Very few apps actually predict overdrafts before they happen. We evaluated the top apps against 8 criteria to determine the best.

May 2, 2026

Reliably predicting checking-account overdrafts is a key component of avoiding overdraft fees, and it requires a specific architecture: a deterministic forecast that projects your cash flow events forward, transaction reconciliation that keeps it accurate, discrepancy detection, conservative same-day timing, and overdraft risk surfaced as the headline metric. Judged against those criteria, most apps marketed around overdraft prediction are solving a different problem: long-horizon planning tools, cash-advance apps, and bank overdraft protection programs each fall short of genuine short-term prediction in different ways. Among consumer apps, only two have a forecast genuinely capable of surfacing a projected shortfall — Centinel and Quicken Simplifi — and they differ sharply in how well their architecture supports the job. Centinel meets all eight criteria; Simplifi, built budgeting-first, meets some.

This article defines the eight criteria, scores Centinel and Simplifi against each, and explains why several apps commonly grouped into this category are built for something else.

Disclosure: We make Centinel, so we have a stake in this comparison. We've worked to represent every tool fairly and to base our analysis on what the products actually do.

Before evaluating apps, it's worth defining the criteria. The term "predict overdrafts" gets applied loosely — to budgeting apps with forecast features, to cash advance products, to bank protection programs. To do the job genuinely, an app needs to meet the following criteria.

A deterministic forecast projects your saved cash flow events — rent, car payment, paycheck — day-by-day across a designated time horizon, computing each future balance from known inputs. This is the only reliable approach to overdraft prediction. The contrast is a probabilistic forecast, which uses historical patterns to make educated estimates about what will happen in your account. Probabilistic approaches are unreliable for overdraft prediction because patterns change: bills increase, new bills arrive, a one-time charge breaks the average. An app using probabilistic prediction might tell you that you're safe when, in fact, you're not. Genuine overdraft prediction requires actual inputs producing actual projected balances — which leads to the next criterion.

Because the forecast's inputs determine its accuracy, the app needs to make those inputs easy for the user to maintain. At minimum, it should show its work — how the balance rises and falls over time and which events drive each change — and allow the user to update the forecast easily by editing amounts, adding new events, or changing dates. A forecast you can't interact with is a forecast you can't keep accurate, and a forecast you can't keep accurate is one you can't trust.

As transactions post to your bank account, the app needs to match them against the forecast's projected events and remove them so they don't continue affecting future projected balances. Without reconciliation, every transaction that posts in real life remains "still expected" in the forecast, double-counting against your projected balance and corrupting every downstream day. Reconciliation is the mechanism that keeps the forecast aligned with reality as time passes.

Reconciliation handles the easy case — an expected transaction posts as expected. Real life is messier. A projected event might not post (rent was scheduled for Friday and it's now Saturday with no charge). An unprojected event might post (a $500 Venmo charge that wasn't in the forecast). The app needs to detect both cases and surface them to the user. Without this, the forecast silently drifts: is the projected item that didn't post still expected or not? Is the unexpected transaction that posted a new recurring item or just a one-time event? Reconciliation handles matches; discrepancy detection handles everything else.

When income and expenses land on the same day, the order of processing matters. Consider a $500 starting balance with rent of $2,000 due and a $2,000 paycheck arriving the same day. If the paycheck posts first, the balance peaks at $2,500 before settling at $500 — no overdraft. If rent posts first, the balance drops to -$1,500 before recovering — potentially triggering an overdraft, even though the end-of-day result is identical. Banks don't guarantee processing order. An app optimized for overdraft prevention should assume the worst-case ordering (bills first, income second) and surface the worst-case intraday balance, because that's where an overdraft can hide.

The horizon needs to match the question being asked. 2 weeks to 1 month is too short — it can miss larger bills due later in the cycle that should be visible now (e.g., quarterly insurance, a tax payment). 6 months to multiple years is too long — forecast accuracy degrades with distance, the same way weather forecasts do, because every additional day introduces compounding uncertainty. The right horizon for checking-account overdraft prediction is roughly 2 months: long enough to surface bills that are coming but not yet imminent, short enough that the projection remains reliable.

You shouldn't have to navigate, configure, and dig to get the answer you came for: am I going to overdraft, when, and by how much? The headline experience of an overdraft prediction app should be that answer, computed and surfaced as the primary metric. Anything less makes the user do work the app should be doing.

The previous criteria each describe what the forecast must do. This one describes what the app must be. Genuine overdraft prediction requires architectural commitment — the forecast can't be a secondary feature inside an app organized around a different purpose, because every choice an app makes (onboarding flow, navigation hierarchy, notification design, what the home screen shows) reflects what the product is for. An app built around the forecast onboards you by determining your cash flow events. It puts reconciliation front and center. It opens to the forecast and its components. An app built around something else — budgeting, long-term planning, cash advances — can add a forecast feature, but the surrounding architecture won't be optimized for keeping that forecast accurate or for surfacing overdraft risk as the answer to the user's question. Architecture is the difference between an app that can be used for overdraft prediction and an app that's built for it.

Here's how each app performs against the criteria, with detailed analysis below.

Simplifi is a comprehensive personal finance suite with budgeting, net worth tracking, credit monitoring, investment tracking, and a Projected Cash Flow feature. For users who want a generalist PFM, it's a strong choice. Evaluated specifically against the criteria for overdraft prediction, here's how it performs:

Simplifi projects from user-maintained Reminders for recurring bills and income, walking the forecast forward day-by-day and adjusting balances as events occur.

You can add events, edit projections, and see how the forecast arrives at its numbers, but the interaction is friction-heavy. The forecast lives under Bills & Income → Cash Flow and requires both account and duration selection on every visit. The desktop view shows a chart with no running balance unless you hover; mobile shows a ledger with no chart alternative. Reviewing what's matched is the bigger problem: matched items disappear from the forecast view entirely, and to verify or undo a match you have to navigate to the Transactions tab, locate the transaction, and unlink it — a workflow that's only available on desktop.

Simplifi matches posted transactions to projected items and removes them from the forecast. Mechanically, it works. But the user's ability to verify and correct matches is limited, as noted above — without inline visibility into what's been matched, users can't easily tell whether the reconciliation reflects reality.

Simplifi has the underlying data to detect discrepancies but doesn't surface them. If a projected transaction doesn't post, Simplifi keeps it in the forecast indefinitely with no alert. If an unprojected transaction posts, the user gets no prompt to decide whether it's a one-time event, a missed recurring item, or something to match against an existing projection. Detection that isn't surfaced is detection the user can't reliably act on.

Simplifi shows end-of-day balances. There's no setting to opt into worst-case intraday calculation, which is where same-day overdrafts hide.

The horizon is configurable from 2 weeks to 12 months and defaults to 1 month. The user can set it to 2 months, but they have to know to do that — and the configurability itself reflects that the forecast is trying to serve both short-term liquidity and long-term planning.

To see whether you're projected to overdraft, you navigate to Bills & Income, then Cash Flow, then select an account, then configure the horizon, then visually scan for where the line dips below zero. Simplifi does offer a Projected Low Account Balance alert that's on by default, but the user has to choose the threshold — early warning at $500, or breach warning at $0, but not both — and the alert is tied to the default 1-month horizon.

Simplifi is a budgeting-first app. Its onboarding, navigation, and notification architecture are all built around budgeting, with forecasting as one feature among many. The forecast that exists isn't optimized for overdraft prediction specifically — its configurable horizon, end-of-day calculations, and unsurfaced discrepancies all reflect a tool built for trajectory viewing rather than safety decisions.

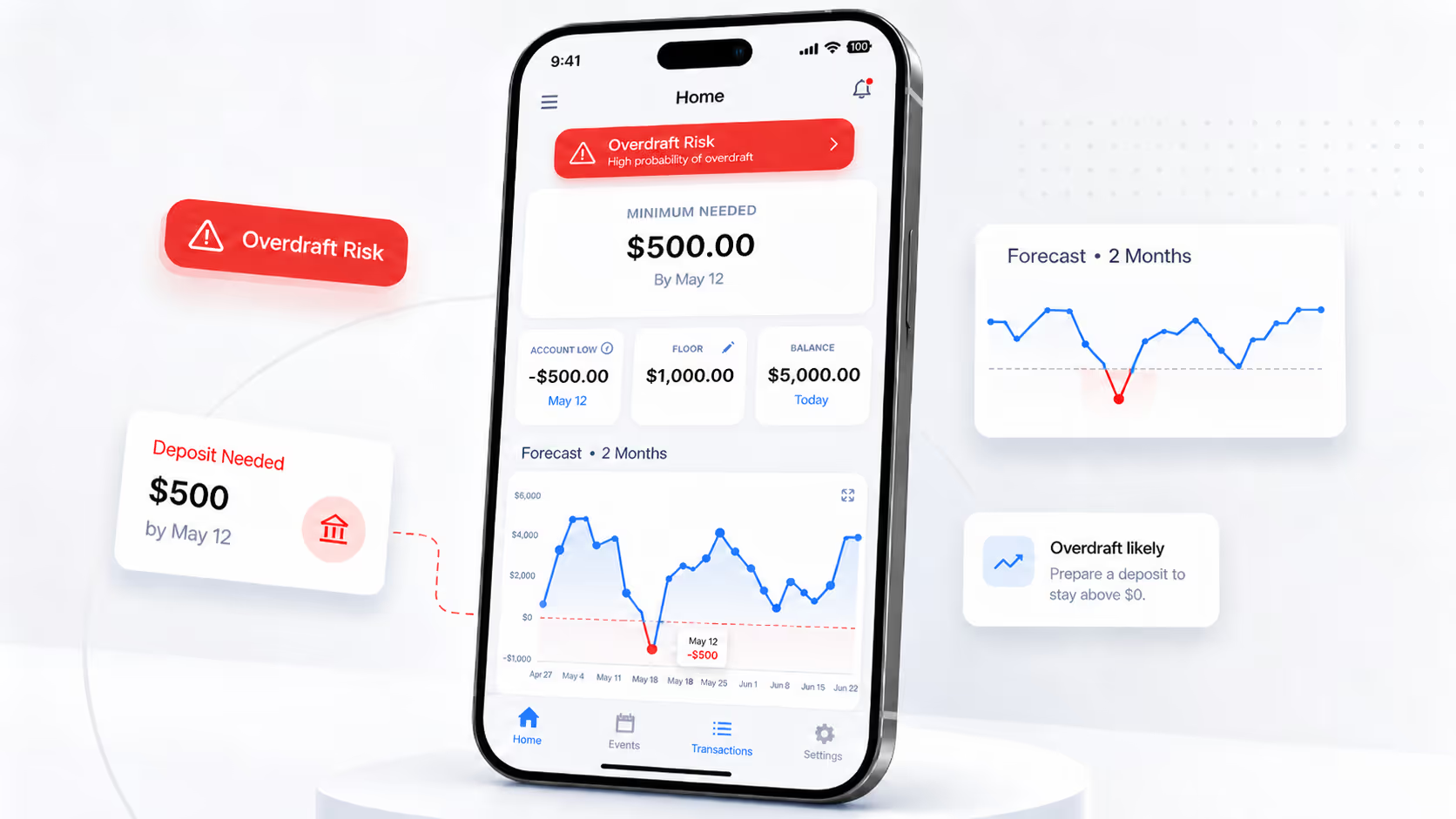

Centinel is architected around a single question: is your checking account safe over the next 2 months, and if not, what should you do? Every feature exists to answer that question and keep the answer accurate.

Centinel projects from your saved cash flow events, walking the forecast forward day-by-day and computing each future balance from known inputs.

The forecast is the home screen. You can add and edit events directly, with three views available — cash flow chart, calendar, and ledger — so you can interact with the forecast in whichever form matches the question you're asking. The ledger shows the math behind every projected balance. Reviewing matched transactions is one click away in the Transactions tab, with full visibility into what was matched to what.

Centinel matches posted transactions to projected items and removes them from the forecast, with inline visibility into match state and one-click access to verify or correct any match.

Both directions are handled and surfaced: when a projected event doesn't post, Centinel alerts the user and lets them decide whether to reschedule it or dismiss it; when an unprojected transaction posts, Centinel surfaces three actions: dismiss as a one-time event, match it to an existing projected item, or add it as a new recurring event. Three actions, three explicit opportunities to keep the forecast accurate.

When income and expenses are projected to land on the same day, Centinel assumes the expense clears first and surfaces the worst-case intraday balance — the number that actually matters for overdraft prevention.

Centinel uses a fixed 2-month forecast. The fixed horizon is intentional: 2 months is long enough to surface bills that are coming but not yet imminent, and short enough that the projection remains reliable.

If you're projected to overdraft, the date and amount are front and center the moment you open the app.

Every architectural choice serves the forecast. Onboarding combs through your checking account to identify recurring transactions automatically. The home screen is the forecast. The notification system alerts you both to forecast events (a shortfall is coming, your account will go below your Floor) and to maintenance needs (a projected transaction didn't post, an unprojected one did). Every action is designed around two principles: reduce the work required to create and maintain the forecast, and improve forecast accuracy and comprehension.

Eight criteria, eight Delivers — not coincidence, but the natural result of an app architected end-to-end around a single question.

Centinel and Simplifi differ in more than overdraft handling; Centinel vs. Simplifi compares them feature by feature across the full forecasting workflow.

PocketSmith has a deterministic forecast with a horizon of 6 months to 60 years. Monarch Plus focuses on long-term financial planning including retirement, net worth, and multi-year goal projections. Both are built around long-term planning. Neither has the architectural emphasis on short-term checking account forecasting or overdraft prediction that the criteria above describe.

Focused on overdraft coverage rather than overdraft prediction. These apps run prediction algorithms internally to underwrite advances but don't surface the forecast to the user. The headline experience is a loan offer, not a projected balance the user can interact with or act on independently.

None of these project a checking account balance forward from saved cash flow events. They fail at the foundational criterion — there's no forecast to evaluate against the rest of the framework.

Reactive features (linked-account auto-transfers) that activate when an overdraft is imminent or has occurred. They don't forecast and don't surface risk in advance — they cover the gap after the fact.

Simplifi and Centinel are built for different jobs. Simplifi is a comprehensive personal finance suite where forecasting is one capability among many; for users who want PFM with budgeting at the center, it's a strong choice. Centinel is architected end-to-end around overdraft prediction — the forecast is the product, the metrics are actionable, the reconciliation infrastructure exists to keep the forecast accurate, and the same-day timing is conservative by design. The other tools surveyed above are built for genuinely different problems: long-horizon planning, post-overdraft coverage, budgeting without forecasting, or reactive bank protection. If your primary need is overdraft prevention, the architectural difference is the difference between working with the app and working around it.

Centinel is currently in pre-launch — join the waitlist for early access.

Yes. Centinel is architected end-to-end around overdraft prediction, with a 2-month deterministic forecast, transaction reconciliation, conservative same-day timing, and overdraft risk surfaced as the headline metric. Quicken Simplifi has a Projected Cash Flow feature that can be configured to predict overdrafts, though forecasting is one capability within a broader budgeting suite rather than the product's foundation. Other apps marketed around overdraft prediction generally fall short on one or more of the architectural criteria that genuine prediction requires.

Predictive tools forecast your future balance and surface projected shortfalls with enough lead time to act. Coverage tools — cash advance apps and bank overdraft protection programs — activate after a shortfall is imminent or has already occurred. They solve related but different problems: one helps you avoid the overdraft; the other helps you handle it.

Some can be configured to but aren’t ideal for this use case. Quicken Simplifi has a real forecast and a configurable low-balance alert that's on by default, but the app is ultimately architected around budgeting. Most other budgeting apps — Monarch standard, Copilot, Rocket Money, YNAB — don't currently project daily forward checking-account balances and aren't built for this use case. If you’re interested in predicting overdrafts, using an app specifically designed for this purpose is the better choice.

Most major banks offer overdraft protection (linked-account auto-transfers) and overdraft notifications, but these are reactive rather than predictive — they activate when an overdraft is imminent or has occurred, not in advance with enough lead time to change course.

Centinel is currently iOS-only. Android is on the roadmap but not yet available.

Centinel is built for anyone who wants to stay ahead of overdrafts rather than react to them. If you've ever been surprised by a low balance, hit with an overdraft fee you didn't see coming, or held back from moving cash to savings because you weren't sure what was safe, Centinel is built to give you that visibility.

STAY A STEP AHEAD