alternative if you were using PocketSmith specifically to stay ahead of your checking account in the short term. It is not an alternative for long-range planning, net worth tracking, scenarios, or multi-account budgeting — PocketSmith does those, and Centinel doesn't try to.

STAY A STEP AHEAD